|

|

|

|

|||||

|

|

|

Lam Research Corporation LRCX and ASML Holding N.V. ASML are leading semiconductor equipment manufacturers that supply critical tools used in chip production. The two companies are playing a critical role in powering the artificial intelligence (AI)-driven boom in chip fabrication. As chipmakers rush to expand capacity for advanced nodes used in AI, 5G and high-performance computing (HPC), these two stocks have attracted significant attention.

While both benefit from the same industry tailwinds, their fundamentals, growth outlook and valuations offer different risk-reward profiles for investors considering semiconductor infrastructure exposure. Let’s see which stock is a better buy right now based on the abovementioned factors.

Lam Research is capitalizing on AI trends. It builds the tools chipmakers need to manufacture next-generation semiconductors, including high-bandwidth memory (HBM) and chips used in advanced packaging. These technologies are vital for powering AI and cloud data centers.

Lam Research’s products are not only critical but also innovative. For example, its ALTUS ALD tool uses molybdenum to improve speed and efficiency in chip production. Another product, the Aether platform, helps chipmakers achieve higher performance and density. These are essential capabilities as demand for advanced AI chips continues to increase.

In 2025, Lam Research’s revenues from advanced packaging grew significantly, and management anticipates strong 40% year-over-year growth for 2026. The industry’s migration to backside power distribution and dry-resist processing presents growth opportunities for LRCX’s cutting-edge fabrication solutions.

These trends are aiding Lam Research’s financial performance. The company has demonstrated consistent execution, maintaining quarterly revenues of more than $5 billion for the past three consecutive quarters, reflecting solid demand from leading chipmakers such as Taiwan Semiconductor Manufacturing and Samsung.

In the company’s last reported financial results for the second quarter of fiscal 2026, total revenues rose 22% year over year to $5.34 billion and beat the Zacks Consensus Estimate by 2.1%, primarily driven by continued demand across the Systems and Customer Support Business Group segments. Lam Research reported second-quarter non-GAAP earnings per share (EPS) of $1.27, surpassing the consensus estimate by 8.5%. The bottom line increased 39.6% year over year.

Lam Research Corporation price-consensus-eps-surprise-chart | Lam Research Corporation Quote

Sustained demand for AI and HPC chips by global data centers, AI labs and hyperscalers has reinforced ASML Holding’s long-term growth outlook as the company provides extreme ultraviolet (EUV) semiconductor lithography tools to chip manufacturers that enable them to accelerate capacity expansion.

On the fourth-quarter 2025 earnings call, ASML Holding’s management noted that its customers have become more confident about medium-term AI demand, leading to stronger order intake and investment plans as chipmakers transition from 4 nanometers to 3 nanometers and prepare for the 2-nanometer transition.

As EUV intensity per wafer continues to rise, AI and HPC workloads are addressed more efficiently. In memory, robust demand for HBM and advanced DRAM nodes is expected to tighten supply through at least 2026, supporting EUV demand.

ASML is also benefiting from a growing installed base, which is driving high-margin service and upgrade revenues as customers increasingly view upgrades as the fastest way to add capacity. With a €38.8 billion backlog and reaffirmed long-term targets, ASML remains well-positioned to capitalize on the AI-led semiconductor investment cycle.

In the last reported financial results for the fourth quarter of 2025, ASML Holding’s total net sales increased 4.9% year over year to €9.72 billion. Converted to USD, ASML’s fourth-quarter revenues were $11.31 billion, which surpassed the Zacks Consensus Estimate by 1.79%. Earnings increased 7.3% to €7.34 per share. In USD, fourth-quarter 2025 EPS were $8.55, which missed the Zacks Consensus Estimate by 5.11%.

ASML Holding N.V. price-consensus-eps-surprise-chart | ASML Holding N.V. Quote

Looking at the Zacks Consensus Estimate for revenues and EPS, Lam Research has a better long-term growth profile than ASML Holding. The consensus mark for Lam Research’s fiscal 2026 and 2027 revenues indicates year-over-year growth of 20% and 22.2%, respectively. Non-GAAP EPS is expected to rise 27.1% in fiscal 2026 and 25.6% in fiscal 2027.

Estimates for ASML Holding’s 2026 revenues and EPS suggest growth of 17.1% and 20.3%, respectively. For 2027, revenues are anticipated to rise 18.9%, while EPS is forecasted to soar 23.2%.

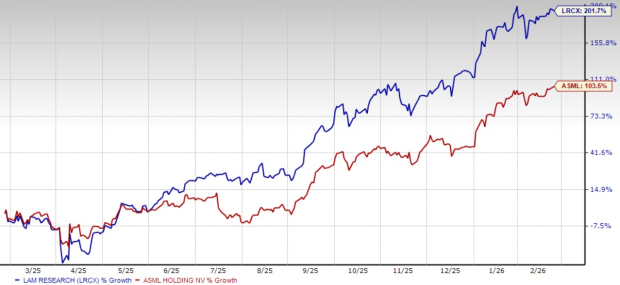

Over the past year, shares of Lam Research and ASML Holding have surged 201.7% and 103.5%, respectively.

On the valuation front, Lam Research trades at 39.45 times forward earnings compared to 42.70 times for ASML Holding. While both companies are of high quality, LRCX looks more reasonably priced, especially considering its stronger earnings growth projections.

Both Lam Research and ASML Holding are set to benefit from the AI-driven semiconductor investment cycle. However, Lam Research’s broader exposure to high-growth AI and memory markets, coupled with a lower valuation, gives it the edge for investors seeking stronger upside potential.

Currently, Lam Research sports a Zacks Rank #1 (Strong Buy), making the stock a must-pick compared to ASML Holding, which has a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 35 min | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 |

Lam Research Stock Jumps On Fiscal Q4 Beat-And-Raise Report

LRCX -6.40% LRCX +6.40% AH

Investor's Business Daily

|

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-28 | |

| Jul-28 | |

| Jul-28 | |

| Jul-28 | |

| Jul-28 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite