|

|

|

|

|||||

|

|

|

Clover Health Investments, Corp. CLOV delivered an adjusted fourth-quarter 2025 loss per share of 5 cents, against the year-ago period’s adjusted earnings per share (EPS) of 2 cents. The bottom line was in line with the Zacks Consensus Estimate.

The company reported a GAAP loss of 10 cents per share from continuing operations, compared with a 4-cent loss in the year-ago period.

For 2025, Clover Health reported a loss per share of 17 cents, higher than the year-ago period’s loss of 9 cents. The company reported adjusted EPS of 4 cents in 2025, compared with an adjusted EPS of 14 cents in the year-ago period.

Clover Health registered total revenues of $487.7 million, up 44.7% year over year. The figure beat the Zacks Consensus Estimate by 3.2%.

The top line gained from robust Insurance revenues.

For 2025, CLOV registered total revenues of $1.92 billion, up 40.3% compared with 2024.

Clover Health Investments, Corp. price-consensus-eps-surprise-chart | Clover Health Investments, Corp. Quote

The company derives its revenues from two primary business segments — Insurance and Other income.

Insurance revenues in the fourth quarter totaled $485.9 million, up 46.9% year over year. According to management, this growth was primarily driven by a 38% increase in Medicare Advantage membership, strong member retention, clinical initiatives and the impact of Clover Assistant-powered care platform.

Within CLOV’s Insurance segment, the Insurance Benefit Expense Ratio (BER) was 95%, reflecting a modest year-over-year increase from 82.8% in the year-ago quarter. Insurance BER rose due to new member dilution and incremental quality investments.

Other income was $1.8 million, down 71% from the prior-year level.

In the quarter under review, Clover Health’s net medical claims increased 70.1% year over year to $413.5 million. Salaries and benefits expenses decreased 9.2% to $56.9 million, while general and administrative expenses rose 26.5% to $66.2 million. Total operating expenses of $537 million increased 49.8% on a year-over-year basis.

Total operating loss was $49.3 million compared with the prior-year quarter’s operating loss of $21.4 million.

The company exited fourth-quarter 2025 with cash and cash equivalents of $78.3 million compared with $190.1 million at the end of third-quarter 2025.

Net cash used in operating activities from continuing operations at the end of fourth-quarter 2025 was $66.9 million against $82.5 million of net cash provided by operating activities from continuing operations in the year-ago period.

Clover Health issued its revenue outlook for 2026.

For 2026, total revenues are estimated to be in the range of $2.81-$2.92 billion, suggesting 49% year-over-year growth at the midpoint. The Zacks Consensus Estimate is pegged at $2.62 billion.

The company now expects GAAP Net Income to be in the range of $0-$20 million. Average Medicare Advantage membership is now likely to be in the band of 154,000-158,000, implying 46% year-over-year growth at the midpoint.

Clover Health exited the fourth quarter of 2025 with better-than-expected sales while earnings were in line. The robust uptick in consolidated revenues and key Insurance segment revenues was encouraging. The company emphasized its continued progress in adjusted EBITDA profitability and a controlled underlying medical cost trend while delivering robust membership and revenue growth within Medicare Advantage.

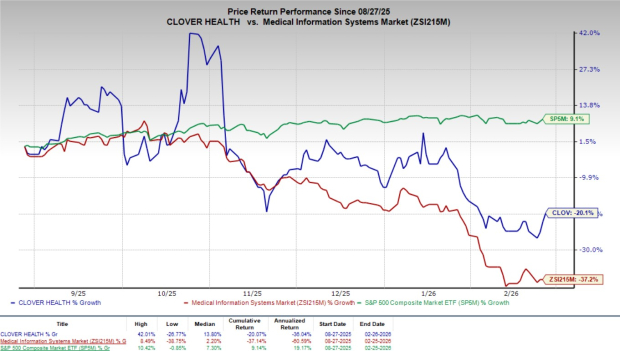

Shares of CLOV gained 2.3% during yesterday’s after-hours trading, following better-than-expected revenue guidance for 2026. The company’s shares have lost 20.1% in the past six months compared with the industry’s decline of 37.2%. However, the S&P 500 Index has increased 9.1% in the same time frame.

In 2025, CLOV demonstrated that its model can sustain profitability even amid elevated industry utilization and new member dilution. The company achieved full-year adjusted EBITDA profitability while growing Medicare Advantage membership 38% year over year, given its full-risk underwriting structure. Despite higher utilization across the industry and operating in a 3.5-star payment year, CLOV kept medical costs under control and maintained disciplined pricing. Growth was driven by stable benefits, strong AEP retention above 95% and focused expansion in core New Jersey markets, where Clover Assistant penetration is highest. The company also reestablished market-leading membership growth during the 2026 AEP, up 53% year over year, underscoring the repeatability of its playbook.

CLOV enters 2026 with over 95% AEP retention and strong Clover Assistant engagement, with two-thirds of members receiving Assistant-powered care in 2025. Management expects 2026 to mark its first full year of GAAP net income profitability, supported by stronger cohort economics. While new members create near-term margin pressure, profitability improves as cohorts mature. A 4-star payment year expected in 2026, along with favorable rate dynamics and earlier care management, is anticipated to strengthen earnings visibility and sustained growth.

Beyond 2026, CLOV believes its encounter-based, clinically integrated approach aligns with evolving Medicare Advantage regulatory direction. Management supports efforts to tie payments closely to documented care, noting its approach focuses on real physician workflows through Clover Assistant. The company views itself as less dependent on rate increases or star upgrades, supported by strong New Jersey PPO leadership and the ability to grow profitably even in a 3.5-star environment. Beyond MA, Counterpart Health leverages the same technology platform, with plans to expand covered lives and clinician adoption, positioning it as a long-term growth driver.

Clover Health currently has a Zacks Rank #3 (Hold).

Some better-ranked stocks in the broader medical space are Intuitive Surgical ISRG, AngioDynamics ANGO and Alcon ALC.

Intuitive Surgical, sporting a Zacks Rank #1 (Strong Buy) at present, has an estimated long-term growth rate of 15.7%. ISRG’s earnings surpassed estimates in each of the trailing four quarters, with the average surprise being 13.2%. You can see the complete list of today’s Zacks #1 Rank stocks here.

Intuitive Surgical’s shares have gained 7.6% against the industry’s 3% decline in the past six months.

AngioDynamics, sporting a Zacks Rank #1 at present, has an estimated earnings growth rate of 59.3% for 2026. ANGO’s earnings surpassed estimates in each of the trailing four quarters, with the average surprise being 82.1%.

AngioDynamics’s shares have climbed 14.5% against the industry’s 3% decline in the past six months.

Alcon, carrying a Zacks Rank of 2 (Buy) at present, has an estimated long-term growth rate of 6.2%. ALC’s earnings surpassed estimates in two of the trailing four quarters and missed twice, with the average surprise being 1.1%.

Alcon’s shares have risen 6.6% against the industry’s 3% decline in the past six months.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-21 | |

| Jul-21 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-18 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite