|

|

|

|

|||||

|

|

|

Dillard’s, Inc. DDS is expected to register a year-over-year decline in the bottom line when it reports fourth-quarter fiscal 2025 numbers.

The Zacks Consensus Estimate for fiscal fourth-quarter revenues of $2.02 billion indicates 0.16% growth from the year-ago reported figure. The consensus estimate for earnings is pegged at $9.98 per share, implying a 26% decrease from the year-ago quarter’s reported figure. The consensus estimate has been unchanged in the past 30 days.

In the last reported quarter, the company registered an earnings surprise of 29.2%. We note that in the trailing four quarters, its bottom line beat the Zacks Consensus Estimate by 26.5%, on average.

Dillard's, Inc. price-eps-surprise | Dillard's, Inc. Quote

Dillard's fourth-quarter fiscal 2025 results are expected to reflect the benefits of its growth initiatives and solid execution. The company has been gaining from its efforts to capture growth opportunities in brick-and-mortar stores and the e-commerce business, aiding in retaining existing customers and attracting new ones. In brick-and-mortar stores, the company has been strengthening its customer base through store enhancements, including better brand partnerships, trend-focused assortments, remodels and stronger personnel incentives. Additionally, the company’s activewear brand is expected to have gained market share in the to-be-reported quarter.

DDS’s e-commerce business has been another growth driver. The company’s e-commerce business is catching pace with strategies like the enhancement of merchandise assortments. We expect the company to gain from its focus on increasing productivity at existing stores, developing a leading omni-channel platform and enhancing domestic operations in the quarters ahead. These efforts are expected to have bolstered performance in the fiscal fourth quarter. Our model predicts flat year-over-year comparable-store sales for the fiscal fourth quarter.

However, Dillard’s has been witnessing the adverse impacts of a tough retail environment due to consumers’ cautious buying behavior. Additionally, higher operating expenses from elevated payroll and payroll-related costs, and investments in store personnel to support service levels and sales execution, have been headwinds. While Dillard’s continues to focus on expense control and operational efficiency, these efforts are not enough to fully offset the expenses related to wages and staffing requirements in the near term. This is likely to have dented margins and the bottom line in the fiscal fourth quarter.

We expect SG&A expenses to increase 4.8% year over year for the fiscal fourth quarter, with the SG&A expense rate anticipated to expand 120 basis points to 23.2%. Our model predicts a 16.1% year-over-year decline in operating profit, with a 190-bps contraction in the operating margin.

Our proven model does not conclusively predict an earnings beat for Dillard’s this time. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the chance of an earnings beat. But that is not the case here. You can uncover the best stocks before they are reported with our Earnings ESP Filter.

Dillard’s currently has an Earnings ESP of 0.00% and a Zacks Rank #2.

From a valuation perspective, Dillard’s is trading at a premium relative to industry and historical benchmarks. The company has a forward 12-month price-to-earnings ratio of 20.82X, higher than the Retail - Regional Department Stores industry’s average of 14.71X. The company is trading above its five-year median of 13.14X.

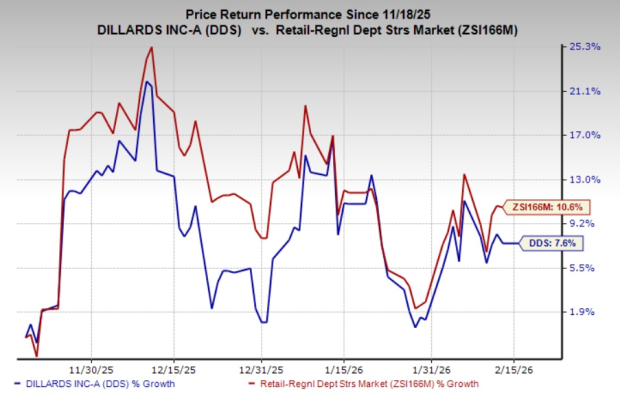

The market movements have shown that DDS shares have gained 7.6% in the past three months compared with the industry's 10.6% growth.

Here are a few companies worth considering, as our model shows that these have the right combination of elements to beat on earnings this reporting cycle.

American Eagle Outfitters Inc. AEO currently has an Earnings ESP of +1.06% and it flaunts a Zacks Rank of 1. The company is likely to report increases in the top and bottom lines when it reports fourth-quarter fiscal 2025 results. The consensus mark for revenues is pegged at $1.73 billion, which indicates an increase of 7.9% from the figure reported in the year-ago quarter. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for AEO’s quarterly earnings per share of 71 cents implies growth of 31.5% from the year-ago quarter’s actual. The consensus mark has increased 2.9% in the past 30 days. AEO has a trailing four-quarter earnings surprise of 35.1%, on average.

Dollar General Corporation DG currently has an Earnings ESP of +7.37% and a Zacks Rank of 2. The company is likely to register an increase in the top line when it reports fourth-quarter fiscal 2025 numbers. The consensus mark for revenues is pegged at $10.74 billion, which indicates a rise of 4.3% from the figure reported in the year-ago quarter.

The Zacks Consensus Estimate for DG’s quarterly earnings per share of $1.57 implies 6.6% year-over-year decline. The consensus mark for earnings has been unchanged in the past 30 days. DG has a trailing four-quarter earnings surprise of 22.9%, on average.

The Home Depot Inc. HD currently has an Earnings ESP of +5.61% and a Zacks Rank #3. The company is likely to report declines in both the top and bottom lines when it reports fourth-quarter fiscal 2025 results. The consensus mark for revenues is pegged at $38.25 billion, which indicates a decline of 3.7% from the figure reported in the year-ago quarter.

The Zacks Consensus Estimate for HD’s fourth-quarter fiscal 2025 EPS is pegged at $2.51, implying a 19.8% year-over-year decline. The consensus mark for EPS has been unchanged in the past 30 days. HD delivered a trailing four-quarter negative earnings surprise of 0.09%, on average.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-23 | |

| Jul-20 | |

| Jul-17 | |

| Jul-16 | |

| Jul-15 | |

| Jul-15 | |

| Jul-14 | |

| Jul-13 | |

| Jul-13 | |

| Jul-10 | |

| Jul-10 | |

| Jul-10 | |

| Jul-10 | |

| Jul-10 | |

| Jul-10 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite