|

|

|

|

|||||

|

|

|

Amid a favorable demand environment for digital learning solutions, AI-based alternatives and career-focused learning, the United States education market is witnessing growth from the recently announced initiative by the U.S. Department of Education. Education providers like Stride, Inc. LRN and Chegg, Inc. CHGG are also riding the same wave.

The formation of the Accreditation, Innovation and Modernization (AIM) program primarily aims to reform the higher education accreditation system. The expansion of the accreditation reforms is expected to boost recognition for innovative education models and career-focused learning, thus directly or indirectly supporting the prospects of the companies mentioned above.

Stride’s operations primarily focus on the United States market, offering K-12 virtual schooling and career-learning programs. Conversely, Chegg mainly focuses on homework help, textbook services and tutoring services through innovative digital models.

Let’s dive deep and closely compare the fundamentals of the two edtech stocks to determine which one is a better investment now.

The sustained secular shift toward virtual and alternative education models is fueling Stride’s prospects in the education market. Parents' dissatisfaction with traditional K-12 education remains high, thus supporting the company’s core value proposition and underpinning management’s confidence in long-term growth.

LRN’s success in aligning its service offerings with the workforce-oriented education trends is substantiated by the recent numbers. During the first six months of fiscal 2026, the Career Learning segment’s enrollments grew year over year by 18.1% to 111,100 students, with revenues growing 20.5% to $547.6 million. Besides, after being threatened by the technical glitches at the beginning of its fiscal 2026, as of now, the volatility has subsided with withdrawal rates being stabilized. This justifies Stride’s consistent focus on its retention initiatives and academic quality investments, which are beginning to show results.

Notably, the company’s operating leverage and disciplined cost management are taking the limelight. During the first six months of fiscal 2026, its adjusted operating income and adjusted EBITDA grew year over year by 23.8% and 21.3%, respectively. Despite temporary headwinds from platform implementation challenges, Stride reaffirmed its full-year revenue guidance and raised its adjusted operating income outlook, signaling confidence in execution for the remainder of fiscal 2026. For fiscal 2026, LRN now expects adjusted operating income to be in the range of $485-$505 million, up from the previously expected range of $475-$500 million.

However, Stride is susceptible to various risks, with the recent technical failure exposing it to execution risk and dependence on third-party vendors. While issues have improved, further disruptions could hurt enrollment retention and reputation. Also, LRN’s margins are expected to face pressure from continued platform investments and implementation costs.

Currently, Chegg seems to be repositioning itself around the $40 billion global workforce skilling market. After years of traffic pressure in its legacy academic business, management has split operations into two focused units, including Chegg Skilling as the growth engine and Academic Services as a cash-flow generator. Early signals regarding this strategic pivot are convincing, with Chegg Skilling revenues increasing 11% year over year in the fourth quarter of 2025 to $17.7 million. Notably, CHGG has integrated AI-powered learner support, predictive nudges, speech recognition tools and conversational AI features across its skilling and language-learning platforms (including Busuu). These capabilities enhance engagement, retention and completion rates, a key differentiator in the competitive edtech landscape.

Another positive factor is the expansion into B2B and enterprise distribution channels. Partnerships with organizations such as DHL, Gi Group, and Woolf University strengthen institutional credibility and broaden distribution. The Woolf partnership is particularly strategic, as it enables skills programs to connect with accredited degree pathways, aligning Chegg’s offerings with credential-based outcomes, an increasingly important factor in workforce mobility.

However, despite all the tailwinds supporting its growth, Chegg’s most significant challenge remains pressure from the legacy Academic Services business. It is experiencing declining revenue and subscriber trends, due to generative AI competition and changing student behavior. Management explicitly acknowledges the disruptive impact of AI on traditional homework-help models, which has weighed on traffic and engagement. Although Chegg Skilling is growing, it remains relatively small compared to the shrinking legacy segment. The turnaround depends heavily on successful execution and sustained double-digit growth in a highly competitive environment.

Moreover, the ongoing restructuring moves are weighing heavily on the cash flow, which was negative $12.6 million as of 2025-end against $50.3 million at 2024-end. The drag was caused by severance expenses tied to multiple restructuring initiatives, with additional cash outflows expected in early 2026. Although these actions aim to improve long-term efficiency, they reflect ongoing operational strain.

As witnessed from the chart below, during the past three months, Stride’s share price performance has outperformed Chegg’s, with the latter indicating a declining trend.

Considering valuation, over the last five years, Stride has been trading above Chegg on a forward 12-month price-to-sales (P/S) ratio basis.

Overall, from these technical indicators, it can be deduced that LRN stock offers an increasing trend with a relatively premium valuation, while CHGG stock offers a declining trend at a comparatively lower valuation.

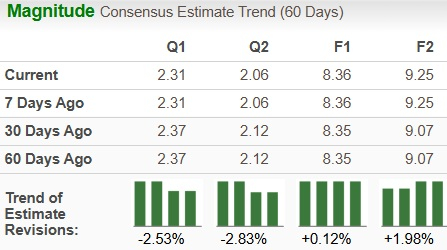

LRN’s earnings estimates for fiscal 2026 and fiscal 2027 have moved north in the past 30 days. The revised figures for fiscal 2026 and 2027 imply year-over-year improvements of 3.2% and 10.7%, respectively.

LRN's EPS Trend

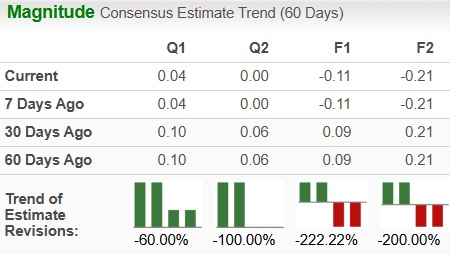

CHGG’s earnings estimate for 2026 and 2027 has contracted to a loss per share of 11 cents and 21 cents, respectively, over the past 30 days. The estimated figures for 2026 and 2027 indicate 466.7% and 90.9% year-over-year decline.

CHGG's EPS Trend

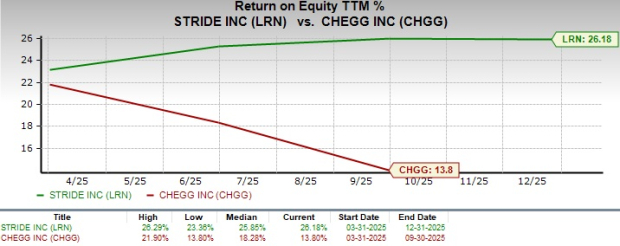

Stride’s trailing 12-month ROE of 26.2% significantly exceeds Chegg’s average, underscoring its efficiency in generating shareholder returns.

The digital education landscape remains supported by growing demand for AI-enabled and career-focused learning solutions. However, a clear divergence is emerging between Stride, which currently has a Zacks Rank #3 (Hold) and Chegg, presently having a Zacks Rank #4 (Sell), in terms of earnings visibility and execution stability.

Stride continues to capitalize on the secular shift toward virtual K-12 and workforce-oriented education. Strong enrollment growth in its Career Learning segment, expanding operating leverage and disciplined cost management have driven solid profit gains. Increasing earnings estimates and healthy ROE reinforce its relatively stable growth profile despite platform-related execution risks and ongoing investment pressures.

On the other hand, Chegg is undergoing a strategic pivot toward workforce skilling while managing structural declines in its legacy Academic Services business. Although Chegg Skilling is showing early growth traction, it remains small relative to the shrinking core segment. Besides, a negative cash flow, elevated restructuring expenses and sharp downturn of earnings estimate revisions (with projected losses through 2027) weigh heavily on the outlook.

Thus, it can be deduced that LRN stock offers relatively better risk-adjusted upside and earnings stability compared with CHGG stock, whose path remains uncertain, supporting its Sell-rated stance. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-05 | |

| Aug-04 | |

| Aug-04 | |

| Jul-30 | |

| Jul-29 | |

| Jul-24 | |

| Jul-21 | |

| Jul-15 | |

| Jul-14 | |

| Jul-07 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite