|

|

|

|

|||||

|

|

|

Both Western Digital Corporation WDC and Teradata TDC are tied to enterprise data infrastructure, with WDC providing the physical storage hardware, and Teradata delivering data analytics and cloud-based data platform solutions that rely on large-scale storage systems.

Per a report from Precedence Research, the global data center infrastructure market is estimated to go from $5.08 billion in 2026 to roughly $19.04 billion by 2035 at a CAGR of 15.86%. Rising demand for digital services and data storage is driving strong growth in the data center market. The ecosystem spans hardware, software and service providers that build and operate these facilities, continually evolving to deliver faster, more reliable and efficient processing and storage for businesses.

To help investors decide which data infrastructure stock might be a better buy, let’s break this down across business models, growth drivers, financial performance, risks, valuations and investment outlook.

WDC is a hardware infrastructure company specializing in storage technologies, especially HDDs, enterprise SSDs and flash solutions, which are core to data centers, cloud providers and AI workloads. Its products help store the vast amounts of data being generated daily by enterprises and AI systems. The company has also spun off its flash business (Sandisk) to sharpen its focus on core storage segments. At Innovation Day 2026, Western Digital, now rebranded as WD, reinforced that hard drives remain vital, positioning them as a core component of AI infrastructure.

The company introduced a new three-to-five-year financial model and updated its branding to reflect its data-center focus, as surging AI workloads fuel demand for high-capacity, reliable storage to handle massive datasets. Over the next three-five years, WD targets revenue growth above 20% CAGR, driven by nearline enterprise demand expanding at a mid-20s pace and supported by stable pricing. The model calls for gross margins exceeding 50% through a richer mix of higher-capacity HDDs and ongoing cost improvements, while operating margins above 40% are expected from strong operating leverage.

With disciplined working-capital management and CapEx maintained at 4–6% of revenue, free cash flow margins are projected to surpass 30%. This financial leverage, combined with share repurchases, positions EPS to rise beyond $20, underscoring a strategy built on execution, technology leadership and sustained, durable growth.

To handle AI-driven data growth, WD unveiled a customer-centric roadmap focused on scalable capacity, higher performance and better power efficiency while preserving HDD cost advantages. It reaffirmed its dual ePMR–HAMR strategy, with 40TB UltraSMR drives now qualifying at two hyperscalers for volume production in the second half of fiscal 2026, and HAMR set to ramp in 2027. The roadmap extends ePMR to 60TB and scales HAMR to 100TB by 2029, leveraging a common architecture to boost manufacturing efficiency and allow seamless customer transitions.

Beyond large language models, the rise of Agentic AI across industries is driving strong demand for unstructured data storage. These AI agents, tailored for specific tasks, from enterprise chatbots to engineering support, are creating new use cases and generating data at an unprecedented rate. The company is already seeing real benefits from Agentic AI in accelerating product development. As AI adoption grows, so does the need for scalable, cost-effective storage.

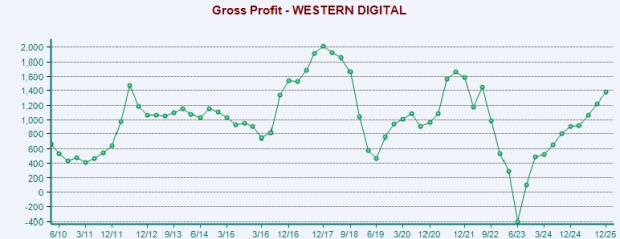

Western Digital continues to prioritize shareholder returns and strategic investments, declaring a cash dividend of 12.5 cents per share on its fiscal second-quarter earnings call. Strong execution drove robust cash generation, with operating cash flow rising to $745 million from $403 million a year ago and free cash flow jumping 95% to $653 million. The company returned more than 100% of this free cash flow through dividends and share repurchases, highlighting solid margins, disciplined capital allocation and confidence in future cash generation.

However, near-term risks are rising from tariffs and trade tensions that could disrupt enterprise and retail demand. At the same time, higher-capacity drives are increasing manufacturing complexity and cycle times. WD’s elevated leverage also limits financial flexibility, with $2 billion in cash against $4.7 billion in long-term debt as of Jan. 2, 2026.

TDC is a software-focused data analytics provider. It helps enterprises manage, analyze and derive insights from data via its Teradata Vantage platform, hybrid cloud analytics, consulting services and increasingly AI integration, making data usable and intelligent across environments. Teradata exited 2025 on a strong note and laid out a 2026 plan centered on operationalizing AI in hybrid environments, launching new products and delivering 2–4% ARR growth with $310–$330 million in free cash flow. Management remains confident in its hybrid AI platform and continued innovation, while flagging seasonality and the shifting cloud/on-prem mix.

Growing workloads on data platforms due to Agentic AI’s 24/7, always-on query potential bodes well for TDC’s prospects, as it not only manages the critical enterprise data that powers these AI systems but is also well-positioned to deliver the performance required by these AI systems. Teradata believes that it offers the best autonomous AI and knowledge platform for Agentic workloads at the best price performance, whether on-premises or in the cloud. An innovative portfolio that includes QueryGrid data analytics fabric, Enterprise Vector Store, AgentBuilder, and ClearScape Analytics with unified ModelOps capabilities is expected to drive top-line growth.

Teradata has partnered with the three leading public cloud providers—AWS, Microsoft Azure and Google Cloud—expanding global access to VantageCloud. It also teamed up with ActionIQ to deliver a joint solution that gives customers deeper control and a unified 360-degree view of their data, enabling more personalized engagement and improved user experiences. Acquisitions, such as Stemma, enhance Teradata's capabilities in data search and exploration, providing added value to its analytics offerings. Teradata has introduced innovative AI capabilities like ask.ai, which are designed to simplify natural language interactions.

In February, Teradata launched its enterprise-grade Data Analyst AI agent on Google Cloud Marketplace, allowing customers to deploy advanced analytics directly within their cloud environment. Built on the Teradata Enterprise MCP and Google’s Agent Development Kit, the agent enables conversational analytics, secure in-place processing and real-time insights without costly data movement, speeding time to value for AI-driven decisions.

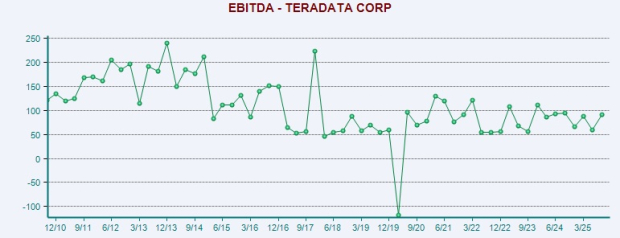

Teradata’s VantageCloud is gaining traction with large, data-heavy enterprises. In fourth-quarter 2025, public-cloud ARR grew 13% year over year in constant currency to $701 million, fueled by rising cloud adoption. The company is continuously enhancing Vantage across both cloud and on-premises to deliver a high-performance, massively scalable hybrid analytics platform. It also has a strong balance sheet, and improving ARR growth with cost savings is expected to drive free cash flow. In the fourth quarter, TDC generated $160 million in cash from operating activities compared with the previous quarter’s $94 million.

However, Teradata projects modest 2026 performance, with recurring revenue expected to range from flat to up 2% and total revenue estimated to fall 2% to remain flat in constant currency, signaling limited near-term growth. Its shift toward higher-margin, Vantage-led engagements is weighing on consulting revenue and profitability in the short term. Competition from financially stronger and more diversified players like IBM and Oracle is intensifying pricing pressure, further constraining margins.

Over the past year, TDC and WDC have registered gains of 472.1% and 16.1%, respectively.

Going by the price/earnings ratio, TDC’s shares currently trade at 16.01 forward earnings, lower than 21.78 for WDC.

The Zacks Consensus Estimate for TDC’s earnings for fiscal 2026 has been revised north 2.8% to $2.55 over the past 60 days.

The Zacks Consensus Estimate for WDC’s earnings for fiscal 2026 has been revised up 17% to $8.96 over the past 60 days.

Western Digital may offer stronger growth potential linked to AI/cloud storage infrastructure with robust financials and strong demand signals. Teradata provides stable software margins and cloud transition potential, but faces a tougher competitive environment and more modest growth. Teradata offers value, but expects slower growth and more competition. It may suit investors looking for a diversified tech play with recurring cloud revenue rather than hardware exposure.

Western Digital’s role in the AI-driven storage wave, strong revenue growth, share buybacks and cloud demand position it as an appealing buy for investors who believe data volume will keep exploding. WDC at present flaunts a Zacks Rank #1 (Strong Buy), while TDC has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-28 | |

| Jul-28 | |

| Jul-28 | |

| Jul-28 | |

| Jul-28 | |

| Jul-28 | |

| Jul-28 | |

| Jul-28 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite