|

|

|

|

|||||

|

|

|

Everpure’s PSTG shares have gained around 9% following fourth-quarter fiscal 2026 results, fueled by strong revenue growth amid a robust AI demand environment. However, the momentum proved short-lived, as the stock declined roughly 10% in the subsequent trading session. Although the company delivered impressive growth, management remains wary of global supply-chain imbalances, AI infrastructure spending cycles, competition from hyperscaler-native storage offerings and pricing pressure in large enterprise deals. Overall, the company’s shares are down around 3% since the earnings release.

In the past year, shares rallied 25.7%, underperforming the Zacks Computer-Storage Devices industry’s growth of 187.2%. The stock has lagged the Zacks Computer & Technology sector growth of 29.1% while it outperformed the S&P 500’s gain of 20.3%, respectively.

The company has outperformed its competitor in the storage space, like NetApp, Inc. NTAP, while underperforming Seagate Technology Holdings plc STX and Sandisk Corporation SNDK. NTAP has gained 1.4% in the past year, while STX and SNDK have skyrocketed 309.6% and 1,291.4%, respectively.

With this mixed relative performance, investors may be questioning whether PSTG has upside or if expectations have outpaced fundamentals. Let’s break down to see what’s driving the rally, the bull and bear cases, and a practical approach to managing risk and position size.

PSTG reported fourth-quarter fiscal 2026 non-GAAP earnings per share (EPS) of 69 cents, which beat the Zacks Consensus Estimate of 65 cents. The company reported non-GAAP EPS of 45 cents in the prior-year quarter.

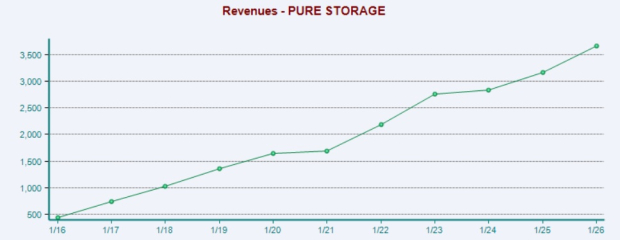

Quarterly revenues expanded 20% year over year to $1.1 billion, beating the Zacks Consensus Estimate by 2.5%. This marks the first billion-dollar quarter in the company’s history. For the full fiscal year, revenues totaled $3.7 billion, up 16% year over year. The growth reflects strong demand across enterprise customers, modernizing legacy storage, hyperscalers scaling AI workloads and hybrid and multi-cloud environments.

Everpure has strengthened its hyperscale positioning by partnering with SK hynix to deliver advanced QLC flash storage optimized for large data centers. The partnership positions Everpure well for large-scale deployments. Recently, it announced a definitive agreement to acquire 1touch, extending its EDC into data discovery, classification, contextualization and enrichment.

The non-GAAP gross margin came in at 71.4% compared with 69.2% in the prior-year quarter. Pure Storage reported a non-GAAP operating income of $226 million compared with $153 million in the year-ago quarter, boosted by strong revenues and solid gross margins. Non-GAAP operating margin reached 21.3%, up from 17.4%, demonstrating that scale and recurring revenues are improving profitability leverage.

In the fiscal fourth quarter, the company returned $127 million to shareholders by buying back 1.7 million shares. In fiscal 2026, it returned $343 million to shareholders by repurchasing 5.6 million shares. It has $329 million left from its existing $400 million share repurchase plan.

For first-quarter fiscal 2027, Pure Storage expects revenues of $990 million-$1.01 billion, up about 28% year over year at the midpoint. The non-GAAP operating income is expected to be $125-$135 million, with around 57% year-over-year growth at the midpoint. PSTG has entered fiscal 2027 with strong momentum and expects 47% of revenues in the first half, up two points year over year. At the midpoint, revenue expectations of $4.3–$4.4 billion suggests 18.8% year-over-year growth, with operating profit of $780–$820 million expected to rise about 26%.

Everpure is gaining from broad-based enterprise strength, accelerating AI-driven demand and expanding hyperscale momentum. The company’s Enterprise Data Cloud (EDC) architecture continues to resonate with customers, with more than 600 customers adopting Fusion within a year of its introduction. Management highlighted that focused investment in enterprise capabilities is translating into accelerating demand and growth. The company also stated that it can now support practically all enterprise storage needs across performance tiers, workloads and protocols through its unified Purity operating environment, DirectFlash architecture and Evergreen platform.

AI-focused offerings are contributing to momentum. FlashBlade//EXA, designed for AI-scale workloads, achieved industry-leading MLPerf benchmark performance and the highest results in the SPECstorage AI Image benchmark. During the fourth quarter, the company secured its first EXA customer and is in advanced-stage discussions with dozens more. Management noted strong initial market interest and demand for the offering.

Hyperscale performance exceeded expectations in fiscal 2026, with the company expanding its solution set and standardizing its financial structure. It expects significant acceleration in hyperscaler shipments and revenues in fiscal 2027, with the majority of hyperscaler revenues anticipated in the second half. Hyperscaler gross margins are expected to range between 75% and 85%, accretive to overall company margins. The company also reported increased breadth and engagement in hyperscaler discussions, with engineering test environments underway across multiple hyperscalers.

Pure Storage, Inc. price-consensus-chart | Pure Storage, Inc. Quote

The company is also benefiting from strong momentum in its subscription and recurring revenue streams. In the fourth quarter, subscription revenues increased 14% year over year, while annual recurring revenues (ARR) grew 16% year over year to $1.9 billion. Remaining performance obligations accelerated to 40% growth in the fourth quarter, driven by large deal execution and strength in Evergreen//Forever and Evergreen//One offerings. Total Contract Value sales for Storage-as-a-Service grew 28% in the fourth quarter and 32% for the full year, reflecting increasing customer adoption of subscription-based offerings. Large transactions also strengthened, with deals more than $5 million growing 80% year over year.

However, management stated that macroeconomic uncertainty is expected to persist and that AI-driven infrastructure demand has outstripped supply across the industry. This has led to dramatic increases in NAND, memory and CPU pricing, along with unpredictable component shortages, extended lead times and potential shipment delays. While the company maintains long-standing supply agreements and a diversified supply chain, it acknowledged limited visibility due to rapid market changes.

Rapid component cost increases have pressured near-term margins. The company implemented an average product price increase of approximately 20% on Feb. 9 to reflect rising input costs. It expects first-quarter product gross margins to be at the lower end of its typical 65-70% range before recovering later in the fiscal year. Additionally, the acquisition of 1touch is expected to be 1.5% dilutive to operating profit in fiscal 2027 before becoming accretive within 24 months.

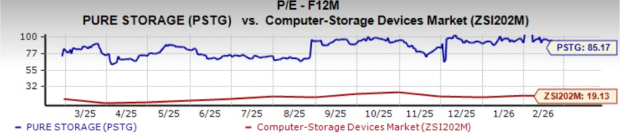

In terms of forward price/earnings, PSTG’s shares are trading at 85.17X, way higher than the industry’s 19.13X.

NTAP, STX and SNDK are trading at multiples of 14.38X, 25.62X and 17.39X, respectively.

Everpure’s strong enterprise momentum, expanding hyperscale opportunity and accelerating subscription growth bode well, but stretched valuation and near-term margin pressure from rising component costs are concerning.

Given the uncertainties, new investors could wait for a better entry point, while existing investors can hold the stock for long-term gains.

At present, PSTG carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 4 hours | |

| 5 hours | |

| 6 hours | |

| 6 hours | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite