|

|

|

|

|||||

|

|

|

Opendoor Technologies Inc.’s OPEN fourth-quarter 2025 earnings call made one thing clear: the company is no longer chasing growth at any cost. Instead, Opendoor 2.0 is deliberately slowing the top line to fix the engine underneath. After years of volatile margins and inventory risk, management is now prioritizing product quality, unit economics, and resale velocity over headline volume.

The strongest evidence comes from the October 2025 acquisition cohort, the first fully under the Opendoor 2.0 model. This cohort is shaping up to be the most profitable October in company history, despite operating in a weak housing market. Faster sell-through, lower margin degradation, and improved contribution margins suggest structural changes, not market luck, are driving results. Management emphasized that Opendoor is shifting from acting like a proprietary trader to behaving more like a market maker, focused on speed and precision rather than spread maximization.

Crucially, leadership is choosing to invest engineering resources into foundational products such as mortgage, pricing, and automation rather than pushing acquisition volumes to the top end of targets. The rationale is simple: better products create durable fuel for future growth. AI-driven underwriting, flexible seller offerings like Cash Plus and tighter control over days-in-inventory are already reducing risk and capital intensity.

Near-term revenue may remain uneven as legacy inventory clears, but margins are improving sequentially, and cost discipline is holding. If Opendoor can sustain these trends, Opendoor 2.0 looks less like a reset and more like a genuine turnaround built for profitability first, and growth later.

Opendoor’s product-first reset stands out when compared with other publicly traded real estate technology platforms facing similar profitability pressures. Zillow Group Z exited its iBuying business after volatile inventory outcomes and has since leaned into a capital-light marketplace model. Zillow’s strategy prioritizes software, agent tools, and customer engagement over balance-sheet exposure, reducing risk but limiting participation in transaction-level upside.

Another relevant competitor is Compass COMP. The company has shifted its focus toward cost discipline, agent productivity, and proprietary technology to improve margins after years of aggressive expansion. Rather than owning homes, Compass uses technology to support agents and drive efficiency, making profitability more dependent on housing volumes and commission structures.

Compared with Zillow and Compass, Opendoor’s Opendoor 2.0 approach is more operationally complex. By retaining a transaction-based model while fixing pricing accuracy, resale velocity, and capital efficiency, Opendoor is betting that stronger product fundamentals today will enable more sustainable growth tomorrow.

Shares of Opendoor have gained 5.3% in the past six months against the industry’s decline of 20.7%.

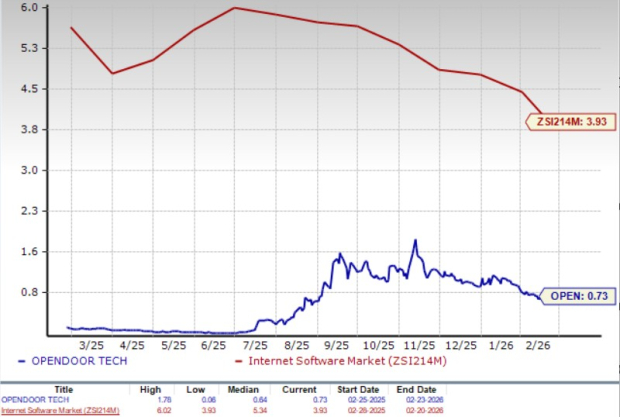

From a valuation standpoint, OPEN trades at a forward price-to-sales (P/S) multiple of 0.73, significantly below the industry’s average of 3.93.

The Zacks Consensus Estimate for OPEN’s 2026 loss per share has narrowed to 21 cents in the past 30 days, as shown below. Also, the estimated figure indicates a narrower loss from the year-ago loss of 26 cents per share.

OPEN currently has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-07 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite