|

|

|

|

|||||

|

|

|

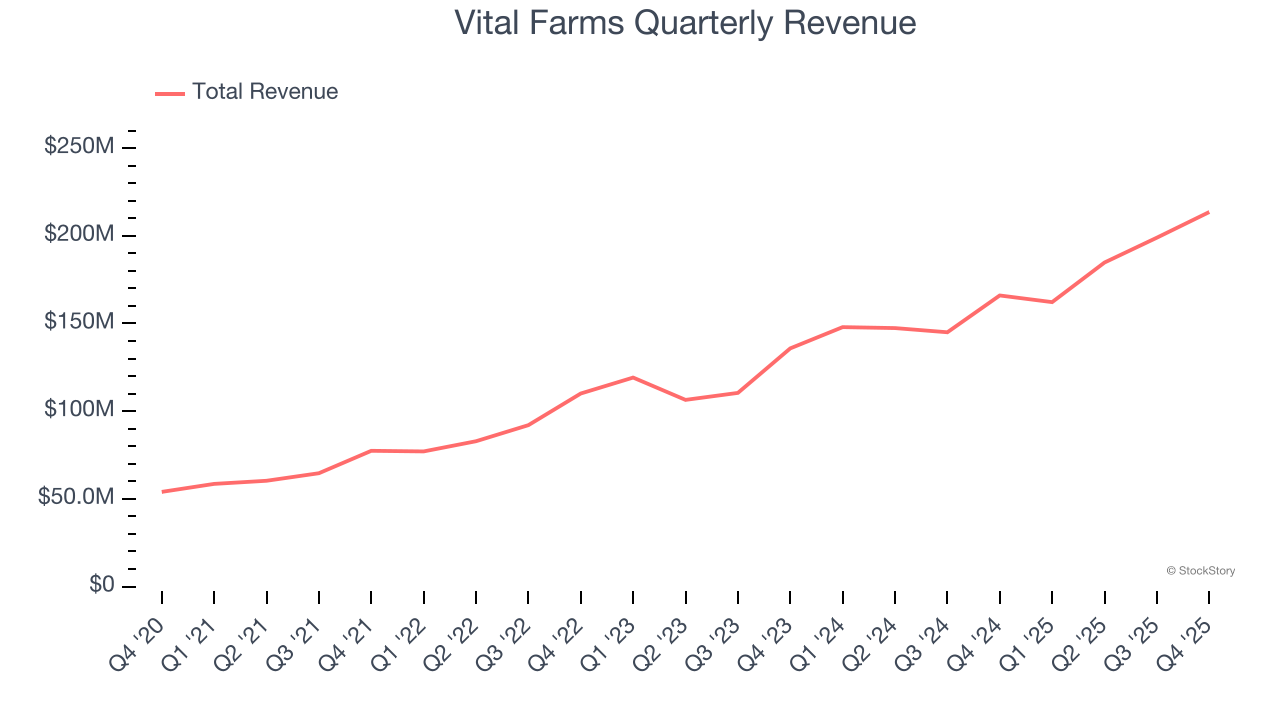

Egg and butter company Vital Farms (NASDAQ:VITL) met Wall Street’s revenue expectations in Q4 CY2025, with sales up 28.7% year on year to $213.6 million. On the other hand, the company’s full-year revenue guidance of $910 million at the midpoint came in 3.1% below analysts’ estimates. Its GAAP profit of $0.35 per share was 11% below analysts’ consensus estimates.

Is now the time to buy Vital Farms? Find out by accessing our full research report, it’s free.

"2025 was the year we scaled our supply chain to meet demand. By expanding Egg Central Station and growing our farmer network to over 600 small farms, we’ve meaningfully reduced the supply constraints that previously capped our growth,” said Russell Diez-Canseco, Vital Farms’ President and CEO.

With an emphasis on ethically produced products, Vital Farms (NASDAQ:VITL) specializes in pasture-raised eggs and butter.

A company’s long-term sales performance is one signal of its overall quality. Any business can have short-term success, but a top-tier one grows for years.

With $759.4 million in revenue over the past 12 months, Vital Farms is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers. On the bright side, it can grow faster because it has a longer list of untapped store chains to sell into.

As you can see below, Vital Farms grew its sales at an exceptional 28% compounded annual growth rate over the last three years as consumers bought more of its products.

This quarter, Vital Farms’s year-on-year revenue growth of 28.7% was excellent, and its $213.6 million of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 23.8% over the next 12 months, a deceleration versus the last three years. Still, this projection is commendable and suggests the market is forecasting success for its products.

While Wall Street chases Nvidia at all-time highs, an under-the-radar semiconductor supplier is dominating a critical AI component these giants can’t build without. Click here to access our free report one of our favorites growth stories.

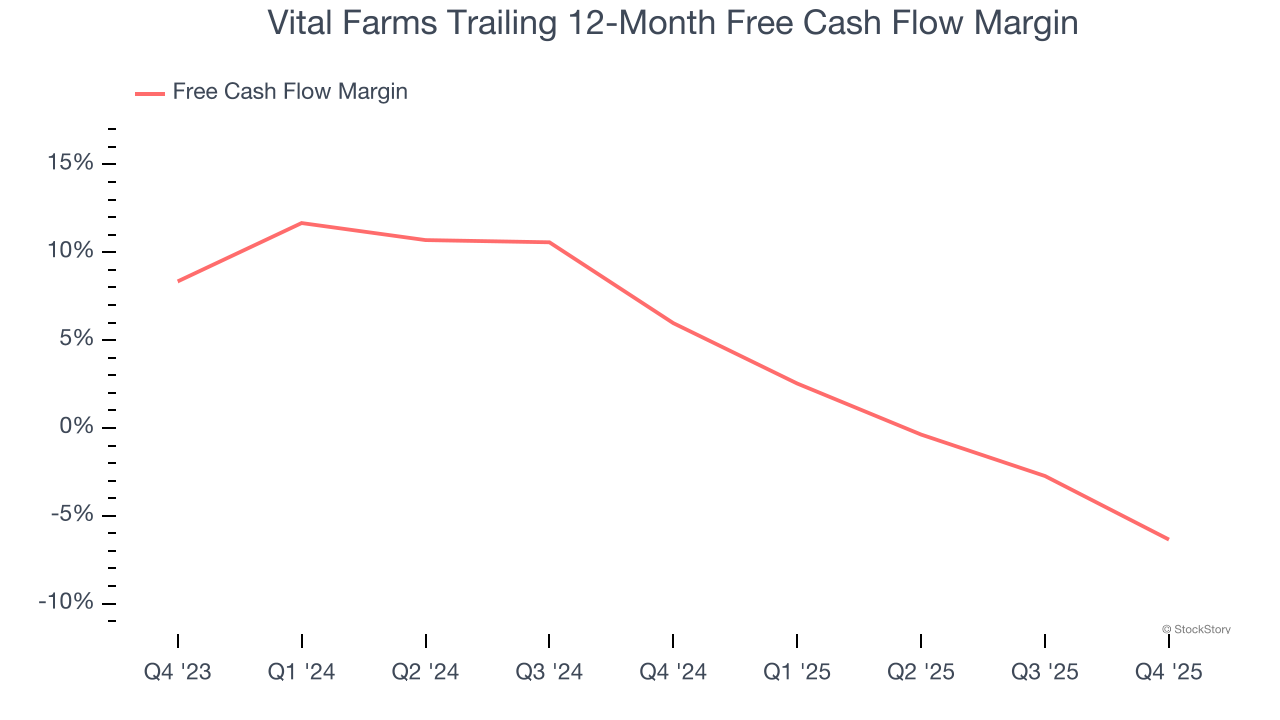

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Vital Farms broke even from a free cash flow perspective over the last two years, giving the company limited opportunities to return capital to shareholders. The divergence from its good operating margin stems from its capital-intensive business model, which requires Vital Farms to make large cash investments in working capital and capital expenditures.

Taking a step back, we can see that Vital Farms’s margin dropped by 12.3 percentage points over the last year. If the trend continues, it could signal it’s in the middle of a big investment cycle.

Vital Farms burned through $32.15 million of cash in Q4, equivalent to a negative 15.1% margin. The company’s cash burn increased from $3.38 million of lost cash in the same quarter last year.

We struggled to find many positives in these results. Its full-year revenue guidance missed and its full-year EBITDA guidance fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 2.9% to $24.08 immediately after reporting.

Vital Farms underperformed this quarter, but does that create an opportunity to invest right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).

| Jul-23 | |

| Jun-05 | |

| May-21 | |

| May-11 | |

| May-07 | |

| May-07 | |

| May-07 | |

| Apr-30 | |

| Apr-23 | |

| Apr-23 | |

| Apr-23 | |

| Apr-16 | |

| Apr-09 | |

| Apr-07 | |

| Apr-03 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite