|

|

|

|

|||||

|

|

|

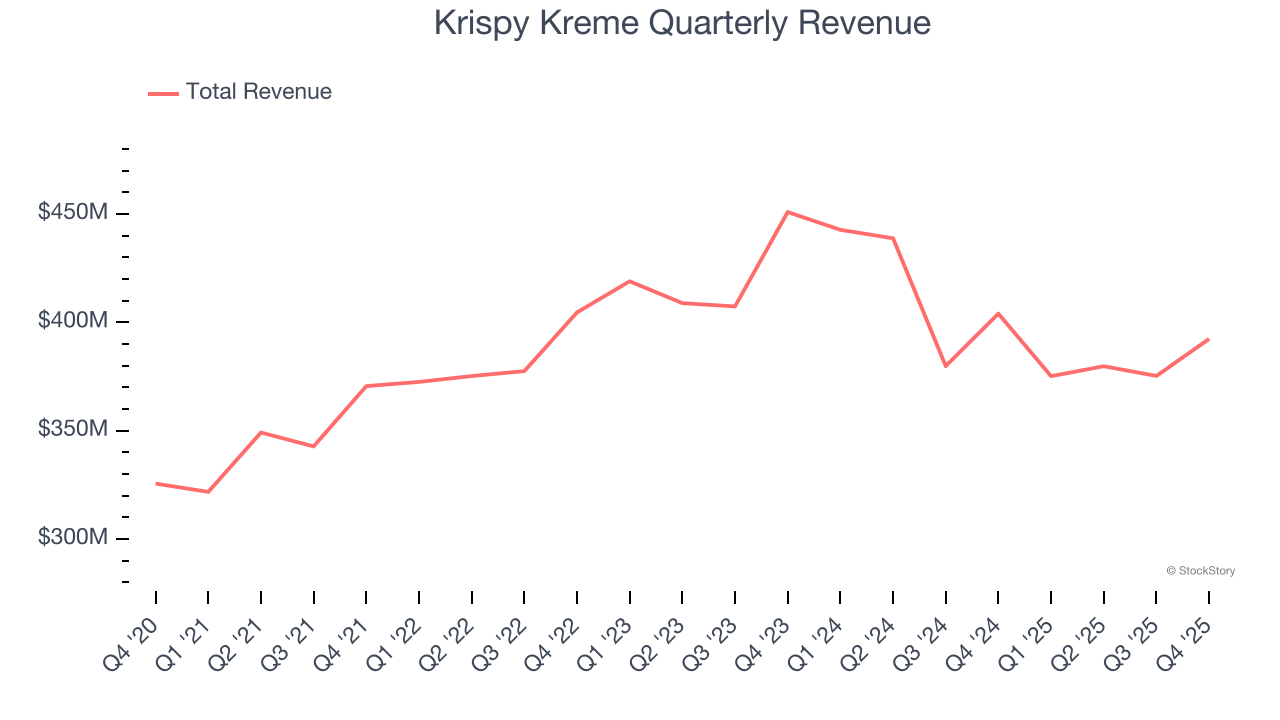

Doughnut chain Krispy Kreme (NASDAQ:DNUT) reported Q4 CY2025 results exceeding the market’s revenue expectations, but sales fell by 2.9% year on year to $392.4 million. Its non-GAAP profit of $0.09 per share was significantly above analysts’ consensus estimates.

Is now the time to buy Krispy Kreme? Find out by accessing our full research report, it’s free.

“We are pleased to have ended 2025 with positive momentum, driven by quality growth in the U.S. with key strategic partners, higher digital sales, and international expansion. In 2026, we look forward to building on this momentum through systemwide sales growth, additional refranchising activity, disciplined capital expenditures, lower net leverage, and positive free cash flow generation,” said Krispy Kreme CEO Josh Charlesworth.

Famous for its Original Glazed doughnuts and parent company of Insomnia Cookies, Krispy Kreme (NASDAQ:DNUT) is one of the most beloved and well-known fast-food chains in the world.

A company’s long-term sales performance is one signal of its overall quality. Any business can have short-term success, but a top-tier one grows for years.

With $1.52 billion in revenue over the past 12 months, Krispy Kreme is a mid-sized restaurant chain, which sometimes brings disadvantages compared to larger competitors benefiting from better brand awareness and economies of scale. On the bright side, it can still flex high growth rates because it’s working from a smaller revenue base.

As you can see below, Krispy Kreme’s sales grew at a decent 8% compounded annual growth rate over the last six years as it opened new restaurants and expanded its reach.

This quarter, Krispy Kreme’s revenue fell by 2.9% year on year to $392.4 million but beat Wall Street’s estimates by 0.9%.

Looking ahead, sell-side analysts expect revenue to decline by 1.5% over the next 12 months, a deceleration versus the last six years. This projection is underwhelming and implies its menu offerings will face some demand challenges.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

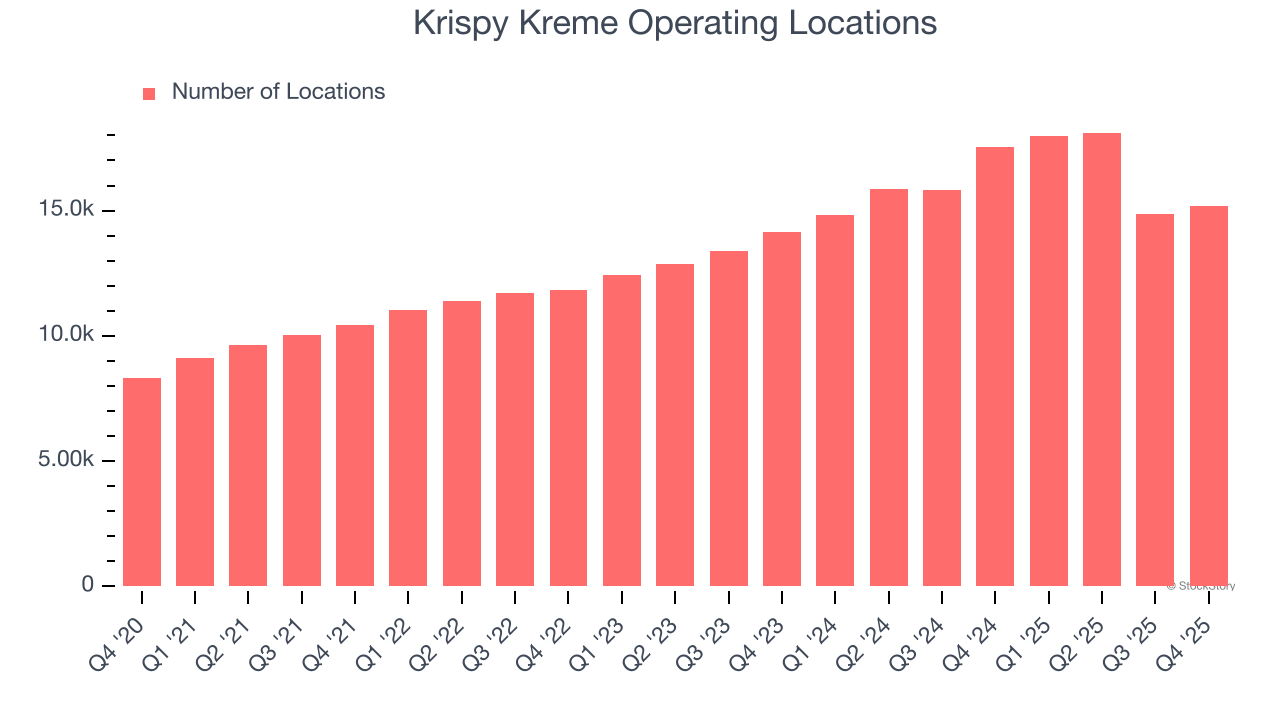

A restaurant chain’s total number of dining locations influences how much it can sell and how quickly revenue can grow.

Krispy Kreme sported 15,194 locations in the latest quarter. Over the last two years, it has opened new restaurants at a rapid clip by averaging 12.6% annual growth, among the fastest in the restaurant sector. This gives it a chance to become a large, scaled business over time.

When a chain opens new restaurants, it usually means it’s investing for growth because there’s healthy demand for its meals and there are markets where its concepts have few or no locations.

It was good to see Krispy Kreme beat analysts’ EPS expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this quarter featured some important positives. The stock traded up 12% to $3.35 immediately after reporting.

Krispy Kreme put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).

| Jul-22 | |

| Jul-20 | |

| Jul-09 | |

| Jul-09 | |

| Jul-06 | |

| Jul-06 | |

| Jun-24 | |

| Jun-22 | |

| Jun-21 | |

| Jun-09 | |

| Jun-05 |

These major companies may owe you money. How to apply in Arizona

DNUT +7.34%

AZCentral | The Arizona Republic

|

| Jun-05 |

These settlement claims may owe you money. How to apply in Arizona

DNUT +7.34%

AZCentral | The Arizona Republic

|

| Jun-04 | |

| Jun-01 | |

| May-26 |

Krispy Kreme's $1.6 million data breach settlement deadline nears. Who qualifies?

DNUT

Yahoo Personal Finance

|

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite