|

|

|

|

|||||

|

|

|

Albemarle Corporation ALB and Sociedad Quimica y Minera de Chile S.A. SQM are prominent players in the lithium space. A rebound in lithium prices amid rising demand and supply tightness has contributed to an upswing in their share prices. Both are well-placed to benefit from higher lithium prices driven by strong demand from electric vehicles (EVs) and energy storage systems, along with supply disruptions partly due to supply reductions in China. Lithium prices have rebounded lately from the trough levels seen last year, supported by tightening supply and strong demand in China and globally.

Let’s dive deep and closely compare the fundamentals of these two major lithium stocks to determine the better investment option now amid improving lithium market conditions.

Albemarle is well-placed to gain from long-term growth in the battery-grade lithium market. The market for lithium batteries and energy storage remains strong, especially for EVs, offering significant opportunities for the company to develop innovative products and expand capacity. Lithium demand is expected to grow on the back of significant global EV penetration. ALB expects lithium demand to witness a compound annual growth rate (CAGR) of 10-20% from 2025 to 2030 and sees stationary storage as a significant driver for lithium demand along with EVs. Lithium demand increased more than 30% year over year, and the company expects demand to grow roughly 15-40% this year.

The company is strategically executing its projects aimed at boosting its global lithium conversion capacity. It remains focused on investing in high-return projects to drive productivity. Healthy customer demand, capacity expansion and plant productivity improvements are supporting its volumes. ALB saw higher sales volumes in its Energy Storage unit in the fourth quarter of 2025 on strong production from its integrated conversion facilities. The Salar yield improvement project in Chile has achieved a 50% operating rate and ramp-up continues to deliver encouraging outcomes. The ramp-up at the Meishan lithium conversion facility in China is also progressing ahead of schedule.

Albemarle is also taking aggressive cost-saving and productivity actions. The company delivered roughly $450 million in cost and productivity improvements for full-year 2025, having surpassed its initial target of $300-$400 million. It expects additional cost and productivity improvements of $100-$150 million in 2026. ALB is taking actions to maintain its competitive position, including the initiation of a comprehensive review of cost and operating structure, optimization of the conversion network and reduction of capital expenditure. Its capital expenditures of $590 million for 2025 decreased 65% year over year.

ALB recently announced that it will idle Train 1, the remaining operating train at its Kemerton lithium hydroxide processing plant in Western Australia, and place it into care and maintenance effective immediately. This move follows earlier actions in 2024 to idle Train 2 for care and maintenance and stop expansion plans for Trains 3 and 4. The Kemerton facility processes spodumene from the Greenbushes mine, one of the world’s best deposits. The move is a result of ongoing efforts over the past two and a half years to reduce operating costs. The company expects higher flexibility and optionality to benefit adjusted EBITDA starting in the second quarter of 2026.

Albemarle remains committed to driving shareholder value by leveraging healthy cash flows and strong liquidity. At the end of 2025, ALB had liquidity of around $3.2 billion, including cash and cash equivalents of around $1.6 billion. Its operating cash flow was around $1.3 billion in 2025, up roughly 86% from the prior-year period. ALB expects generated free cash flow of $692 million for full-year 2025, driven by strong cash conversion, lower capital spending and productivity measures.

The company remains focused on maintaining its dividend payout. It has raised its quarterly dividend for the 30th straight year. ALB offers a dividend yield of 0.9% at the current stock price. Backed by healthy cash flows and sound financial health, the company's dividend is perceived to be safe and reliable.

Chile-based Sociedad Quimica produces plant nutrients, iodine, lithium and industrial chemicals. It is benefiting from being the low-cost producer of potassium chloride, potassium sulfate and potassium nitrate. SQM is gaining from the favorable trends in the lithium market underpinned by strong EV sales. Higher demand is also expected to continue to support the company’s lithium sales volumes.

Strong demand from EVs and energy storage systems, along with supply disruptions, is driving an improvement in lithium prices. Iodine volumes are being boosted by growing demand following the post-pandemic recovery. SQM is expected to benefit from its investment in expanding production capacity. Its Specialty Plant Nutrition business is also seeing higher demand across key end markets.

SQM logged record lithium sales volumes in the third quarter of 2025 on stronger-than-expected demand growth, driven by EVs and battery energy storage systems. The company achieved strong operating efficiency at its Atacama operations and made progress with the ramp-up of Australian operations. It saw a significant increase in spodumene sales produced in Australia and started production of lithium hydroxide in the country. Lower inventory in the supply chain, along with supply disruptions, contributed to an uptick in lithium prices. SQM expects lithium carbonate prices to increase sequentially in the fourth quarter.

Sociedad Quimica projects total capital expenditure of $2.7 billion for the 2025–2027 period, which includes the expansion of lithium carbonate and lithium hydroxide capacity in Chile, the expansion of the Mt. Holland project and investments to develop the Andover project, both in Australia.

SQM and Codelco recently completed their strategic partnership to jointly develop the Atacama salt flat. The partnership was completed through the merger by absorption of Codelco’s subsidiary, Minera Tarar SpA, into SQM’s subsidiary, SQM Salar SpA, which took full effect last month after a favorable Supreme Court resolution.

This major milestone paves the way for the production of refined lithium in the Salar de Atacama until 2060 and contributes to making Chile a leader in the production of lithium. Improvements in process efficiency, the adoption of new technologies and the optimization of operations are expected to lead to incremental lithium production through 2060.

Sociedad Quimica has a robust balance sheet and generates strong cash flows, which allow it to make investments in driving production capacity. The company ended the third quarter with cash and cash equivalents of roughly $1.5 billion. SQM generated an operating cash flow of roughly $756 million in the first nine months of 2025. It offers a dividend yield of 0.2% at the current stock price.

The ALB stock has surged 155.1% over the past year, while SQM has rallied 100.6% compared with the Zacks Chemicals Diversified industry’s decline of 12%.

ALB is currently trading at a forward price-to-sales ratio of 4.23. This represents a roughly 288% premium when stacked up with the industry average of 1.09X.

SQM is currently trading at a forward price-to-sales ratio of 3.21, below ALB and above the industry.

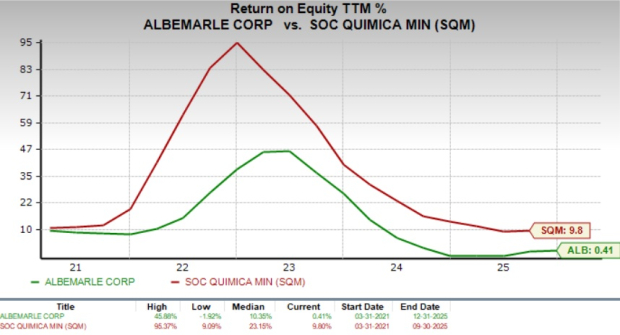

SQM’s return on equity of 9.8% is higher than ALB’s 0.4%. This reflects Sociedad Quimica’s efficient use of shareholder funds in generating profits.

The Zacks Consensus Estimate for ALB’s 2026 sales implies a year-over-year growth of 7.9%. The same for EPS suggests a 984.8% year-over-year rise. The EPS estimates for 2026 have been trending higher over the past 60 days.

The consensus estimate for SQM’s 2026 sales and EPS implies a year-over-year rise of 53.1% and 180.1%, respectively. The EPS estimates for 2026 have been trending northward over the past 60 days.

Both ALB and SQM currently sport a Zacks Rank #1 (Strong Buy), so picking one stock is not easy. You can see the complete list of today’s Zacks #1 Rank stocks here.

ALB and SQM stand to benefit from rebounding lithium prices driven by EV and energy storage demand. Albemarle is benefiting from higher lithium volumes on project ramp-ups and actions to boost global lithium conversion capacity and productivity. SQM is delivering record lithium volumes, expanding Atacama operations and is expected to benefit from the strategic partnership with Codelco. SQM appears to have an edge over ALB due to its more attractive valuation. In addition, SQM’s higher ROE indicates that it is more effectively utilizing shareholder funds. Investors seeking exposure to the lithium space might consider Sociedad Quimica as the more favorable option at this time.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Jul-30 | |

| Jul-28 | |

| Jul-28 | |

| Jul-23 | |

| Jul-21 | |

| Jul-16 | |

| Jul-16 | |

| Jul-07 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite