|

|

|

|

|||||

|

|

|

As Target Corporation TGT is slated to report fourth-quarter fiscal 2025 earnings on March 3 before market open, investors face an important decision on whether they should buy the stock now or hold their current positions.

TGT has built a strong position in retail through its diversified business model and omnichannel strategy. With market conditions in mind, it is crucial to evaluate key factors influencing Target’s performance and whether the stock offers an attractive entry point ahead of its earnings report.

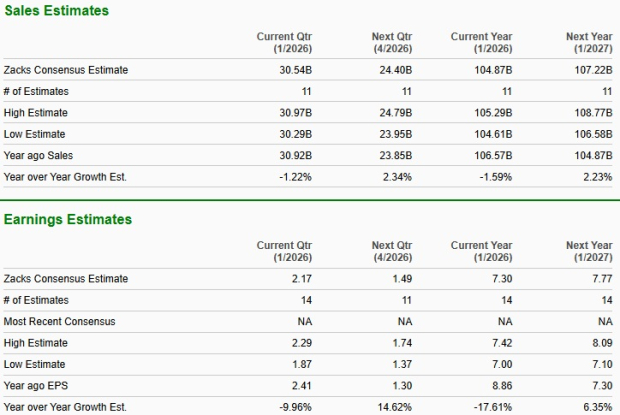

The Zacks Consensus Estimate for fiscal fourth-quarter revenues is pegged at $30.54 billion, indicating a 1.2% decline from the year-ago reported level. Although the consensus mark for quarterly earnings has moved up by a penny in the past 30 days to $2.17 per share, it still indicates a 10% decline from the year-ago quarter’s reported figure.

Target has a trailing four-quarter average negative earnings surprise of 3.4%. However, in the last reported quarter, the company’s bottom line beat the Zacks Consensus Estimate by 1.1%.

As investors prepare for TGT’s fourth-quarter fiscal 2025 announcement, the question of earnings beat or miss looms. Our proven model does not conclusively predict an earnings beat for Target this time. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. However, that is not the case here. You can see the complete list of today’s Zacks #1 Rank stocks here.

Target has a Zacks Rank #2 but an Earnings ESP of -2.24%. You can uncover the best stocks to buy or sell before they are reported with our Earnings ESP Filter.

Target Corporation price-consensus-eps-surprise-chart | Target Corporation Quote

Target’s integrated strategy appears to have supported its fiscal fourth-quarter performance despite a challenging retail backdrop. The company’s strong brand equity and differentiated owned-brand portfolio continue to set it apart in a crowded marketplace. Its focus on merchandising authority, built around trend-right and design-led assortments, likely helped maintain relevance with core guests during the critical holiday period.

Initiatives such as the evolution of Hardlines into Fun 101, renewed emphasis on Home and Baby, and an acceleration of product introductions for the holiday season are likely to have driven traffic during the key shopping season.

At the same time, Target’s omnichannel ecosystem has been a stabilizing force. Growth in same-day services, including Drive Up and Target Circle 360 delivery, along with the expansion of marketplace capabilities through Target Plus and retail media momentum via Roundel, is likely to have played a constructive role in TGT’s performance.

Ongoing investments in AI-driven merchandising tools, improved inventory forecasting and fulfillment optimization were aimed at enhancing in-stock levels, personalization and speed to market. Better inventory discipline and improved shrink trends may have also supported operational efficiency and helped protect profitability during a competitive holiday season.

However, the fiscal fourth-quarter performance is likely to have been constrained by persistent headwinds such as tariffs. Also, consumers have been cautious, particularly in discretionary categories, prioritizing essential purchases over non-essentials. Softer store traffic and lighter basket sizes, combined with heightened promotional activity across the retail landscape, are likely to have weighed on the overall sales productivity.

Elevated markdown activity and competitive pricing pressures are anticipated to have weighed on margin, making it difficult for the company’s strategic initiatives to fully offset softness in demand.

We expect the number of transactions to decline 2.2% and the average transaction value to decrease 0.6% in the fiscal fourth quarter. As a result, we anticipate comparable sales to decline 2.8%.

From a valuation standpoint, Target’s stock is currently trading at a discount compared with the Zacks Retail - Discount Stores industry. With a forward 12-month price-to-earnings (P/E) ratio of 14.92, Target stands far below the industry average of 33.48, suggesting that the stock may be relatively cheap at the current levels.

When compared with other retail giants, including Costco Wholesale Corporation COST, Walmart Inc. WMT and Ross Stores, Inc. ROST, the company’s valuation looks even more discounted. Costco trades at a forward P/E of 47.15, Walmart at 43.09 and Ross Stores at 28.09 — all higher than Target’s valuation multiple.

Over the past three months, Target’s stock has gained 31% compared with the industry’s growth of 11.6%. Meanwhile, the Retail-Wholesale sector and the S&P 500 have increased 0.5% and 1.2%, respectively.

The company outperformed its key peers, including Walmart, which has gained 15.5%. Ross Stores’ stock has rallied 13.7%, while Costco’s stock has returned 9.7% over the same period.

TGT heads into its fiscal fourth-quarter earnings release with solid strategic strengths but lingering pressures that could limit upside surprises. Its differentiated merchandise offerings, expanding omnichannel capabilities and operational improvements position the company well for long-term growth, yet cautious consumer spending, promotional intensity and margin headwinds may keep results mixed.

Given its discounted valuation and improving momentum relative to peers, the stock appears attractively positioned for investors with a longer-term horizon. Current shareholders should consider holding their positions to benefit from potential long-term recovery and strategic execution.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite