|

|

|

|

|||||

|

|

|

Citigroup, Inc. C stock is currently trading at a 12-month trailing price-to-earnings (P/E) of 10.67X, which is below the industry’s 14.42X. This shows the stock is trading at a discount.

Price-to-Earnings F12M

The C stock is also attractively priced compared with peers such as Bank of America BAC and Wells Fargo WFC, which are trading at higher multiples of 12X and 12.33X, respectively.

Let us dig deeper to understand if the current valuation makes Citigroup a smart bet.

Citigroup’s stock has appreciated 31.5% in a year, outperforming the industry’s 19.1% growth. It has also pulled ahead of key peers, with Bank of America rising 11.9% and Wells Fargo gaining 7.7%.

Price Performance

Image Source: Zacks Investment Research

With a cheaper valuation and an upbeat price performance, let us find out what awaits Citigroup this year.

From Complexity to Focus: CEO Jane Fraser continues to advance the company’s multi-year strategy to streamline operations and focus on its core businesses. Since announcing plans in April 2021 to exit consumer banking in 14 markets across Asia and EMEA, the company has completed its exit in nine countries.

In December 2025, Citigroup agreed to sell its Russia-based banking unit, AO Citibank, to Renaissance Capital. The transaction is expected to improve the bank’s capital position over time by eliminating related risk-weighted assets. The same month, C divested a 25% stake in Banamex to a Mexican business leader after separating its Mexican institutional banking business from consumer and middle-market units in December 2024. The company is now preparing for a planned initial public offering (IPO) of its Mexican consumer, and small and middle-market banking units.

In May 2025, C announced an agreement to sell its consumer banking business in Poland, while in June 2024, it sold its China-based consumer wealth portfolio. Also, as part of its strategy, Citigroup continues to make progress with the wind-down of its Korea consumer banking operations. These initiatives will free up capital and help the company pursue investments in wealth management and investment banking (IB) operations, which will stoke fee income growth.

In sync with its plan to accelerate its IB business growth, Citigroup plans to increase its Japan IB headcount by 30% by the first half of 2026 to seize opportunities from a surge in merger and acquisition (M&A) deals, according to a Seeking Alpha article published on MSN.

These initiatives will free up capital and help the company pursue investments in wealth management operations in Singapore, Hong Kong, the UAE and London to stoke fee income growth. Supported by these initiatives, Citigroup expects revenues to see a 4-5% CAGR through 2026.

Push for Efficiency: The company continues to focus on streamlining processes and platforms, and driving automation to reduce manual touchpoints. Citigroup is increasingly deploying artificial intelligence (AI) tools to support these efforts. In support of this strategy, the company signed a multi-year agreement this week with LSEG to modernize its enterprise-wide data infrastructure. The initiative spans markets, investment banking, wealth management, trading and risk functions, aiming to improve data quality, standardization and accessibility across the organization. Management expects these upgrades to enable more data-driven decisions while delivering operational efficiencies at scale.

The company also announced an organizational realignment to simplify its governance structure by eliminating various management layers. Pursuant to this, the company changed its operating model and the leadership structure. This resulted in a streamlined and straightforward management structure aligned with and supporting the bank's strategy of increased spans of control and significantly reduced bureaucracy and unnecessary complexity.

In January 2024, the bank announced plans to cut 20,000 jobs, approximately 8% of its global staff, by 2026. The bank has already made significant progress by reducing its headcount by more than 10,000 employees.

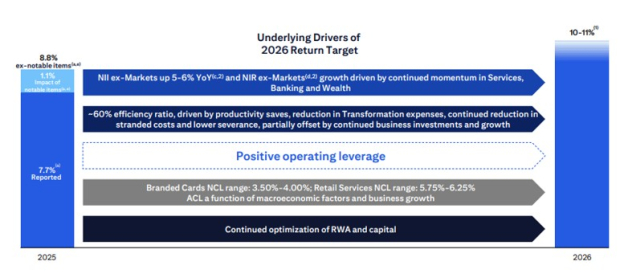

Given such efforts, the company expects to achieve $2-2.5 billion in annualized run rate savings by 2026. Further, management continues to target a return on tangible common equity (RoTCE) of 10-11% in 2026.

ROTCE

Macroenvironment & Regulatory Winds Turn Favorable: Citigroup stands to benefit from an increasingly supportive macro and regulatory backdrop. Following the initial easing in 2024 and three subsequent rate cuts in 2025, interest rates stand at 3.50-3.75% currently. With lower rates, funding costs gradually stabilize, supporting increased borrowing, which means more loan volumes.

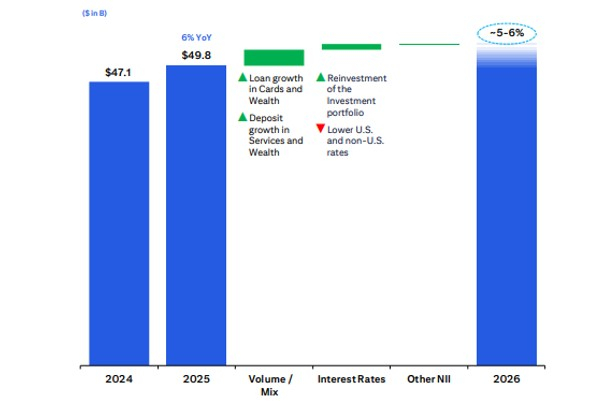

Hence, C is expected to witness decent net interest income (NII) growth in the quarters ahead, supported by lower funding costs, increased loan volumes and repricing of maturing assets into higher yields. NII witnessed a three-year compounded annual growth rate (CAGR) of 6.2% (ended 2025). Management expects NII, excluding markets, to increase 5-6% year over year in 2026.

NII Outlook

Reduced rates are likely to accelerate deal-making momentum by lowering financing costs and prompting companies to revive delayed M&A and capital-raising plans. Cheaper capital, along with resilient economic growth, typically boosts deal pipelines and IPO readiness. This improved backdrop positions Citigroup for stronger IB revenues in the upcoming period.

At the same time, regulatory pressures are easing. C has received notable regulatory relief after the Office of the Comptroller of the Currency (OCC) removed the July 2024 amendment to the bank’s 2020 consent order. This original consent order was focused on longstanding deficiencies in risk management, data governance, internal controls and compliance. The regulatory easing aligns with Citigroup’s broader strategy to modernize its technology and control data.

The firm has outlined plans to reduce reliance on external IT contractors while expanding internal technology headcount, strengthening in-house governance and execution capabilities. With this burden lifted, C is better-positioned to execute its growth and efficiency initiatives.

Solid Liquidity Aids Capital Distribution: C enjoys a strong liquidity position. As of Dec. 31, 2025, Citigroup’s cash and due from banks and total investments aggregated to $476.7 billion, while its total debt (short-term and long-term borrowing) was $335.8 billion.

Post-clearing the 2025 Fed stress test, the company hiked its dividend 7.1% to 60 cents per share. In the past five years, it has raised its dividends three times. It has a payout ratio of 30%. It has a dividend yield of 2.04%. Wells Fargo has raised its dividend six times in the past five years, while Bank of America has increased its dividend five times in the past five years.

In January 2025, Citigroup's board of directors approved a $20-billion common stock repurchase program with no expiration date. As of Dec. 31, 2025, $6.8 billion worth of authorization remained available. Supported by a strong capital and liquidity position, its capital distribution activities seem sustainable.

Asset Quality: Citigroup’s asset quality has been deteriorating. While the company recorded negative provisions in 2021, a substantial jump in provisions was recorded in the years after that because of the worsening macroeconomic outlook. The metric saw a CAGR of 24.5% from 2022 to 2025. Though interest rates have declined, deterioration due to softer labor markets and economic and geopolitical uncertainty might hurt the company’s asset quality in the near term.

The Zacks Consensus Estimate for Citigroup’s 2026 and 2027 earnings implies year-over-year rallies of 28.2% and 17.8%, respectively. Over the past month, the estimates for both years have been revised upward.

Estimate Revision Trend

Citigroup presents a compelling mix of discounted valuation, improving earnings momentum, solid capital strength and a clearer strategic focus. The bank’s ongoing divestitures, efficiency initiatives and reinvestment in higher-return businesses such as wealth management and investment banking position it well for medium-term growth. A more favorable macro and regulatory backdrop, along with accelerating consensus earnings estimates for 2026 and 2027, further support the fundamental outlook.

However, risks temper the bullish case. Asset quality trends warrant close monitoring amid economic uncertainty, and execution risks remain as the company continues its operational overhaul. Moreover, after a strong rally over the past year, a portion of the turnaround optimism appears to be already reflected in the stock price.

Considering the balance of improving fundamentals, reasonable valuation, solid capital returns, and lingering execution and credit risks, the prudent stance at this stage is holding Citigroup stock. Long-term investors can remain patient as the transformation story unfolds, but aggressive new buying may be better timed after clearer evidence of sustained return-on-equity expansion and asset-quality stabilization.

Citigroup currently has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 46 min | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 2 hours | |

| 2 hours | |

| 3 hours | |

| 9 hours | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite