|

|

|

|

|||||

|

|

|

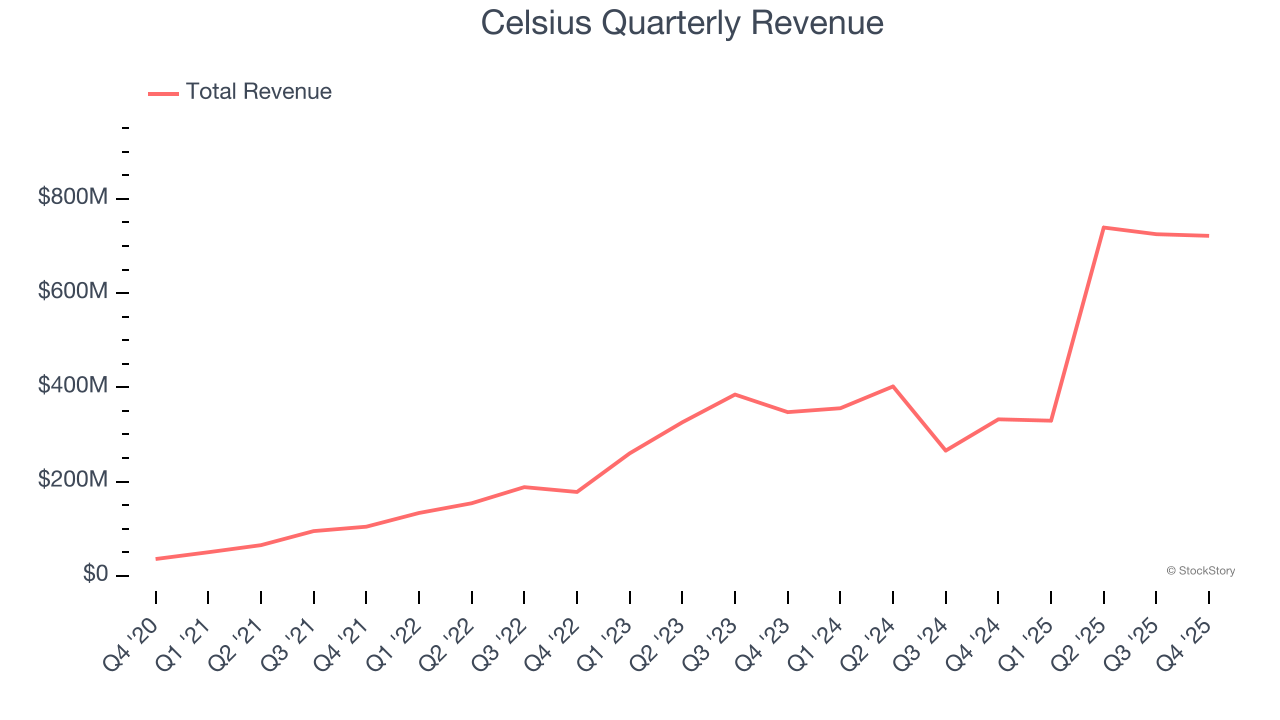

Energy drink company Celsius (NASDAQ:CELH) reported Q4 CY2025 results exceeding the market’s revenue expectations, with sales up 117% year on year to $721.6 million. Its non-GAAP profit of $0.26 per share was 36.9% above analysts’ consensus estimates.

Is now the time to buy Celsius? Find out by accessing our full research report, it’s free.

With its proprietary MetaPlus formula as the basis for key products, Celsius (NASDAQ:CELH) offers energy drinks that feature natural ingredients to help in fitness and weight management.

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

With $2.52 billion in revenue over the past 12 months, Celsius carries some recognizable products but is a mid-sized consumer staples company. Its size could bring disadvantages compared to larger competitors benefiting from better brand awareness and economies of scale. On the bright side, it can still flex high growth rates because it’s working from a smaller revenue base.

As you can see below, Celsius’s sales grew at an incredible 56.7% compounded annual growth rate over the last three years. This is an encouraging starting point for our analysis because it shows Celsius’s demand was higher than many consumer staples companies.

This quarter, Celsius reported magnificent year-on-year revenue growth of 117%, and its $721.6 million of revenue beat Wall Street’s estimates by 13.5%.

Looking ahead, sell-side analysts expect revenue to grow 28.5% over the next 12 months, a deceleration versus the last three years. Despite the slowdown, this projection is noteworthy and indicates the market is forecasting success for its products.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

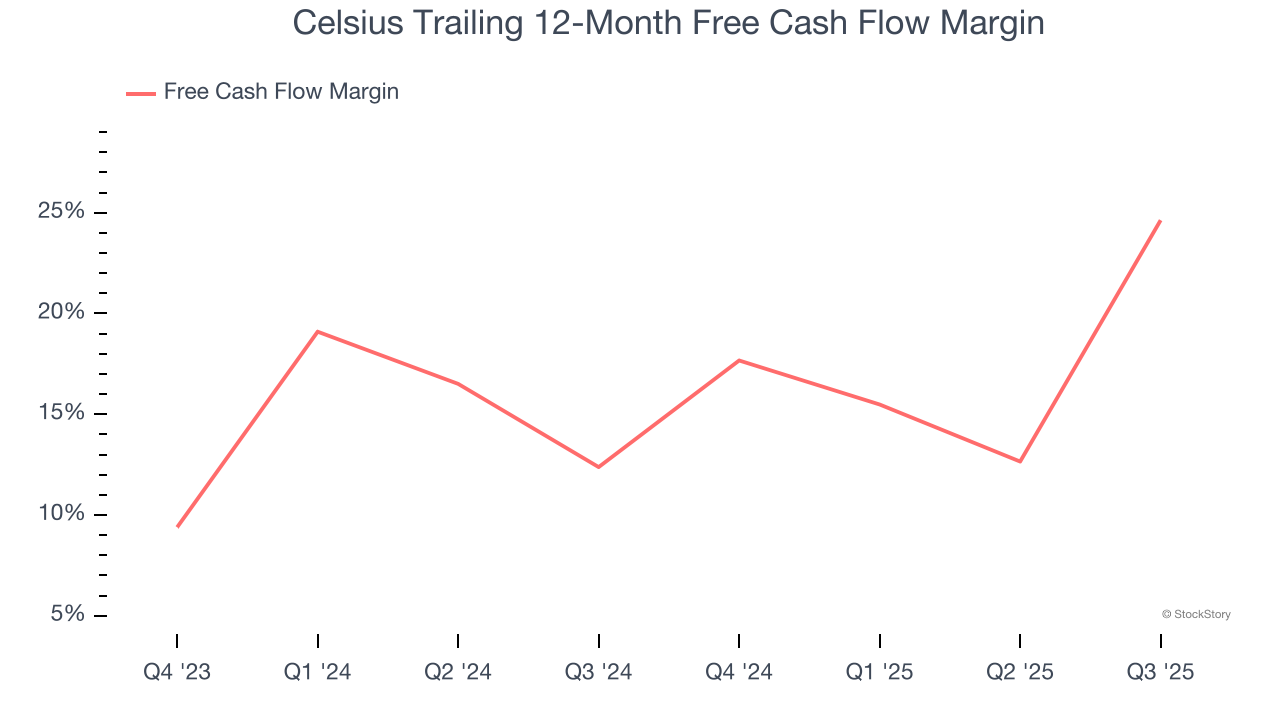

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Celsius has shown terrific cash profitability, driven by its lucrative business model that enables it to reinvest, return capital to investors, and stay ahead of the competition. The company’s free cash flow margin was among the best in the consumer staples sector, averaging 22% over the last two years.

We were impressed by how significantly Celsius blew past analysts’ EBITDA expectations this quarter. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. On the other hand, its gross margin missed. Zooming out, we think this quarter featured some important positives. The stock traded up 17% to $59.21 immediately following the results.

Celsius may have had a good quarter, but does that mean you should invest right now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).

| 56 min | |

| 2 hours | |

| Aug-10 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite