|

|

|

|

|||||

|

|

|

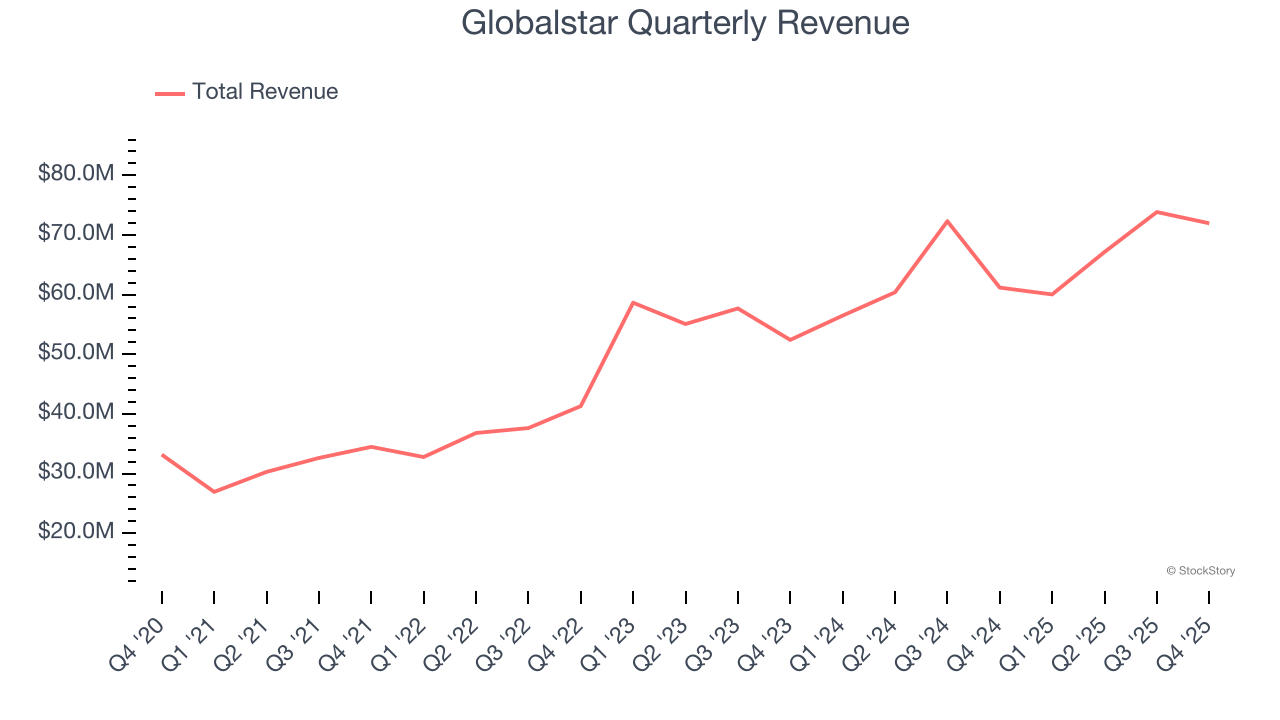

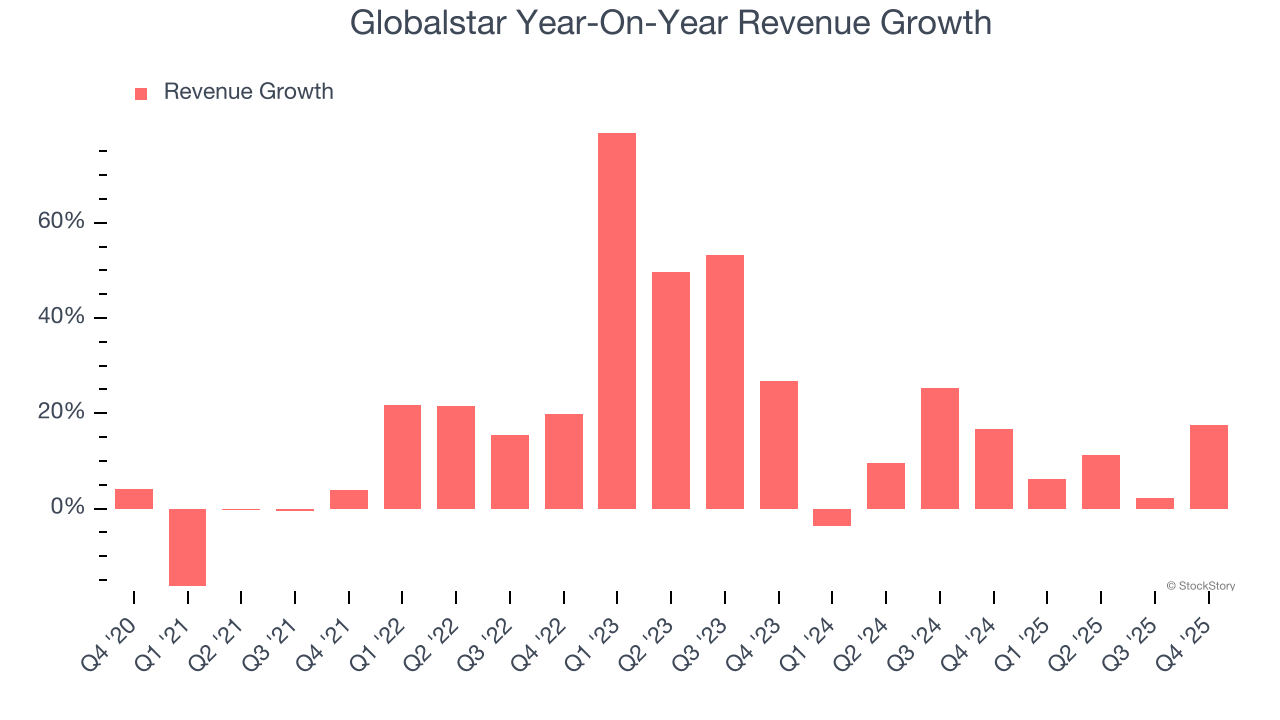

Satellite communications provider Globalstar (NASDAQ:GSAT) reported Q4 CY2025 results topping the market’s revenue expectations, with sales up 17.6% year on year to $71.96 million. On the other hand, the company’s full-year revenue guidance of $292.5 million at the midpoint came in 3.9% below analysts’ estimates. Its GAAP loss of $0.11 per share was significantly below analysts’ consensus estimates.

Is now the time to buy Globalstar? Find out by accessing our full research report, it’s free.

Known for powering the emergency SOS feature in newer Apple iPhones, Globalstar (NASDAQ:GSAT) operates a network of low-earth orbit satellites that provide voice and data communications services in remote areas where traditional cellular networks don't reach.

A company’s long-term performance is an indicator of its overall quality. Any business can have short-term success, but a top-tier one grows for years.

With $273 million in revenue over the past 12 months, Globalstar is a small player in the business services space, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and numerous distribution channels. On the bright side, it can grow faster because it has more room to expand.

As you can see below, Globalstar grew its sales at an incredible 16.3% compounded annual growth rate over the last five years. This is a great starting point for our analysis because it shows Globalstar’s demand was higher than many business services companies.

We at StockStory place the most emphasis on long-term growth, but within business services, a half-decade historical view may miss recent innovations or disruptive industry trends. Globalstar’s annualized revenue growth of 10.4% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, Globalstar reported year-on-year revenue growth of 17.6%, and its $71.96 million of revenue exceeded Wall Street’s estimates by 1.9%.

Looking ahead, sell-side analysts expect revenue to grow 11.5% over the next 12 months, similar to its two-year rate. This projection is admirable and suggests its newer products and services will catalyze better top-line performance.

The 1999 book Gorilla Game predicted Microsoft and Apple would dominate tech before it happened. Its thesis? Identify the platform winners early. Today, enterprise software companies embedding generative AI are becoming the new gorillas. a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

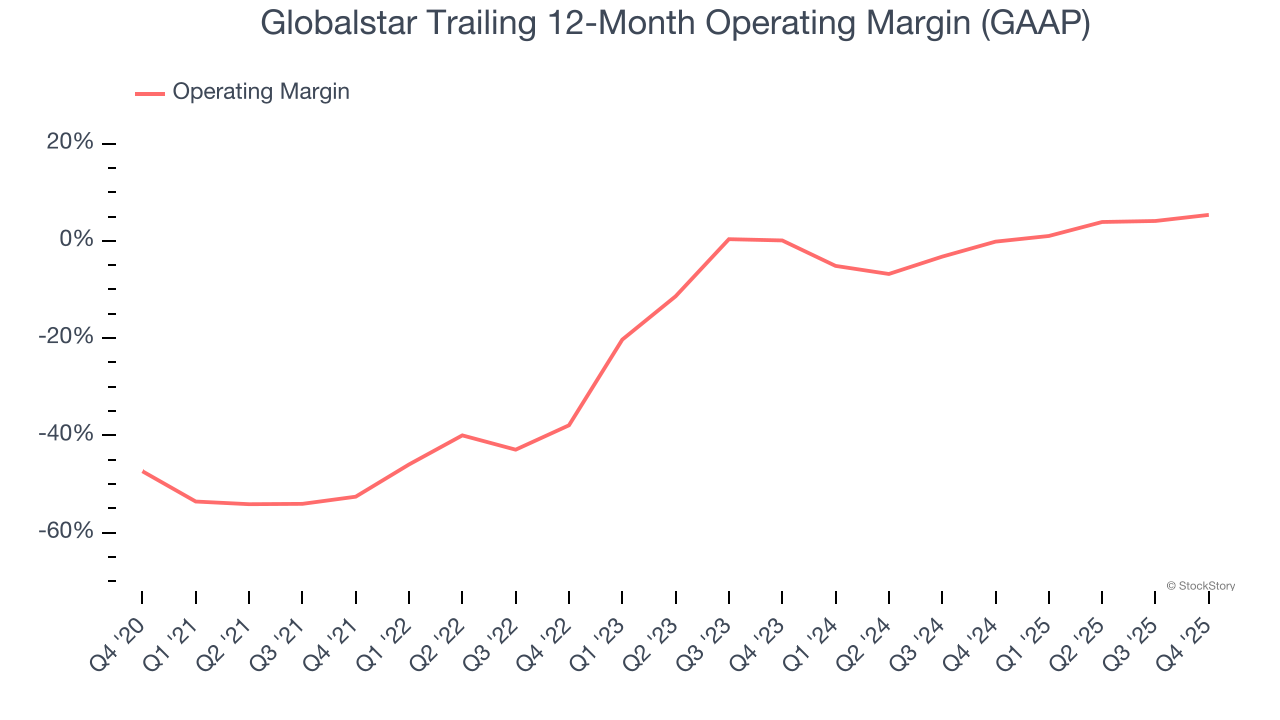

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after subtracting all core expenses, like marketing and R&D.

Although Globalstar broke even this quarter from an operational perspective, it’s generally struggled over a longer time period. Its expensive cost structure has contributed to an average operating margin of negative 10.5% over the last five years. Unprofitable business services companies require extra attention because they could get caught swimming naked when the tide goes out.

On the plus side, Globalstar’s operating margin rose by 57.9 percentage points over the last five years, as its sales growth gave it operating leverage. Still, it will take much more for the company to reach long-term profitability.

Globalstar’s operating margin was negative 0.5% this quarter.

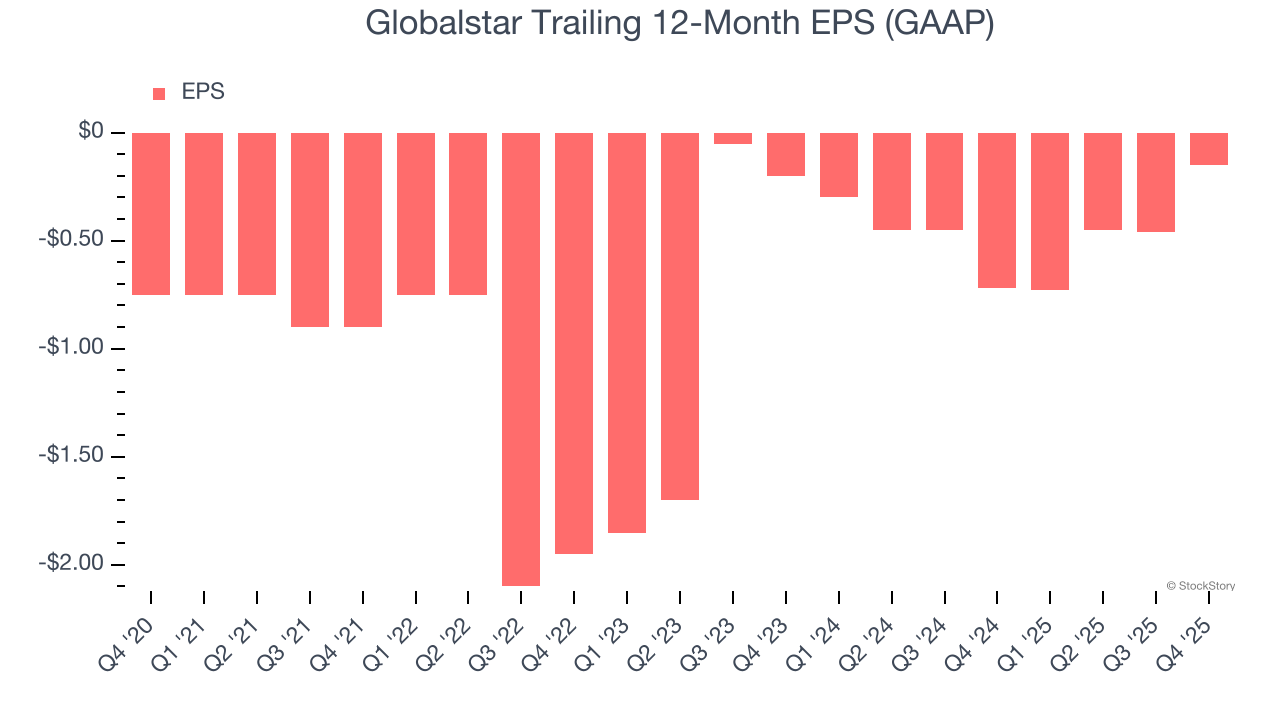

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Although Globalstar’s full-year earnings are still negative, it reduced its losses and improved its EPS by 27.5% annually over the last five years. The next few quarters will be critical for assessing its long-term profitability. We hope to see an inflection point soon.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Globalstar, its two-year annual EPS growth of 13.6% was lower than its five-year trend. We still think its growth was good and hope it can accelerate in the future.

In Q4, Globalstar reported EPS of negative $0.11, up from negative $0.42 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates. Over the next 12 months, Wall Street expects Globalstar to improve its earnings losses. Analysts forecast its full-year EPS of negative $0.15 will advance to negative $0.04.

It was encouraging to see Globalstar beat analysts’ revenue expectations this quarter. On the other hand, its full-year revenue guidance missed and its EPS fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 1.9% to $56.41 immediately following the results.

Globalstar’s latest earnings report disappointed. One quarter doesn’t define a company’s quality, so let’s explore whether the stock is a buy at the current price. When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).

| Aug-06 | |

| Aug-06 | |

| Aug-03 | |

| Jul-30 | |

| Jul-27 | |

| Jul-27 | |

| Jul-27 | |

| Jul-27 | |

| Jul-27 | |

| Jul-27 | |

| Jul-27 | |

| Jul-27 | |

| Jul-27 | |

| Jul-22 | |

| Jul-01 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite