|

|

|

|

|||||

|

|

|

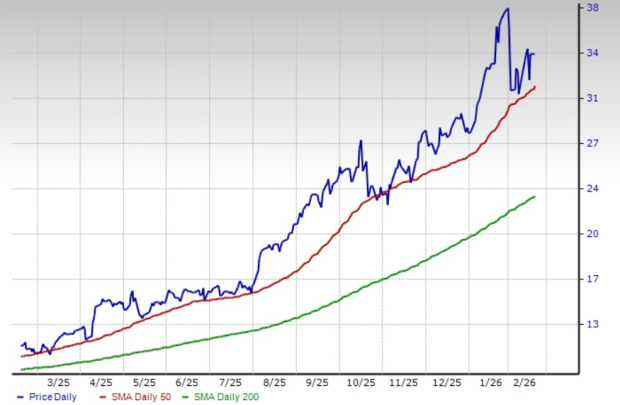

Kinross Gold Corporation’s KGC shares have gained 38.1% over the past three months, largely driven by an unprecedented rally in gold prices. KGC has outperformed the Zacks Mining – Gold industry’s growth of 36.1% and the S&P 500’s rise of 3%. Its gold mining peers, Barrick Mining Corporation B, Newmont Corporation NEM and Agnico Eagle Mines Limited AEM, have rallied 29.9%, 44.4% and 30.8%, respectively, over the same period.

Technical indicators show that KGC has been trading above the 200-day simple moving average (SMA) since March 6, 2024. The stock is also currently trading above its 50-day SMA. The 50-day SMA continues to read higher than the 200-day moving average, indicating a bullish trend.

Let’s take a look at KGC’s fundamentals to better analyze how to play the stock.

Kinross has a strong production profile and boasts a promising pipeline of exploration and development projects. Its key development projects and exploration programs remain on track. These projects are expected to boost production and cash flow and deliver significant value. The successful execution of these projects will position the company for a new wave of low-cost, long-life production.

KGC recently said that it is progressing with the construction of three organic growth projects to expand its U.S. portfolio. This is aimed at extending mine life and cost optimization. The projects are Round Mountain Phase X and Bald Mountain Redbird 2 in Nevada, and the Kettle River–Curlew project in Washington.

Together, these projects are expected to contribute significantly to Kinross’ U.S. production profile and add a strong value proposition with a combined Internal Rate of Return (IRR) of 55% and a combined incremental post-tax Net Present Value (NPV) of $4.1 billion. These projects are expected to contribute 3 million ounces of life-of-mine production to KGC’s portfolio, adding grades and mine lives. Kinross Gold is planning to self-fund three growth projects entirely from operating cash flows, reflecting its disciplined strategy.

Tasiast and Paracatu, the company’s two biggest assets, remain the key contributors to cash flow generation and production. Tasiast remains the lowest-cost asset within its portfolio, with a consistently strong performance. Paracatu continues to deliver a strong performance, with third-quarter production rising year over year on higher grades. KGC also completed the commissioning of its Manh Choh project and commenced production during the third quarter of 2024, leading to a substantial increase in cash flow at the Fort Knox operation.

KGC has a strong liquidity position and generates substantial cash flows, which allows it to finance its development projects, pay down debt and drive shareholder value. Kinross reactivated its share buyback program in April 2025. It completed a $600 million share repurchase program as of Dec. 31, 2025. It returned more than $750 million to its shareholders through dividends and buybacks in 2025, ending the year with about $1 billion in net cash.

In 2025, the company repaid $700 million of debt. With $1.6 billion in available credit (as of Sept. 30, 2025) and no debt maturities until 2033, Kinross is well-positioned to support growth while strengthening its balance sheet and delivering shareholder value.

KGC offers a dividend yield of 0.4% at the current stock price. It has a payout ratio of 9% (a ratio below 60% is a good indicator that the dividend will be sustainable). Backed by strong cash flows and sound financial health, the company's dividend is perceived as safe and reliable.

Surging gold prices should boost KGC’s profitability and drive cash flow generation. Gold prices shot up to record highs in 2025, ending the year with a 65% gain, largely attributable to aggressive trade policies, including sweeping new import tariffs announced by President Donald Trump that intensified global trade tensions and heightened investor anxiety. Also, central banks worldwide have been accumulating gold reserves, led by risks arising from Trump’s policies. The rally was further supported by the Federal Reserve’s rate cuts and expectations of additional easing amid signs of U.S. economic softening and labor market concerns.

Escalating geopolitical strains, including the unrest in Iran with the possibility of U.S. intervention, a weaker greenback, fresh tariff threats and renewed concerns over the independence of the Federal Reserve, drove bullion to a record high of nearly $5,600 per ounce in late January. While gold prices have pulled back from that level, partly due to aggressive profit-taking and a rebound in the U.S. dollar, they remain elevated, currently hovering near $5,000 per ounce.

Sustained central-bank purchases, hopes of more interest rate cuts following the softer-than-anticipated inflation data and persistent safe-haven demand tied to prevailing geopolitical tensions due to U.S.-Iran tensions and broader macroeconomic uncertainties are likely to continue to support gold prices.

Kinross is exposed to headwinds from higher production costs. It saw a roughly 17% year-over-year rise in production cost of sales per ounce to $1,145 in the third quarter. All-in-sustaining costs (AISC), a key indicator of cost efficiency in mining, rose nearly 20% year over year to $1,622 per gold equivalent ounce sold and were also up from $1,493 in the prior quarter. The inflationary pressure is likely to continue in the fourth quarter, weighing on KGC’s profit margins and overall financial performance. The company expects an AISC of $1,500 per ounce for 2025, which indicates a significant year-over-year rise. The expected increase is due to a rise in the production cost of sales.

Earnings estimates for KGC have been rising over the past 60 days, reflecting analysts’ optimism. The Zacks Consensus Estimate for 2025 and 2026 has been revised upward over the same time frame.

The Zacks Consensus Estimate for 2025 earnings is currently pegged at $1.69, suggesting year-over-year growth of 148.5%. Earnings are also expected to register roughly 52.9% growth in 2026.

Kinross Gold is currently trading at a forward 12-month earnings multiple of 13.39, a roughly 4.7% discount to the peer group average of 14.05X. KGC is trading at a premium to Barrick Mining and at a discount to Newmont and Agnico Eagle. Kinross Gold and Barrick Mining have a Value Score of B, each, while Agnico Eagle and Newmont have a Value Score of C.

KGC has a strong pipeline of development projects and solid financial health. Rising earnings estimates and a healthy growth trajectory are the other positives. Kinross continues to demonstrate strong financial performance and remains committed to driving shareholder returns. The company is generating solid free cash flow and deleveraging rapidly, benefiting from a favorable gold price environment. However, its higher production costs warrant caution. Holding onto this Zacks Rank #3 (Hold) stock will be prudent for investors who already own it.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| 2 hours | |

| 3 hours | |

| 3 hours | |

| 4 hours | |

| 4 hours | |

| 5 hours | |

| 5 hours | |

| 6 hours | |

| 6 hours | |

| 6 hours | |

| 6 hours | |

| Aug-09 | |

| Aug-07 | |

| Aug-07 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite