|

|

|

|

|||||

|

|

|

IAMGOLD Corporation IAG is slated to report fourth-quarter 2025 results after market close on Feb. 17. The company’s performance is expected to have benefited from strong production growth and record sales volumes, as well as higher realized gold prices.

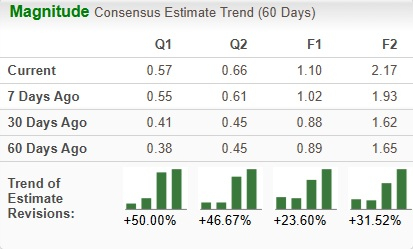

The Zacks Consensus Estimate for fourth-quarter earnings has been going up in the past 30 days. The consensus estimate for earnings is pegged at 57 cents per share, suggesting a 470% year-over-year surge.

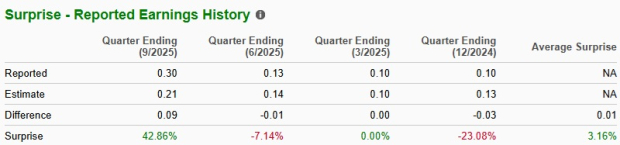

In the trailing four quarters, IAG beat the Zacks Consensus Estimate for earnings in one quarter, missed twice and came in line in one quarter. In this timeframe, it delivered an earnings surprise of roughly 3.2%, on average.

Our proven model does not conclusively predict an earnings beat for IAG this season. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy), or 3 (Hold) increases the chances of an earnings beat. But that’s not the case here. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

IAMGOLD has an Earnings ESP of 0.00% and a Zacks Rank #2. You can see the complete list of today’s Zacks #1 Rank stocks here.

A primary driver is expected to have been the continued gold price strength, as higher realized prices directly lift revenue and margins by expanding per-ounce profitability and overall cash generation. Realized prices averaged roughly $4,190 per ounce for the fourth quarter, well above the prior-year levels.

IAMGOLD recorded quarterly production of 242,400 ounces, reflecting a 37.2% year-over-year increase. This indicates improved execution across its diversified asset base, particularly at Côté Gold, Essakane and Westwood, all of which reported their highest quarterly outputs to date.

Production performance across its key assets will remain a critical earnings lever, as higher throughput and improved reliability directly translate into greater volumes sold and lower unit costs. The continued ramp-up at Côté Gold is particularly important, with rising mill utilization, stronger recoveries and record output driving incremental ounces and meaningful economies of scale. Essakane provides steady, base-level production supported by consistent grades and stable plant performance, underpinning predictable cash flow generation. At Westwood, ongoing underground development, improved stope sequencing and higher throughput are lifting productivity and supporting a gradual normalization of costs.

Cost and margin pressures are likely to have persisted in the quarter, as cash costs and all-in sustaining costs (AISC) remain sensitive to gold-linked royalties, higher fuel and consumables prices, and temporary ramp-up inefficiencies that should gradually ease as operations stabilize.

IAMGOLD is expected to report consolidated cash costs near the top end of $1,375–$1,475 per ounce and AISC of $1,830–$1,930 per ounce, up year over year from roughly $1,152 per ounce and $1,716 per ounce, respectively. This reflects higher unit costs and royalties.

IAG’s shares have shot up 208.2% over the past year, outperforming the Zacks Mining – Gold industry’s 121.3% increase and the S&P 500’s rise of 14%. Among its peers, Centerra Gold, inc. CGAU, AngloGold Ashanti Plc. AU and Gold Fields Limited GFI have rallied 169.6%, 215% and 169.1%, respectively, over the same period.

From a valuation standpoint, IAG is currently trading at a forward 12-month sales multiple of 4.49. This represents a roughly 28% premium when stacked up with the industry average of 3.52X. IAG is trading at a premium to Centerra Gold, AngloGold and Gold Fields. CGAU has a Value Score of B, while AU and GFI have a Value Score of D.

IAMGOLD is well-positioned to benefit from the ramp-up of the Côté Gold project and steadier performance across its Canadian and West African mines, driving higher production, improved scale efficiencies and stronger margins amid elevated gold prices. With major capital spending largely complete, the company is prioritizing debt reduction, balance sheet strength and potential shareholder returns, supporting a more disciplined, value-focused strategy and improved cash flow. Longer term, exploration upside in Québec adds growth optionality. Key risks include gold price volatility, cost inflation, execution challenges and geopolitical uncertainty at the Essakane Mine, which could pressure earnings stability.

IAMGOLD is expected to post strong fourth-quarter results, mainly driven by higher gold production from the continued ramp-up and stable throughput at Côté Gold alongside solid operating consistency at Essakane and Westwood, which together lifted volumes and sales. Elevated realized gold prices and improving operational efficiencies are expected to have boosted margins and free cash flow.

Exploration success in Québec and ongoing optimization initiatives across the portfolio add longer-term growth upside beyond current guidance. With major capital spending largely complete, the company can now focus on debt reduction and potential shareholder returns, while exploration and optimization efforts add longer-term growth upside. Buying the IAG stock will be prudent for investors before its forthcoming earnings release.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-23 | |

| Jul-20 | |

| Jul-15 | |

| Jul-15 | |

| Jul-14 | |

| Jul-13 | |

| Jul-09 | |

| Jul-08 | |

| Jul-07 | |

| Jul-06 | |

| Jul-06 | |

| Jul-06 | |

| Jun-26 | |

| Jun-19 | |

| Jun-17 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite