|

|

|

|

|||||

|

|

|

The rapid rise of artificial intelligence (AI) has transformed the cloud computing landscape, making AI enabled infrastructure a central focus for investors. Nebius Group N.V. NBIS and Alphabet Inc. GOOGL represent two distinct approaches to this evolving market. Nebius is a specialized AI cloud provider, offering high-performance GPU clusters and bespoke infrastructure for large-scale AI workloads, backed by multi-billion-dollar deals with major tech players, while Alphabet, through Google Cloud, leverages its vast, diversified ecosystem to deliver AI-enhanced services alongside search, YouTube and other revenue streams.

Per the Grand View Research Report, the global cloud AI market was valued at approximately $121.74 billion in 2025 and is expected to expand to $1,728.40 billion by 2033, representing a robust CAGR of 39.3% between 2026 and 2033. This uptrend in the cloud AI market benefits both Alphabet and Nebius, but not equally.

For investors aiming to make a strategic play in the AI infrastructure sector, which stock emerges as the most compelling choice?

Let’s evaluate their fundamentals, growth prospects, market challenges and valuations to determine which one presents a stronger investment opportunity.

Nebius continues to experience robust demand across large accounts, hyperscalers, AI start-ups and enterprise clients. AI-native companies are rapidly scaling, with GPU usage increasing from hundreds and thousands to tens of thousands. Enterprise clients are also expanding AI adoption across critical business processes, resulting in larger and longer-duration contracts. The company’s sales pipeline remains strong, with new contract durations increasing 50%. The company continues to see strong pipeline growth, with first-quarter 2026 pipeline creation projected to exceed $4 billion.

In fourth-quarter 2025, Nebius’ core AI cloud business delivered exceptional results, with revenue surging 830% year over year and 63% sequentially, supported by high utilization levels, favorable pricing and disciplined execution. Adjusted EBITDA turned positive in the fourth quarter, with margins expanding to 24% from 19% in the prior quarter.

Nebius’ growth is further supported by the expansion of its AI cloud platform through organic development and strategic acquisitions. The launch of Token Factory and Aether, along with the acquisition of Tavily, has enhanced platform capabilities and developer engagement. Software attach rates for AI cloud customers are 100%, and the company has multiple financing options, including operating cash flow, debt financing, asset-backed financing, potential equity issuance and stakes in non-core assets.

Nebius is aggressively expanding its infrastructure, having secured more than 2 gigawatts of contracted power with plans to surpass 3 gigawatts, and remains on track to deliver 800 megawatts to 1 gigawatt of data center capacity by the end of 2026. For 2026, the company expects revenue of $3 billion to $3.4 billion, with an annualized run-rate revenue target of $7 billion to $9 billion by year-end.

However, Nebius operates in a highly dynamic and capital-intensive environment. The company plans to invest between $16 billion and $20 billion in capex in 2026. Such elevated capex levels increase risk if revenue growth does not keep pace with the company’s capital-intensive strategy, especially as AI demand could fluctuate amid competitive pricing pressures and evolving regulatory conditions. Moreover, scaling aggressively (multiple data centers in various regions) involves execution risk. Stiff competition is an added concern.

Google Cloud is rapidly emerging as a leading platform for AI-powered enterprise solutions. Revenues grew 35.8% year over year to $58.71 billion in 2025, supported by investments in infrastructure, data management, security and AI services. Strategic partnerships, notably with NVIDIA, allow Google Cloud to offer cutting-edge GPUs such as the B200, GB200 Blackwell and next-generation Vera Rubin GPUs, enabling customers to run large AI workloads efficiently. Enterprise adoption is further accelerated through tools like the Agent Development Kit and Agent Designer, which simplify the deployment of AI agents.

The company is capitalizing on demand for large language models with Gemini, Gemini Flash, Imagen 3 and Veo 2, while the recent launch of Gemma 3 enables lightweight, high-performance AI models to run on a single GPU or TPU. Infrastructure enhancements, including the seventh-generation Ironwood TPU, Cloud WAN and quantum chip Willow, strengthen its AI cloud capabilities. Combined with strong developer adoption and continued AI innovation, these initiatives position Alphabet to maintain leadership in AI cloud services, drive enterprise adoption and sustain robust revenue growth.

Alphabet has a diversified business model spanning search, YouTube, cloud and AI-driven services, reducing reliance on any single revenue stream. The company continues to strengthen its position in AI-driven search and advertising, leveraging advanced AI models and features to enhance user engagement. Initiatives such as the launch of Gemini 3, Gemini 2.5 and AI Overview are transforming the search experience, offering faster, multimodal and context-aware responses.

Features like Circle to Search and AI Mode, available in 40 languages and used by more than 75 million daily active users, are expanding Alphabet’s reach among younger users and driving increased search engagement, which in turn supports advertising revenue growth. In 2025, Google’s advertising revenues rose 11.4% year over year to $294.69 billion, fueled by gains in Search and YouTube ads, highlighting the direct impact of AI integration on monetization.

The company is also deepening its focus on generative AI, and next-generation AI infrastructure underpins its long-term growth guidance. In fourth-quarter 2025, revenues from products built on Alphabet’s generative AI models (Gemini, Imagen, Veo, Chirp and Lyria) grew more than 400% year over year, reflecting accelerating adoption. Nearly 350 Google Cloud customers each processed more than 100 billion tokens in December alone, highlighting the increasing adoption and usage of Alphabet’s AI models for various applications.

Despite its strong AI and cloud growth, Alphabet faces several challenges that could pressure revenues and margins. Advertising, which accounted for 73.2% of total revenue in 2025, remains exposed to fluctuations in advertiser spending, with Network ad revenues declining 2% year over year. Regulatory scrutiny and global litigations, including antitrust fines in Europe, Android distribution investigations and search data-sharing mandates, pose ongoing legal and compliance risks. Rising investments in AI initiatives, R&D and global infrastructure are escalating costs, with R&D up 23.8% in 2025. For 2026, the company projects capital expenditures within $175–$185 billion.

NBIS shares have surged 49.2%, while GOOGL stock has soared 51.2% over the past six months.

Valuation-wise, Alphabet seems undervalued while Nebius seems overvalued, as suggested by the Value Score of B and the Value Score of F, respectively.

In terms of Price/Sales, NBIS shares are trading at 50.26X, higher than GOOGL’s 9.5.

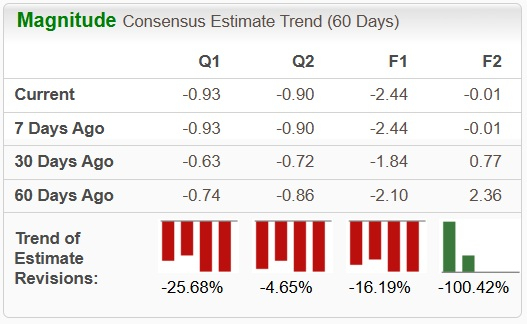

Analysts have significantly revised their earnings estimates downward for NBIS’ bottom line for the current year.

For GOOGL, there is a significant upward revision.

Both NBIS and GOOGL carry a Zacks Rank #3 (Hold) at present.You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

NBIS has rapid AI cloud growth but faces several aforementioned headwinds, while GOOGL combines scale, diversified revenue and advanced AI, making it the stronger, more sustainable investment at the moment.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 9 min | |

| 28 min | |

| 28 min | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite