|

|

|

|

|||||

|

|

|

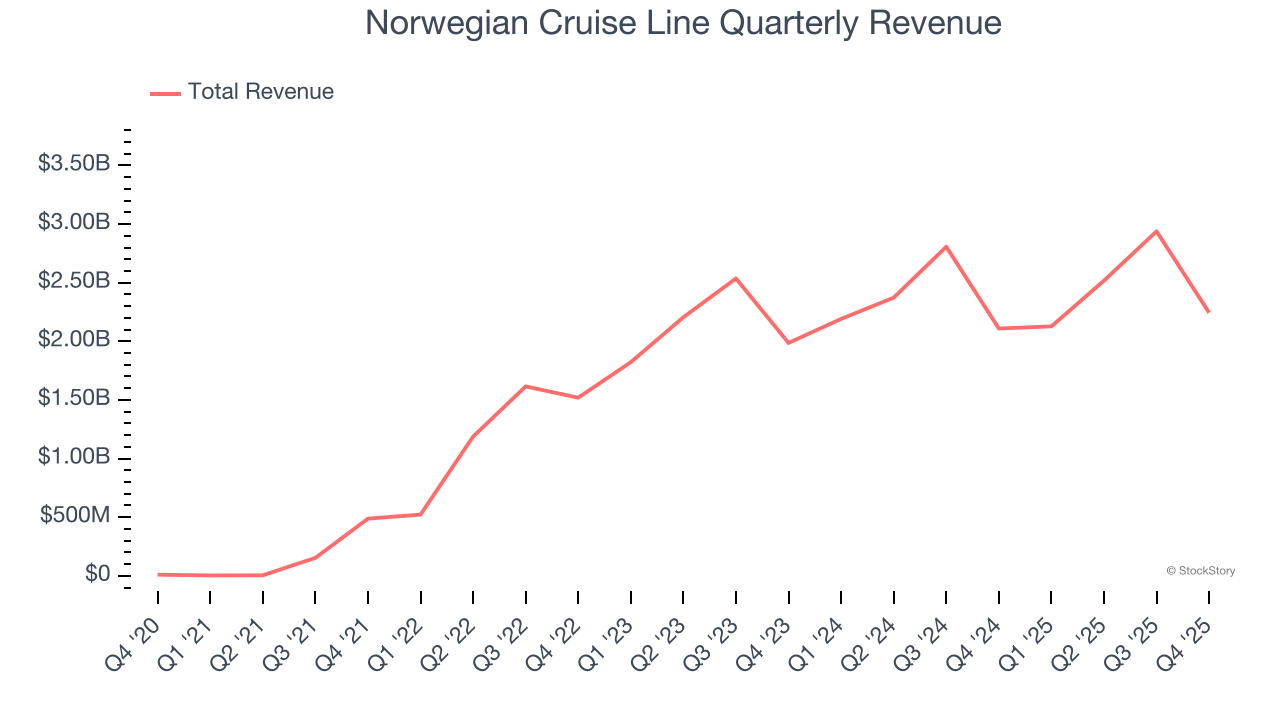

Cruise company Norwegian Cruise Line (NYSE:NCLH) fell short of the market’s revenue expectations in Q4 CY2025, but sales rose 6.4% year on year to $2.24 billion. Its non-GAAP profit of $0.28 per share was 5.5% above analysts’ consensus estimates.

Is now the time to buy Norwegian Cruise Line? Find out by accessing our full research report, it’s free.

“The team delivered solid fourth quarter and full year 2025 results reflecting the strength of our award-winning brands, loyal guests and dedication of our team and crew members,” said John W. Chidsey, president and chief executive officer of Norwegian Cruise Line Holdings Ltd.

With amenities like a full go-kart race track built into its ships, Norwegian Cruise Line (NYSE:NCLH) is a premier global cruise company.

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, Norwegian Cruise Line grew its sales at a solid 50.3% compounded annual growth rate. Its growth beat the average consumer discretionary company and shows its offerings resonate with customers.

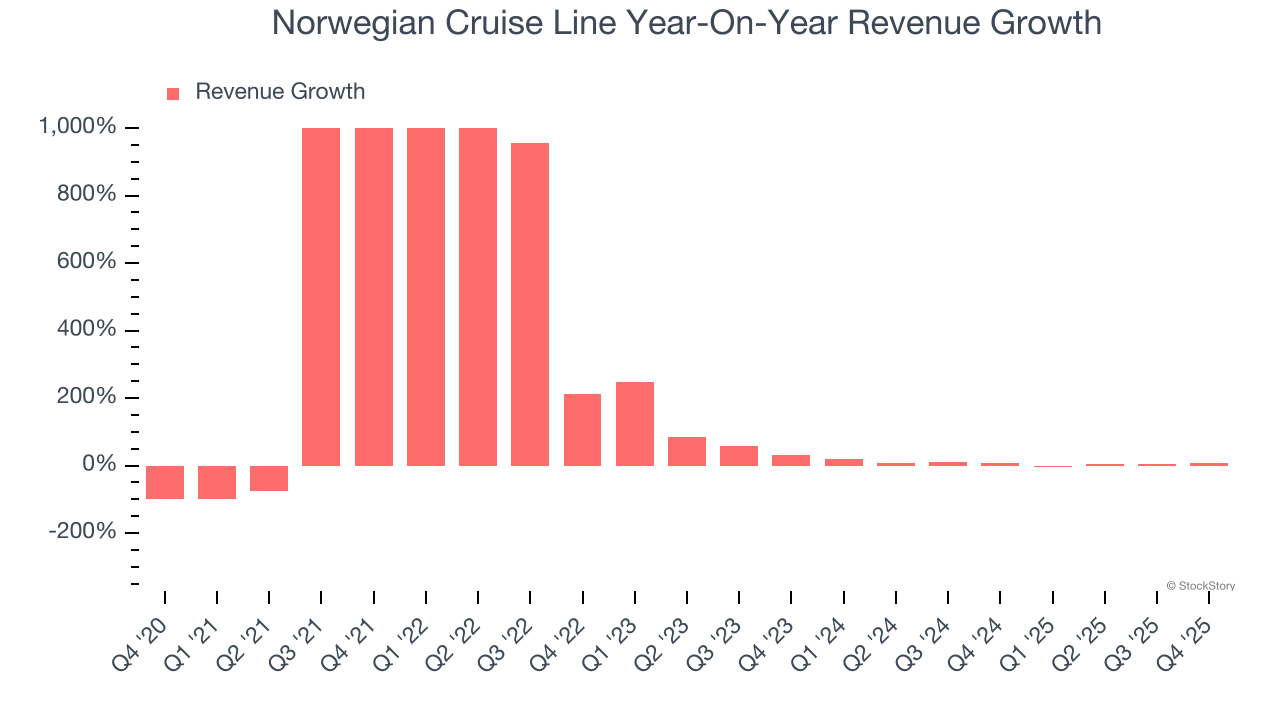

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new property or trend. Norwegian Cruise Line’s recent performance shows its demand has slowed as its annualized revenue growth of 7.2% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

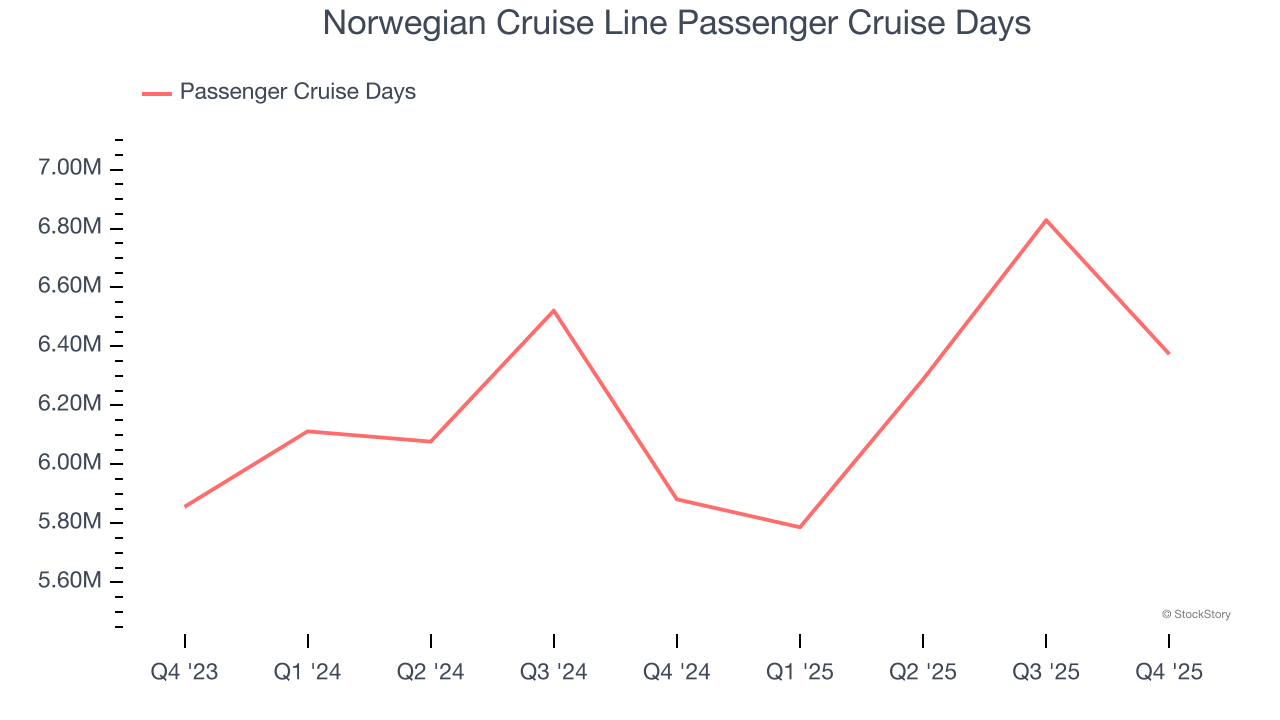

We can better understand the company’s revenue dynamics by analyzing its number of passenger cruise days, which reached 6.37 million in the latest quarter. Over the last two years, Norwegian Cruise Line’s passenger cruise days averaged 2.3% year-on-year growth. Because this number is lower than its revenue growth during the same period, we can see the company’s monetization has risen.

This quarter, Norwegian Cruise Line’s revenue grew by 6.4% year on year to $2.24 billion, missing Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 10.6% over the next 12 months. Although this projection suggests its newer products and services will fuel better top-line performance, it is still below average for the sector.

While Wall Street chases Nvidia at all-time highs, an under-the-radar semiconductor supplier is dominating a critical AI component these giants can’t build without. Click here to access our free report one of our favorites growth stories.

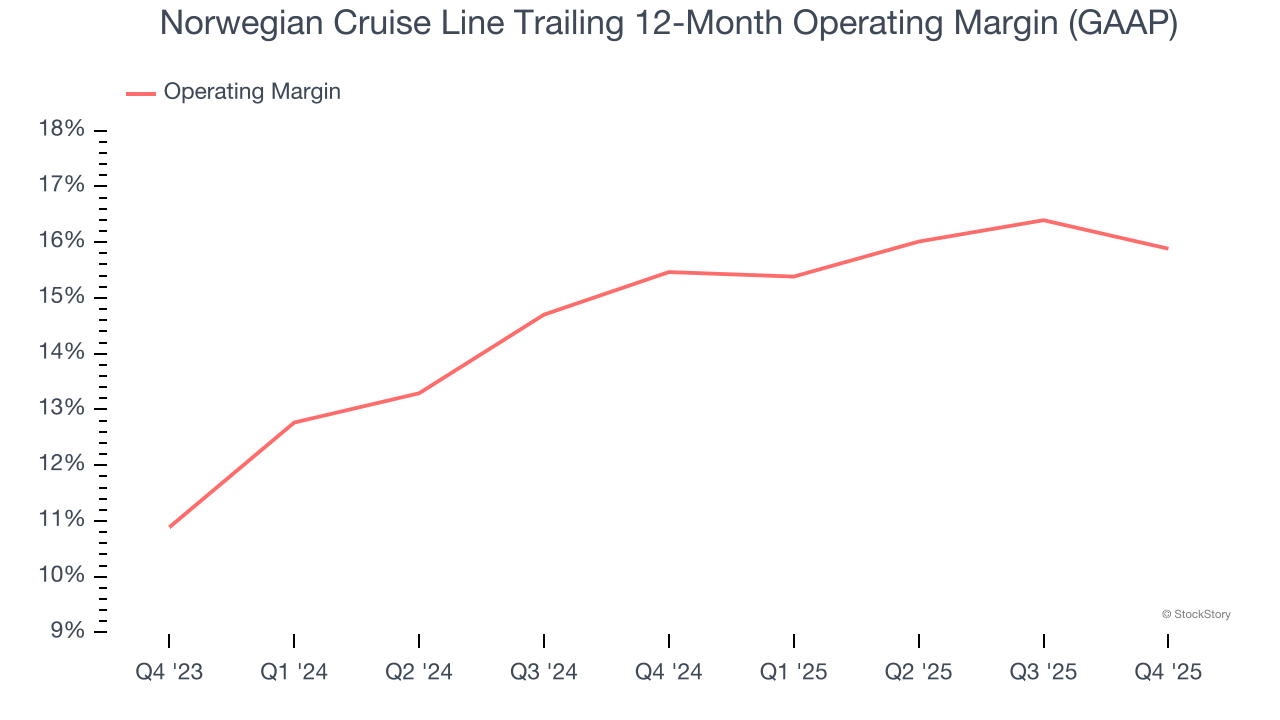

Norwegian Cruise Line’s operating margin might fluctuated slightly over the last 12 months but has remained more or less the same, averaging 15.7% over the last two years. This profitability was inadequate for a consumer discretionary business and caused by its suboptimal cost structure.

This quarter, Norwegian Cruise Line generated an operating margin profit margin of 8.3%, down 1.9 percentage points year on year. This reduction is quite minuscule and indicates the company’s overall cost structure has been relatively stable.

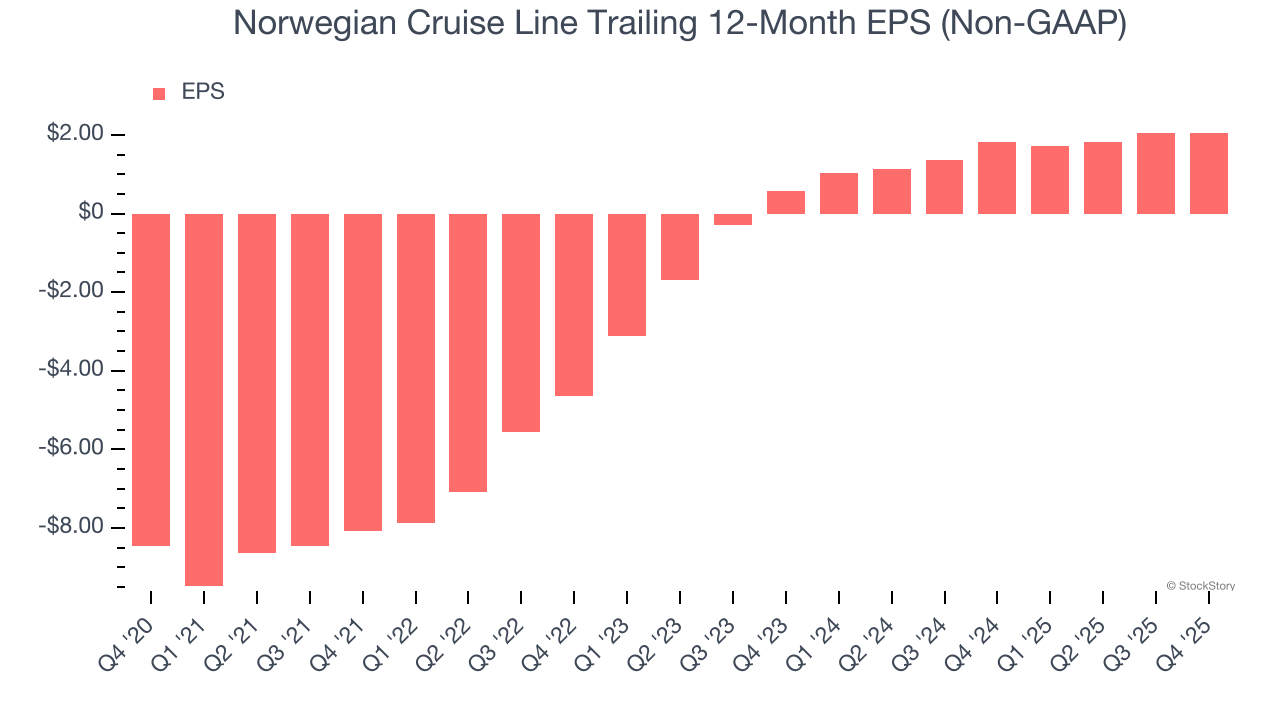

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Norwegian Cruise Line’s full-year EPS flipped from negative to positive over the last five years. This is encouraging and shows it’s at a critical moment in its life.

In Q4, Norwegian Cruise Line reported adjusted EPS of $0.28, up from $0.26 in the same quarter last year. This print beat analysts’ estimates by 5.5%. Over the next 12 months, Wall Street expects Norwegian Cruise Line’s full-year EPS of $2.06 to grow 24.1%.

It was good to see Norwegian Cruise Line provide EBITDA guidance for next quarter that slightly beat analysts’ expectations. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its revenue missed and its full-year EBITDA guidance fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 7% to $23.07 immediately after reporting.

Norwegian Cruise Line underperformed this quarter, but does that create an opportunity to invest right now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).

| 9 hours | |

| Jul-16 | |

| Jul-15 | |

| Jul-08 | |

| Jul-08 | |

| Jul-07 | |

| Jun-30 | |

| Jun-29 | |

| Jun-22 | |

| Jun-17 | |

| Jun-16 | |

| Jun-15 | |

| Jun-15 | |

| Jun-12 | |

| Jun-08 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite