|

|

|

|

|||||

|

|

|

Persistent public funding momentum and resilient private market demand continue to shape the U.S. civil construction landscape, supporting activity across transportation, water systems and large-scale site development. Against this backdrop, Sterling Infrastructure, Inc. STRL and Granite Construction Incorporated GVA stand out as closely aligned infrastructure players positioned to benefit from multiyear project pipelines and disciplined execution strategies. Both companies have emphasized selective bidding, margin-focused growth and operational efficiency as key pillars of their long-term plans.

Granite has underscored strong public market demand and a robust project pipeline supported by infrastructure legislation, while Sterling is leveraging similar tailwinds in transportation and mission-critical site development tied to data centers and industrial expansion. With both companies highlighting quality backlog, execution discipline and margin expansion initiatives, the comparison becomes especially timely for investors evaluating infrastructure exposure.

Let’s dive deep and closely compare the fundamentals of the two stocks to determine which one is a better investment now.

This Texas-based infrastructure services provider continues to benefit from resilient demand across transportation, utilities and mission-critical site development. Strong activity in data centers, manufacturing and distribution facilities has reinforced momentum within its E-Infrastructure platform, positioning the company in higher-growth end markets tied to digital infrastructure and industrial expansion. A disciplined focus on complex, large-scale projects and execution reliability has supported steady operating performance as infrastructure investment remains constructive.

E-Infrastructure remains the primary growth engine. In the third quarter of 2025, revenues from data center projects increased more than 125% year over year, highlighting accelerating hyperscale demand. The company reported a $2.6 billion signed backlog during the period, up 64% year over year. Including negotiated awards and future phases associated with ongoing megaprojects, total potential work exceeds $4 billion, strengthening multi-year revenue visibility across mission-critical and industrial markets.

However, residential softness and permitting delays across certain large developments may create timing variability. Elevated project complexity and competitive bidding conditions also present execution risks, particularly as labor availability and input costs fluctuate, which could pressure margins if project timelines shift.

Looking ahead, the company expects its deep pipeline across data centers, e-commerce and manufacturing to sustain growth through 2026 and beyond. With large multi-phase projects advancing and customers maintaining capital commitments, Sterling appears positioned to extend its expansion trajectory while improving revenue durability.

This California-based civil construction and materials provider continues to benefit from resilient public infrastructure demand, supported by transportation funding and a disciplined bidding strategy. Granite has focused on pursuing higher-quality projects within its core markets, emphasizing best-value contract structures that improve collaboration and reduce execution risk. Its vertically integrated construction and materials platform further enhances operational control and margin potential across large-scale infrastructure projects.

The company ended the fourth quarter of 2025 with a record $7 billion in CAP, representing a 31.6% year-over-year increase and reflecting sustained bidding momentum across public markets. Best-value projects accounted for 48% of CAP, highlighting a continued shift toward risk-mitigated, higher-margin work. Construction segment revenues rose 14% year over year to $940 million in the quarter, demonstrating steady project conversion and improved portfolio quality. The expanding CAP provides solid revenue visibility as infrastructure funding remains supportive.

However, large and complex public projects carry execution and timing risks. Weather variability, evolving federal infrastructure legislation and differing burn rates between bid-build and best-value contracts may affect near-term revenue pacing. Continued integration of recent acquisitions and maintaining margin consistency remain important operational priorities.

Looking ahead, Granite expects continued revenue growth and margin expansion, supported by its high-quality CAP mix, ongoing materials investments and disciplined capital allocation strategy. With strong public funding visibility and a growing portfolio of collaborative projects, the company appears positioned to extend its operational momentum into the coming year.

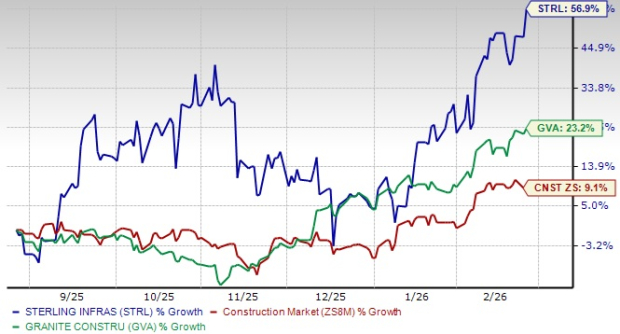

As witnessed from the chart below, in the past six months, Sterling’s share price performance stands above Granite’s and the broader Construction sector.

Considering valuation, over the past year, Sterling is trading above Granite on a forward 12-month price-to-earnings (P/E) ratio basis.

Overall, from these technical indicators, it can be deduced that STRL stock offers an incremental growth trend with a premium valuation, while GVA stock offers a slow growth trend with a discounted valuation.

The Zacks Consensus Estimate for STRL’s 2026 EPS has increased to $12.25 from $11.95 in the past 30 days. This indicates expected earnings rise of 17.2% year over year on projected revenue growth of 18.8%.

The Zacks Consensus Estimate for GVA’s 2026 EPS has decreased to $6.35 from $6.38 in the past 30 days. This indicates expected earnings growth of 16.2% year over year.

Sterling and Granite are both positioned to benefit from sustained U.S. infrastructure spending, but their near-term investment profiles differ. STRL’s growth story is increasingly tied to mission-critical development, particularly data centers and large industrial projects, supported by strong backlog expansion and accelerating revenue trends in its E-Infrastructure segment. Granite, meanwhile, offers greater exposure to public transportation and civil works, backed by a record CAP balance and an increasing mix of best-value, risk-managed contracts that enhance visibility and margin stability.

From an earnings momentum standpoint, Sterling appears to have the edge, with upward revisions to 2026 EPS estimates and stronger projected revenue growth. Granite’s estimates have edged lower, reflecting a more measured outlook despite solid operational momentum and improving portfolio quality.

With Sterling currently carrying a Zacks Rank #2 (Buy) and Granite a Zacks Rank #4 (Sell), the former stands out as the more compelling infrastructure stock at this time, particularly for investors seeking stronger earnings momentum and higher-growth exposure within the construction space.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-07 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-03 | |

| Aug-03 | |

| Jul-31 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-28 | |

| Jul-27 | |

| Jul-23 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite