|

|

|

|

|||||

|

|

|

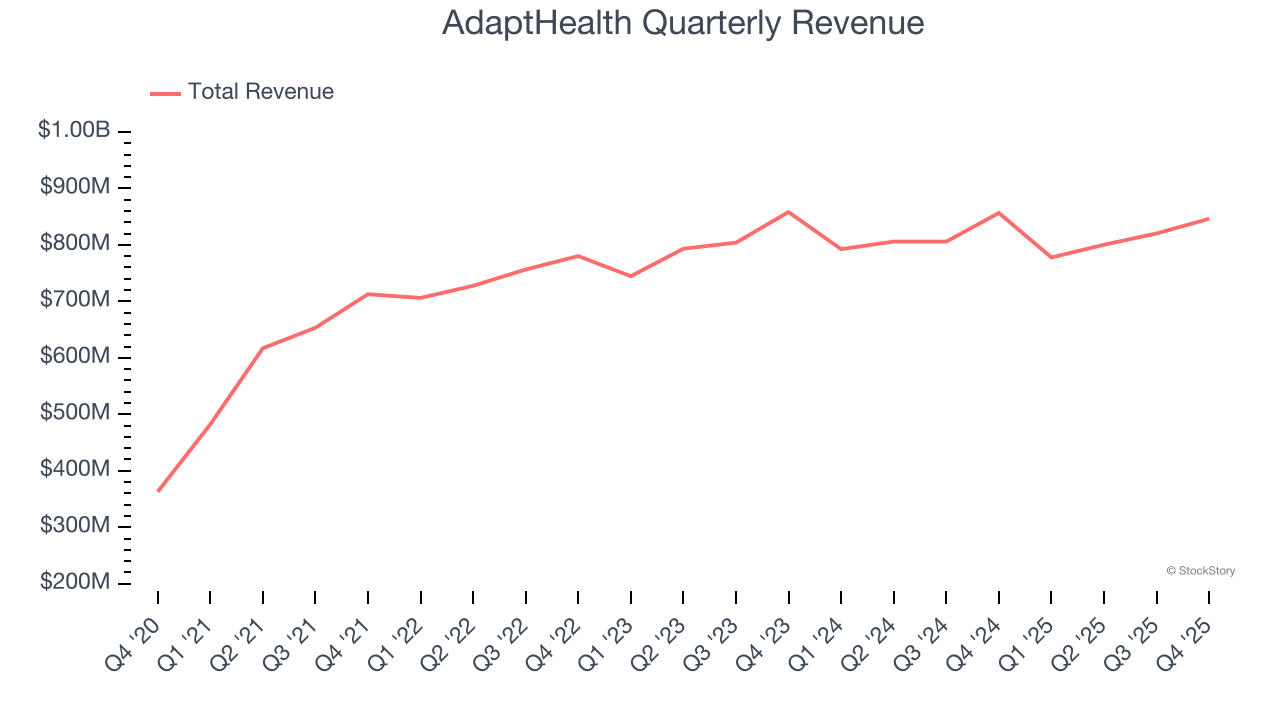

Healthcare services provider AdaptHealth Corp. (NASDAQ:AHCO) reported Q4 CY2025 results beating Wall Street’s revenue expectations, but sales fell by 1.2% year on year to $846.3 million. The company’s full-year revenue guidance of $3.48 billion at the midpoint came in 1% above analysts’ estimates. Its GAAP loss of $0.76 per share was significantly below analysts’ consensus estimates.

Is now the time to buy AdaptHealth? Find out by accessing our full research report, it’s free.

With a network of approximately 680 locations serving patients across all 50 states, AdaptHealth (NASDAQ:AHCO) provides home medical equipment, supplies, and related services to patients with chronic conditions like sleep apnea, diabetes, and respiratory disorders.

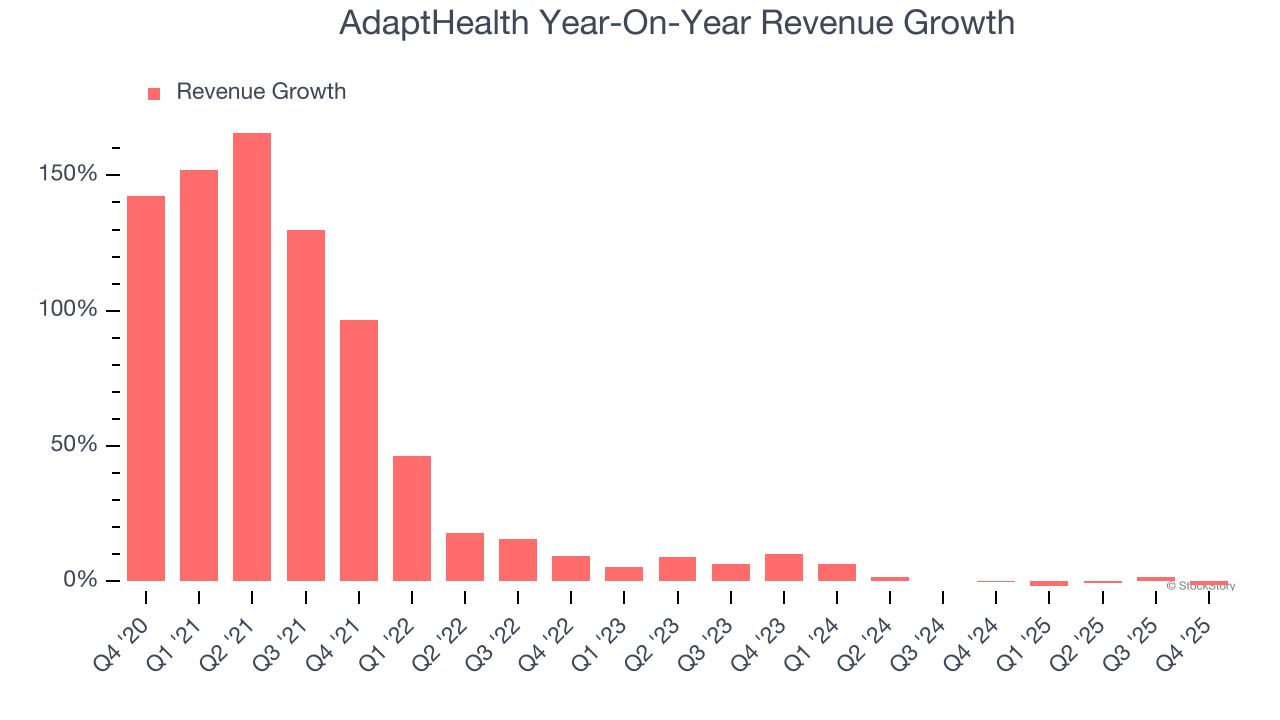

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Thankfully, AdaptHealth’s 24.8% annualized revenue growth over the last five years was excellent. Its growth beat the average healthcare company and shows its offerings resonate with customers.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. AdaptHealth’s recent performance shows its demand has slowed significantly as its revenue was flat over the last two years.

This quarter, AdaptHealth’s revenue fell by 1.2% year on year to $846.3 million but beat Wall Street’s estimates by 2.1%.

Looking ahead, sell-side analysts expect revenue to grow 6% over the next 12 months, an improvement versus the last two years. This projection is above the sector average and indicates its newer products and services will fuel better top-line performance.

The 1999 book Gorilla Game predicted Microsoft and Apple would dominate tech before it happened. Its thesis? Identify the platform winners early. Today, enterprise software companies embedding generative AI are becoming the new gorillas. a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

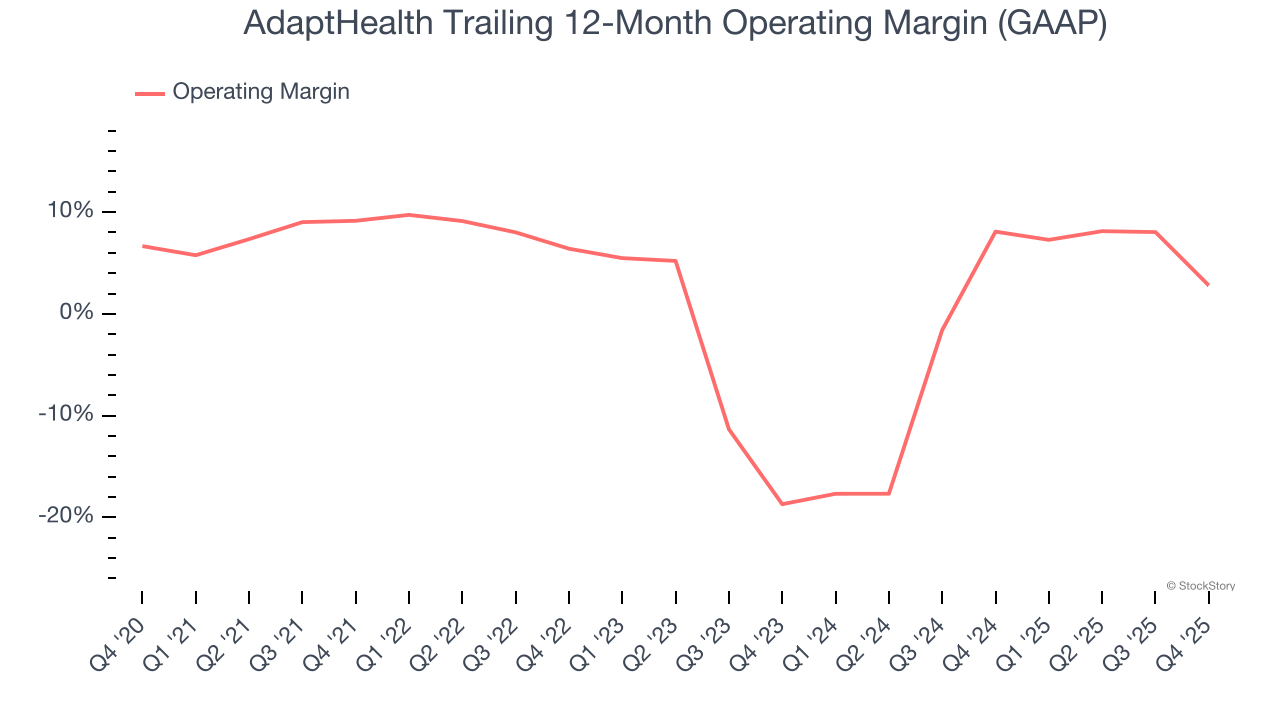

AdaptHealth was profitable over the last five years but held back by its large cost base. Its average operating margin of 1.1% was weak for a healthcare business.

Analyzing the trend in its profitability, AdaptHealth’s operating margin decreased by 6.4 percentage points over the last five years, but it rose by 21.5 percentage points on a two-year basis. Still, shareholders will want to see AdaptHealth become more profitable in the future.

In Q4, AdaptHealth generated an operating margin profit margin of negative 8.7%, down 20.1 percentage points year on year. This contraction shows it was less efficient because its expenses increased relative to its revenue.

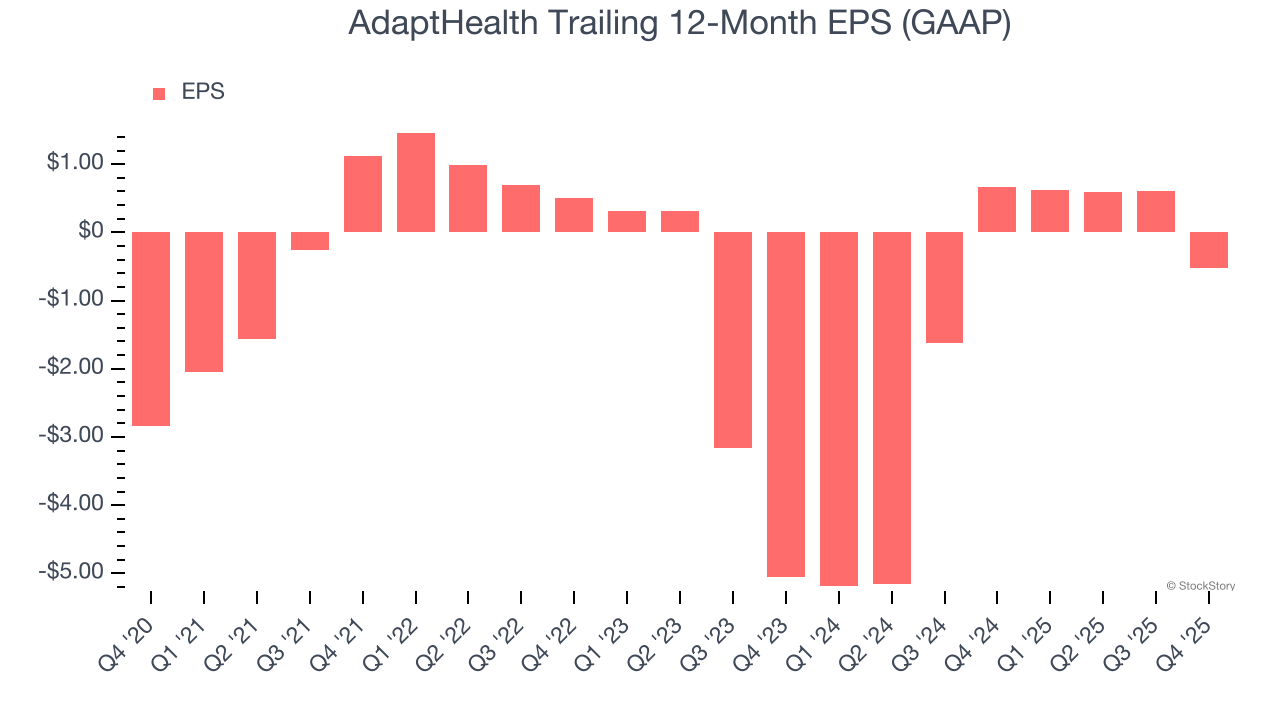

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Although AdaptHealth’s full-year earnings are still negative, it reduced its losses and improved its EPS by 28.6% annually over the last five years. The next few quarters will be critical for assessing its long-term profitability.

In Q4, AdaptHealth reported EPS of negative $0.76, down from $0.37 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street is optimistic. Analysts forecast AdaptHealth’s full-year EPS of negative $0.53 will flip to positive $0.89.

It was encouraging to see AdaptHealth beat analysts’ revenue expectations this quarter. We were also glad its full-year revenue guidance slightly exceeded Wall Street’s estimates. On the other hand, its EPS missed. Zooming out, we think this was a mixed quarter. The stock remained flat at $10.29 immediately following the results.

So should you invest in AdaptHealth right now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).

| 17 min | |

| Jul-20 | |

| Jul-20 | |

| Jul-14 | |

| Jul-07 | |

| Jul-06 |

AdaptHealth discloses June cyberattack resulting in patient data exposure

AHCO

Medical Device Network

|

| May-05 | |

| May-05 | |

| May-05 | |

| May-04 | |

| Apr-14 | |

| Apr-13 | |

| Mar-03 | |

| Mar-03 | |

| Feb-25 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite