|

|

|

|

|||||

|

|

|

The mechanical and electrical market continues to benefit from strong demand trends in data centers, infrastructure and industrial construction. Names like Comfort Systems USA, Inc. FIX and EMCOR Group, Inc. EME are being highlighted amid the favorable fundamentals, highlighting strong backlogs and improving profitability.

Comfort Systems offers installation and contracting services across the HVAC market and is currently focused on seeking opportunities for large-scale projects and investing additional capital in inorganic growth initiatives. Conversely, EMCOR offers mechanical and electrical construction, industrial and energy infrastructure services, with its main focus on streamlining its U.S. operations.

Let’s dive deep and closely compare the fundamentals of the two stocks to determine which one is a better investment now.

Comfort Systems is gaining from a robust public spending scenario in the United States, mainly due to its exposure to large-scale projects. Strong project activity and robust execution across its mechanical and electrical businesses are the main highlights, thanks to modular expansion and substantial organic construction and service growth. As of Dec. 31, 2025, backlog stood at $11.94 billion, up year over year by 99.3% from $5.99 billion. Within the total backlog, the Mechanical Segment contributed 75.6% while the Electrical Segment contributed 24.4%.

The previously announced acquisitions of Feyen-Zylstra Holdings, LLC (Michigan) and Meisner Electric, Inc. (Florida) are an encouraging step toward expanding its market footprint. The transactions were made on Oct. 1, 2025, and are included in its Electrical segment. In 2025, FIX’s revenues grew 29.5% year over year, which included a 3.4% increase related to the Feyen Zylstra, Meisner, Right Way, Century, Summit and J&S acquisitions.

Notably, the Technology end market, which is dominated by data center work, was 45% of FIX’s 2025 revenues, an increase from 33% in 2024. Currently, the company’s modular capacity is about 3 million square feet, which is expected to increase to approximately 4 million square feet by the end of 2026, with planned additions in Texas and North Carolina. Comfort Systems is consistently working on expanding its modular footprint, alongside investing in technology, equipment and training for its amazing workforce.

The operational momentum, disciplined bidding and favorable project mix continue to fuel growth for Comfort Systems. In 2025, the company paid its shareholders $217.9 million through share repurchases and $68.8 million through dividends. Also, it declared a quarterly dividend of 70 cents per share ($2.80 per share annually), reflecting 16.7% growth. It is payable on March 17, 2026, to stockholders as of March 6.

However, Comfort Systems’ growing exposure to hyperscale data centers is a double-edged sword. Any slowdown in AI-driven capital expenditures, project deferrals by cloud providers or power availability constraints could compress backlog growth and utilization.

EMCOR is also benefiting from the robust trends in the United States public infrastructure market. Its two major segments, the US Electrical and Mechanical Construction and Facilities Services segments, are consistently displaying significant strength amid positive market fundamentals.

As of Sept. 30, 2025, Remaining Performance Obligations (RPOs) were $12.61 billion, indicating 29% year-over-year growth and 25% from Dec. 31, 2024. Increased activity within the network and communications sector, mainly driven by data center construction projects demand trends, with other sectors including healthcare, commercial, manufacturing and industrial, and the high-tech manufacturing sectors are boding well. The diversity in EMCOR’s RPOs is stabilizing its revenue visibility and profitability structure despite ongoing macro uncertainties.

Besides the market’s favorable fundamentals, EME is currently focusing on divesting its U.K. business and streamlining its U.S. operations for better execution across highly profitable markets. In September 2025, EMCOR announced the divestiture of its U.K. Building Services segment, which was completed in December 2025. The segment was acquired by OCS Group UK Limited for a total value of approximately $250 million. This strategic transaction offers EMCOR further financial flexibility to expand its business by redirecting the proceeds into strategic M&A, prefabrication capacity and U.S. project expansion.

Notably, EMCOR’s acquisition strategies are directed toward buying small private firms with proven management and expansion potential. On Feb. 3, 2025, the company acquired Miller Electric Company, which specializes in designing, installing and maintaining complex electrical systems across sectors such as data centers, manufacturing and healthcare. Being officially considered under the U.S. Electrical Construction and Facilities Services segment, this strategic addition has complemented EMCOR’s existing electrical construction capabilities in high-growth end markets while expanding its geographic presence.

As witnessed from the chart below, in the past six months, Comfort Systems’ share price performance stands significantly above EMCOR’s and the broader Construction sector.

Considering valuation, over the last five years, Comfort Systems has been trading above EMCOR on a forward 12-month price-to-earnings (P/E) ratio basis.

Overall, from these technical indicators, it can be deduced that FIX stock offers an incremental growth trend but with a premium valuation, while EME stock offers a diminishing growth trend with a discounted valuation.

The Zacks Consensus Estimate for FIX’s 2026 EPS indicates 6% year-over-year growth. The 2026 EPS estimate has remained stable in the past 60 days.

FIX's EPS Trend

The Zacks Consensus Estimate for EME’s 2026 earnings estimates implies year-over-year growth of 8.6%. Its 2026 EPS estimates have trended upward over the past 30 days.

EME's EPS Trend

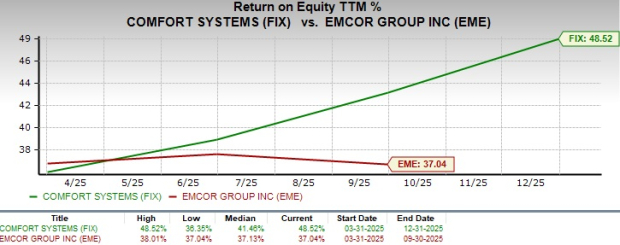

Comfort Systems’ trailing 12-month ROE of 48.5% significantly exceeds EMCOR’s average, underscoring its efficiency in generating shareholder returns.

Both Comfort Systems and EMCOR operate in a favorable mechanical and electrical construction environment, supported by strong demand for data centers, infrastructure and industrial projects.

Comfort Systems, which currently has a Zacks Rank #3 (Hold), continues to benefit from robust backlog growth and expanding exposure to data center construction, which accounted for a significant portion of 2025 revenues. However, the stock trades at a premium valuation after a sharp rally, and heavy reliance on hyperscale data center spending introduces concentration risk if AI-related capital expenditures moderate.

On the other hand, EMCOR, which currently carries a Zacks Rank #2 (Buy), offers more balanced growth supported by diversified RPOs, improving profitability across its U.S. operations and strategic initiatives, which are expected to enhance operational efficiency and long-term growth. EMCOR also trades at a more reasonable valuation and benefits from upward earnings estimate revisions, indicating improving analyst sentiment.

As FIX stock stands out as the higher-growth contractor, EME stock offers a more balanced and diversified growth story. Thus, investors can consider EMCOR stock as it appears to be better positioned for near-term upside compared with Comfort Systems stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-24 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-20 | |

| Jul-17 | |

| Jul-16 | |

| Jul-09 | |

| Jul-01 | |

| Jun-30 | |

| Jun-23 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite