|

|

|

|

|||||

|

|

|

Credo Technology Group Holding Ltd CRDO is scheduled to report third-quarter fiscal 2026 results on March 2, 2026, after the closing bell.

The Zacks Consensus Estimate for the bottom line for the to-be-reported quarter is pegged at 96 cents, indicating a 284% year-over-year surge. The estimate has moved up 18 cents in the past 30 days. The Zacks Consensus Estimate for total revenues is pinned at $389.4 million, implying a 188.5% increase.

CRDO recently reported preliminary results for the third quarter of fiscal 2026. The company now expects to report revenues between $404 million and $408 million, far exceeding its previously issued guidance of $335 million to $345 million.

Credo’s earnings beat the Zacks Consensus Estimate in each of the trailing four quarters, with an average surprise of 38.46%.

Our proven model predicts an earnings beat for CRDO this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the chances of an earnings beat. This is exactly the case here.

You can uncover the best stocks to buy or sell before they are reported with our Earnings ESP Filter.

CRDO has an Earnings ESP of +3.54% and a Zacks Rank #1. You can see the complete list of today’s Zacks #1 Rank stocks here.

Credo’s fiscal third-quarter performance is likely to have been driven by strong demand for its active electrical cables (“AEC”) and optical products, along with deeper engagement with hyperscalers. In the last reported quarter, four hyperscalers each contributed more than 10% of total revenues, reflecting strong adoption of Credo’s high-reliability AEC solutions. Management noted that the fourth hyperscaler is in full volume. Still, the more important development in the last reported quarter was the emergence of a fifth hyperscaler, which has begun contributing initial revenues. The company also highlighted that customer forecasts have strengthened across the board in recent months. This marks a major inflection point.

CRDO expects each of its top four customers to grow significantly year over year in the current fiscal year. This is likely to have benefited the performance of the fiscal third quarter. The growing hyperscaler base reduces the risk of customer concentration and enhances the stability of top-line growth.

AECs remain Credo’s fastest-growing product line and the primary revenue driver. On the last earnings call, management highlighted that AECs, now scaling to 100-gig per lane and transitioning to 200-gig per lane architectures, have become the “de facto” standard for inter-rack connectivity. These are now replacing optical rack-to-rack connections up to seven meters. The explosive adoption of zero-flap AECs is mainly due to these cables offering up to 1,000 times more reliability with 50% lower power consumption than optical solutions, underscored by CRDO.

Credo’s IC business, which includes retimers and optical DSPs, has also been witnessing increasing traction.

Management noted that the Bluebird optical DSP (demonstrated in the fiscal first quarter) is receiving strong interest and positive customer feedback. Ethernet retimers also remain a critical piece of AI server and switching fabrics, particularly where MACsec encryption, gearbox capabilities and software programmability matter. Credo’s PCIe retimer program remains on track for design wins in fiscal 2026 and revenue contributions in the next fiscal year.

Credo Technology Group Holding Ltd. price-consensus-eps-surprise-chart | Credo Technology Group Holding Ltd. Quote

With the recent launch of the Blue Heron 224G AI scale-up retimer, it is eyeing the lucrative scale-up networking market.

CRDO’s improving profitability is another thing investors need to watch for. In the last reported quarter, non-GAAP gross margin expanded 410 basis points (bps) to 67.7%, coming in above the high end of the company’s guidance. Non-GAAP operating income was $124.1 million compared with $8.3 million reported in the prior-year period.

For the fiscal third quarter, CRDO expects non-GAAP gross margin to be between 64% and 66% and operating expenses at $68-$72 million.

However, tougher competition and an uncertain macro backdrop due to looming tariff shifts continue to pose challenges. Credo competes with semiconductor bigshots like Broadcom Inc. AVGO and Marvell Technology, Inc. MRVL as well as newer entrants like Astera Labs ALAB.

Also, heavy reliance on a few customers creates concentration risks, leaving the company exposed to sharp revenue hits if any major client pulls back.

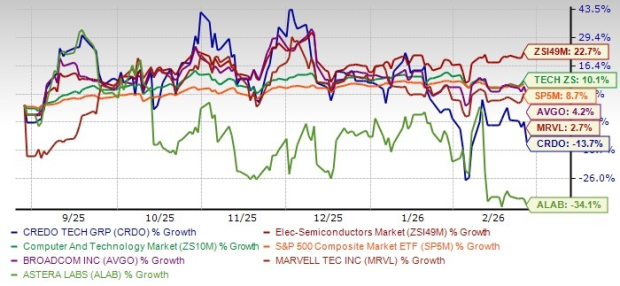

CRDO’s shares have tanked 13.7% in the past six months, significantly underperforming its Electronics - Semiconductors industry, Zacks Computer and Technology sector and S&P 500 composite’s growth of 22.7%, 10.1% and 8.7%, respectively.

AVGO and MRVL have gained 4.2% and 2.7%, respectively, while ALAB has lost 34.1% in the same time frame.

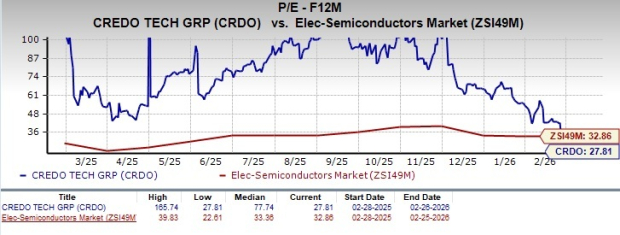

From a valuation standpoint, CRDO appears to be trading at a discount relative to the industry and is trading well above its mean. Going by the price/earnings ratio, the company’s shares currently trade at 27.81 forward earnings, lower than 32.86 for the industry and the stock’s mean of 77.74.

In comparison, Broadcom trades at a forward 12-month P/E multiple of 27.94, while Astera Labs and Marvell Technology are trading at a multiple of 49.28 and 22.19, respectively.

Credo’s preliminary fiscal third-quarter revenue update above its prior guidance reinforces strong hyperscaler-driven demand momentum. The company’s leadership in AECs and expanding IC portfolio position it at the center of AI cluster buildouts. Margin expansion and operating leverage remain compelling. Trading at a relative discount, CRDO offers an attractive risk-reward setup ahead of the upcoming results.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 28 min | |

| 2 hours | |

| 3 hours | |

| 8 hours | |

| Jul-19 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 |

Chip Stocks Enter Bear Market But Roar Back. Astera Labs Continues Slump.

ALAB -5.04%

Investor's Business Daily

|

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite