|

|

|

|

|||||

|

|

|

SoundHound AI, Inc. SOUN is scheduled to report its fourth-quarter 2025 results on Feb. 26, 2026, after market close.

In the last reported quarter, SoundHound delivered strong results, reflecting accelerating enterprise adoption and diversified growth. Revenue rose 68% year over year to $42 million and beat the Zacks Consensus Estimate by 4.9%, driven by expansion across financial services, healthcare, restaurants and IoT, despite ongoing softness in automotive markets. The company raised its 2025 revenue outlook to $165–$180 million, signaling confidence in sustained momentum.

Non-GAAP gross margin remained robust at 59.3%, supported by efficiencies and greater use of proprietary models. The company reported a non-GAAP net loss of 3 cents per share, narrower than the Zacks Consensus Estimate of a loss of 4 cents and the year-ago loss of 4 cents per share. While adjusted EBITDA reflected continued investment, management emphasized improving scale dynamics and a strong liquidity position, ending the quarter with $269 million in cash and no debt.

This maker of artificial intelligence (AI) tools for computer interpretation of voice commands surpassed earnings estimates in three of the trailing four quarters and missed on the other occasion, with an average negative surprise of 109.5%. You can see the historical figures in the chart below.

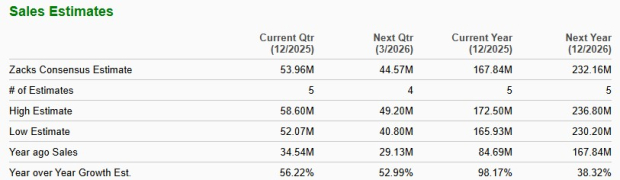

The Zacks Consensus Estimate for the fourth-quarter bottom line has remained unchanged at a loss of 2 cents per share over the past 60 days. The company reported a year-ago loss per share of 69 cents. The consensus mark for revenues is pegged at $54 million, suggesting a 56.2% year-over-year increase.

For 2026, SOUN is expected to register a 38.3% increase from a year ago in revenues to $232.2 million. Its bottom line is expected to witness an improvement to a loss of 6 cents per share from an estimated 13 cents for 2025.

SOUN’s Earnings Estimate

SOUN’s Revenue Estimate

Our proven model does not conclusively predict an earnings beat for SoundHound for the quarter to be reported. That is because a stock needs to have both a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy), or 3 (Hold) for this to happen. This is not the case here, as you will see below.

Earnings ESP: SoundHound has an Earnings ESP of 0.00%. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Zacks Rank: The company currently carries a Zacks Rank #3.

You can see the complete list of today’s Zacks #1 Rank stocks here.

On the topline front, fourth-quarter performance is likely to have been supported by continued traction in enterprise AI, which management has identified as one of the largest near-term opportunities. The Amelia platform and the company’s Agentic+ framework are being positioned as enterprise-grade solutions that balance generative AI with deterministic controls, a feature set aimed at accelerating production deployments. Management raised its 2025 revenue outlook to a range of $165 million to $180 million during the third-quarter earnings call, implying a solid contribution from the December quarter. Expansion within financial services, healthcare, insurance, telecom and energy, along with renewals and upsells, likely aided recurring revenue visibility.

Restaurant deployments of Smart Ordering, Employee Assist and Voice Insights solutions may also have supported growth, particularly as franchise wins and national chain rollouts scale. Additionally, progress in IoT and smart device integrations, including large-volume device commitments, could have contributed incremental revenue as deployments ramped.

However, automotive softness remains a potential headwind. Management has previously highlighted industry-wide pressures, including tariff-related impacts and broader vehicle production trends. If these conditions persisted into the fourth quarter, they may have weighed on growth within the automotive vertical, partially offsetting strength elsewhere.

From a profitability standpoint, gross margins may have benefited from greater adoption of proprietary technologies such as Polaris, which are designed to reduce reliance on third-party models and lower cloud costs. Ongoing acquisition integration efforts and cost synergies are likely to have further supported margin expansion. At the same time, elevated investments in research and development, go-to-market expansion and enterprise sales capabilities may have continued to pressure operating income.

Management has indicated that as it exits 2025 and enters 2026, it expects continued high growth alongside a transition toward a breakeven profitability profile. The fourth-quarter results will therefore be critical in demonstrating whether scale efficiencies are beginning to meaningfully narrow adjusted losses while sustaining robust revenue momentum.

SOUN shares have gained 53.4% in the past six months, underperforming the Zacks Computers - IT Services industry, the broader Zacks Computer & Technology sector and the S&P 500 index, as shown below.

SOUN Stock’s Performance

SoundHound operates in a competitive voice and conversational AI market alongside established players such as Nuance Communications of Microsoft MSFT, Cerence Inc. CRNC and NICE Ltd. NICE. Nuance remains a formidable force in enterprise and healthcare AI, leveraging deep clinical and customer-service integrations. Nuance’s scale and Microsoft backing intensify pricing and platform competition. Cerence, heavily focused on automotive voice assistants, directly overlaps with SoundHound in connected vehicle deployments, making Cerence a persistent rival as automakers streamline vendors. Meanwhile, NICE dominates contact-center AI, where NICE’s CX platform competes with SoundHound’s Amelia offerings. As Nuance, Cerence and NICE expand generative and agentic capabilities, competitive differentiation will hinge on speed, accuracy and cost efficiency.

SOUN shares are currently slightly overvalued. In terms of its forward 12-month price-to-sales (P/S) ratio, SOUN is trading at 13.73, higher than the Zacks Computers - IT Services industry, as shown below.

SOUN’s P/S Ratio (Forward 12-Month) vs. Industry

The company continues to post strong revenue momentum, with the Zacks Consensus Estimate implying 56% year-over-year growth for the December quarter and further expansion projected in 2026. Enterprise adoption across financial services, healthcare and restaurants, along with scalable platforms like Amelia and Agentic+, supports long-term growth visibility. Gross margins remain healthy, and a solid liquidity position of $269 million in cash with no debt provides financial flexibility.

That said, ongoing automotive softness, elevated investments pressuring near-term profitability and premium valuation levels warrant caution. Investors may stay on the sidelines until clearer evidence of sustained profitability and competitive edge emerges.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours | |

| 4 hours | |

| 4 hours | |

| 4 hours | |

| 4 hours | |

| 5 hours | |

| 6 hours | |

| 6 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite