|

|

|

|

|||||

|

|

|

Ciena Corporation CIEN and Cisco Systems, Inc. CSCO are prominent players in the global networking industry, providing critical infrastructure that enables data transmission, cloud connectivity and enterprise communications. Their solutions support service providers, hyperscalers and enterprises as demand rises for high-speed networks driven by AI workloads, video streaming and digital transformation initiatives.

While both companies operate in the broader networking space, their business mix and scale differ meaningfully. Ciena is more focused on optical networking and data-center interconnect solutions, positioning it to benefit from surging bandwidth requirements. Cisco offers a broader portfolio spanning switching, routing, security and software, giving it greater diversification and a more established global footprint.

According to a report by Grand View Research, the global enterprise networking market was valued at $215.45 billion in 2024 and is projected to reach $298.30 billion by 2030 at a compound annual growth rate (CAGR) of 5.4% from 2025 to 2030. So, for investors looking to make a smart move in the Networking space, which stock truly stands out?

Let’s analyze their fundamentals, growth opportunities, market challenges and valuation to assess which one presents a stronger investment opportunity.

Ciena is witnessing encouraging momentum driven by improving customer spending and the rapid proliferation of AI applications. Rising network traffic and bandwidth demand are prompting cloud and service provider customers to prioritize infrastructure investments, supporting long-term opportunities for its Systems and Interconnects businesses. Ciena is benefiting from strong traction in optical networking, pluggables and data center interconnect (DCI). Its interconnects portfolio, particularly in pluggables for AI-driven metro data center campuses, is gaining momentum, with fiscal 2025 pluggable revenue surpassing $168 million and expectations for further growth.

Also, Ciena is strategically aligning its portfolio toward metro, edge and AI-driven data center opportunities. Strategic acquisitions such as Tibit Communications, Benu Networks and AT&T’s Vyatta assets have strengthened its routing and edge capabilities, while the 2025 acquisition of Nubis expanded its high-performance, low-power interconnect offerings for AI workloads. Ciena is scaling R&D in coherent optical systems, routing and interconnect technologies, including its DCOM solution—originally co-developed with Meta—which is being deployed across multiple hyperscale data centers.

The company continues to strengthen its technology leadership through its WaveLogic, Reconfigurable Line System (RLS), Navigator and Interconnect portfolios. WaveLogic 6 and RLS provide a competitive edge in AI-driven networking, highlighted by WaveLogic 6 Extreme enabling Poland’s first 1.2 Tb/s optical transmission.

With a $5 billion backlog, including $3.8 billion in hardware and software, the company has solid revenue visibility into fiscal 2026 and early signs of demand strength extending into 2027. Management is addressing input cost pressures through supply rebalancing, cost controls and pricing actions, with margin improvement expected in the latter half of fiscal 2026.

Ciena Corporation price-consensus-chart | Ciena Corporation Quote

However, the company continues to face elevated expense levels due to ongoing strategic investments in business expansion and technology upgrades. The company is also dealing with near-term headwinds from new product introduction (NPI) ramp challenges and rising input costs amid supply constraints. Planned fiscal 2026 capex of $250–$275 million, above historical levels, is expected to weigh on near-term cash flow, particularly with increasing 3-nanometer mask set costs.

Additionally, Ciena derives a substantial portion of its revenue from a limited number of large global communications service providers. In a highly competitive industry, the loss or reduced spending of any major customer could adversely impact its financial performance.

For the first quarter of fiscal 2026, management expects revenues in the range of $1.35-$1.43 billion. The adjusted gross margin is estimated between 43% and 44%. Adjusted operating margin estimated at 15.5-16.5%. The company is scheduled to report fiscal first-quarter results on March 5, 2026.

Cisco is experiencing strong growth momentum, driven primarily by accelerating AI adoption across cloud and enterprise environments. The company has secured more than $2 billion in AI infrastructure orders in fiscal 2025 and an additional $2.1 billion from hyperscalers in the second quarter of fiscal 2026, reflecting rising investments in AI-optimized networking. Expanding demand from major cloud providers is supporting growth across Cisco’s networking and data center portfolios.

A key growth driver is Cisco’s expanding AI-focused product portfolio. The company is introducing advanced solutions, such as Unified Nexus Dashboard, Intelligent Packet Flow, configurable AI PODs and 400G BiDi optics to support AI-scale data centers. Its collaboration with NVIDIA, including the Secure AI Factory built on NVIDIA Spectrum-X and integration of AI Defense and Hypershield, is strengthening its position in AI infrastructure and enabling secure, scalable AI deployments.

Cisco’s security business is another major catalyst. The $28 billion acquisition of Splunk has enhanced its Threat Intelligence, Detection and Response, XDR, SASE and broader network security offerings. Strong customer adoption, including hundreds of new customer additions in recent quarters, highlights sustained demand for integrated, AI-powered security platforms across enterprises and cloud customers. Cisco’s products like Secure Access, XDR, Hypershield and AI Defense have gained traction by adding around 1000 new customers in the second quarter of fiscal 2026.

Cisco has been benefiting from a flexible and diversified supply chain that is driving gross margin expansion. This improvement, along with productivity enhancements and disciplined cost management, bodes well for operating margin expansion. Cisco’s investments in regional manufacturing and logistics have minimized exposure to high-tariff areas, helping the company cut import-related expenses. Cisco expects third-quarter fiscal 2026 non-GAAP gross margin to be between 65.5% and 66.5%. Non-GAAP operating margin is expected to be between 33.5% and 34.5%. Revenues are expected to be in the range of $15.4 billion-$15.6 billion for the third quarter. For fiscal 2026, Cisco projects revenues between $61.2 billion and $61.7 billion.

However, Cisco faces near-term headwinds from declining new orders, which could weigh on revenue growth. Intensifying competition from rivals has forced Cisco to offer discounts in the Ethernet switch and router markets, potentially pressuring margins despite strength in the edge segment. Additionally, with a substantial portion of revenue generated outside the Americas, the company remains exposed to foreign exchange volatility.

Over the past six months, CIEN shares have surged 280% while Cisco stock jumped 17.1%.

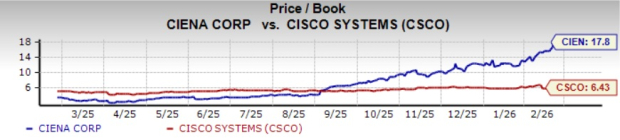

In terms of Price/Book, CIEN shares are trading at 17.8X, higher than CSCO’s 6.43X.

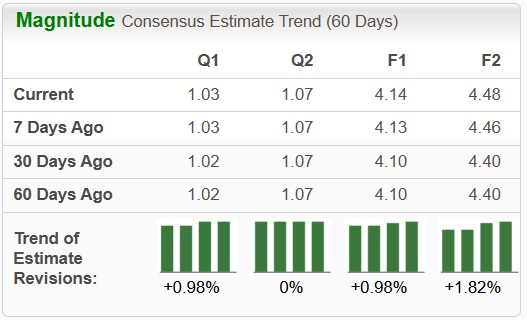

Analysts have revised their earnings estimates upward for CIEN’s bottom line for the current year.

For CSCO, there have been marginal upward revisions for the current year.

CIEN carries a Zacks Rank #3 (Hold) at present, while CSCO sports a Zacks Rank #1 (Strong Buy). Consequently, in terms of Zacks Rank and valuation, CSCO seems to be a better pick at the moment.

You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 3 hours | |

| Jul-21 | |

| Jul-20 | |

| Jul-20 | |

| Jul-18 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-16 | |

| Jul-15 | |

| Jul-15 | |

| Jul-15 | |

| Jul-15 | |

| Jul-15 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite