|

|

|

|

|||||

|

|

|

Both Seagate Technology Holdings plc STX and NetApp, Inc. NTAP are tied to enterprise storage demand, with STX focused on hardware drives and NTAP specializing in data management and hybrid cloud storage.

Per a report from Fortune Business Insights, the global data storage market is projected to go from $298.5 billion in 2026 to $984.6 billion by 2034 at a CAGR of 16%. A report from Mordor Intelligence estimates that the HDD market will expand from $51.8 billion in 2026 to $69.7 billion by 2031 at a CAGR of 6%. It projects that the enterprise flash storage market will expand from $29.04 billion in 2025 at a 11.42% CAGR to $49.87 billion by 2030.

STX and NTAP stand to benefit from AI-driven data center expansion, as higher data workloads increase demand for scalable storage infrastructure. For investors seeking diversification, holding both provides exposure to the entire storage ecosystem that underpins AI and cloud computing. If a single choice is necessary, the decision essentially hinges on value versus growth, your investment horizon and how you see the evolution of data infrastructure.

Let’s break it down in more detail.

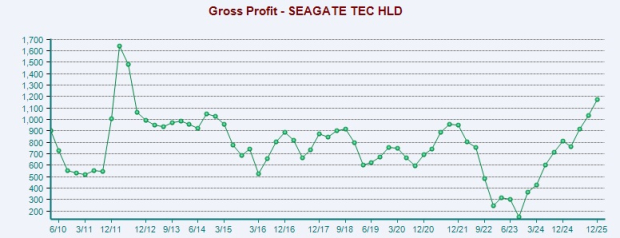

Seagate is fundamentally a hardware storage company, specializing in HDDs, enterprise nearline storage and mass capacity solutions for data centers and hyperscalers. It has been benefiting from rising demand for data storage driven by AI, cloud and big data workloads. Seagate’s revenue swings can be larger because hardware demand, especially HDDs, tends to be cyclical and tied to enterprise capex and hyperscaler orders. Fiscal second-quarter revenue reached $2.83 billion, topping the guidance midpoint and rising 22% year over year, driven by strong nearline cloud demand and improving enterprise edge trends, momentum that the company expects to continue on a solid build-to-order pipeline.

Seagate expanded its non-GAAP gross margin above 42%, supported by its pricing strategy and increased adoption of high-capacity drives as HAMR shipments ramped up. HAMR technology is highlighted as a key enabler for mass capacity storage. The company is progressing with its second-generation Mozaic 4-terabyte-per-disk products and aims to achieve 10 terabytes per disk early in the next decade. Seagate's nearline capacity is fully allocated through 2026, with demand visibility strengthening for 2027 and discussions underway for 2028.

It plans to meet growing demand through advancements in areal density rather than increasing production volume. Seagate is benefiting from strong demand for video applications, cloud data storage and emerging AI-driven applications, which are driving significant data creation and storage needs. The company is focused on expanding profitability through higher capacity product mixes and leveraging HAMR technology to improve total cost of ownership (TCO) and efficiency for customers.

Furthermore, Seagate’s strong cash flow supports investment in innovation, acquisitions and growth initiatives, while funding consistent dividends and share buybacks to deliver risk-adjusted shareholder returns. In the December quarter, it returned $154 million to shareholders via dividends and retired about $500 million of exchangeable senior notes due 2028, reducing potential dilution and preserving cash flexibility for future share repurchases. It expects free cash flow to increase further in the March quarter, driven by strong demand, operational efficiency and disciplined capital spending, supporting sustainable long-term cash generation.

STX will maintain capital discipline while continuing the HAMR technology transition and ramp-up, with fiscal 2026 capital spending expected to remain within its target range of 4–6% of revenue. Seagate's business model changes and strong product pipeline position it well for improved profitability and cash flow in fiscal 2026.

However, Seagate is struggling with forex fluctuations, stiff competition and persistent macro and supply-chain uncertainty. Its elevated debt load adds financial risk and reduces flexibility for share repurchases, dividends and M&A, potentially constraining long-term growth. As of Jan. 2, 2026, the company held $1.05 billion in cash and cash equivalents against $4.5 billion in long-term debt, including the current portion.

NetApp provides enterprise storage as well as data management software and hardware products and services. Growth in all-flash storage, public cloud and AI solutions is driving NTAP’s performance. The company continues to roll out innovative products, enhanced cybersecurity and expanded cloud capabilities, positioning itself for continued growth despite macroeconomic challenges. It earns substantial revenues from intelligent data management, all-flash arrays and hybrid cloud software (ONTAP) as enterprises modernize infrastructure.

NetApp is seeing strong customer traction for its modern all-flash portfolio, led by the C-series capacity flash and ASA block-optimized systems, with the newer A-series also gaining momentum. These platforms are designed to accelerate a wide range of workloads, from core enterprise applications to GenAI, and management expects them to drive additional share in the all-flash market. By the end of the fiscal second quarter, all-flash systems made up 46% of the installed base under active support contracts. All-Flash Array revenue grew 9% year over year to $1 billion, implying an annualized run rate of $4.1 billion, while total billings increased 4% to $1.65 billion.

Cybersecurity remains a board-level priority. NetApp expanded its ransomware resilience capabilities with AI-powered breach detection, isolated recovery environments and proactive threat identification. These enhancements reinforce its value proposition in regulated industries where data protection is mission-critical. The release of StorageGRID 12.0 further supports unstructured data growth and AI initiatives, while strengthening object storage scalability and security. It is strengthening its cloud-native ecosystem with Trident 25.10, an expanded Shift Toolkit, and bidirectional VMware–Hyper-V migration, keeping the platform relevant for containerized and hybrid enterprise environments.

NetApp’s Keystone storage-as-a-service solution is gaining broad-based adoption. The enhanced NetApp Keystone Storage-as-a-Service (STaaS) offering now supports AI use cases through a consumption-based model. Keystone revenues grew 76% year over year in the fiscal second quarter. This led to a 13.8% jump in Professional Services revenues to $99 million. With $456 million in unbilled RPO (indicator for Keystone performance), up 39% year over year, the pipeline for Keystone remains robust.

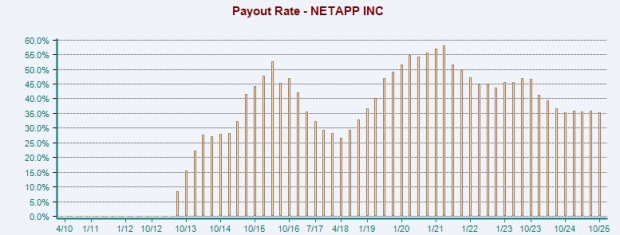

NTAP also sustains strong buybacks and a reliable dividend, supported by solid free cash flow. The company returned $353 million to its shareholders as dividend payouts and share repurchases in the fiscal second quarter. NetApp returned $250 million to its shareholders through share repurchases and distributed $103 million in dividends. The company returned $1.57 billion to its shareholders as dividend payouts and share repurchases in fiscal 2025. NetApp’s ability to generate solid free cash flow is expected to help it sustain the current dividend payout (0.35) level, at least in the near term.

However, NetApp remains cautious on spending due to an uncertain macro backdrop, with weakness in the U.S. public sector and EMEA keeping fiscal second-quarter revenue flat and expected to remain a headwind in the second half. Full-year fiscal 2026 revenue is projected at $6.625–$6.875 billion. Storage refresh cycles could be delayed if conditions worsen, pressuring the top line. The company’s active acquisition strategy is expanding growth opportunities but raising integration risk and driving goodwill and intangibles to 28.6% of total assets.

Over the past year, STX has registered gains of 294.9% while NTAP plunged 19.8%.

Going by the price/earnings ratio, NTAP’s shares currently trade at 14.49 forward earnings, compared with 24.82 for STX.

The Zacks Consensus Estimate for STX’s earnings for fiscal 2026 has been revised up 11.8% to $12.63 over the past 60 days.

The Zacks Consensus Estimate for NTAP’s earnings for fiscal 2026 has been revised down marginally to $7.91 over the past 60 days.

Seagate is benefiting from strong AI and cloud-driven mass-capacity HDD demand, record shipment growth, margin expansion and the long-term potential of HAMR, but remains exposed to hyperscaler capex cycles, higher debt and earnings volatility if storage demand weakens. NetApp, meanwhile, is gaining from hybrid-cloud and all-flash adoption, solid cloud-integrated data management and rising recurring software and services revenue that supports earnings visibility, though its growth is slower than more aggressive peers and it faces intense cloud competition and periodic guidance-related sentiment pressure.

STX at present sports a Zacks Rank #1 (Strong Buy), while NTAP has a Zacks Rank #3 (Hold). Consequently, in terms of Zacks Rank, STX seems to be a better pick. You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-24 | |

| Jul-24 |

Why Tesla, Google, and other Mag 7 stocks are losing billions in valuation

STX -6.75%

Yahoo Finance Video

|

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-20 | |

| Jul-20 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite