|

|

|

|

|||||

|

|

|

PulteGroup currently trades at $136.99 per share and has shown little upside over the past six months, posting a middling return of 3.7%.

Is there a buying opportunity in PulteGroup, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

We're cautious about PulteGroup. Here are three reasons there are better opportunities than PHM and a stock we'd rather own.

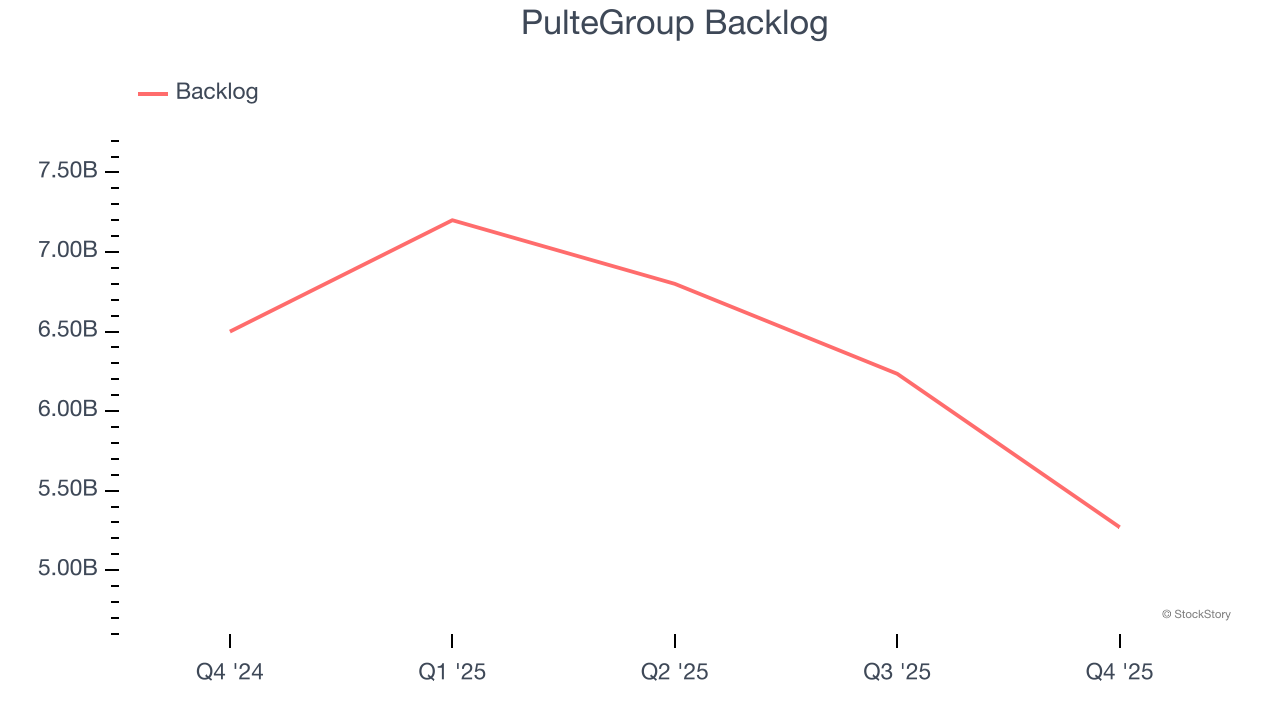

In addition to reported revenue, backlog is a useful data point for analyzing Home Builders companies. This metric shows the value of outstanding orders that have not yet been executed or delivered, giving visibility into PulteGroup’s future revenue streams.

PulteGroup’s backlog came in at $5.27 billion in the latest quarter, and it averaged 18.9% year-on-year declines over the last two years. This performance was underwhelming and shows the company is not winning new orders. It also suggests there may be increasing competition or market saturation.

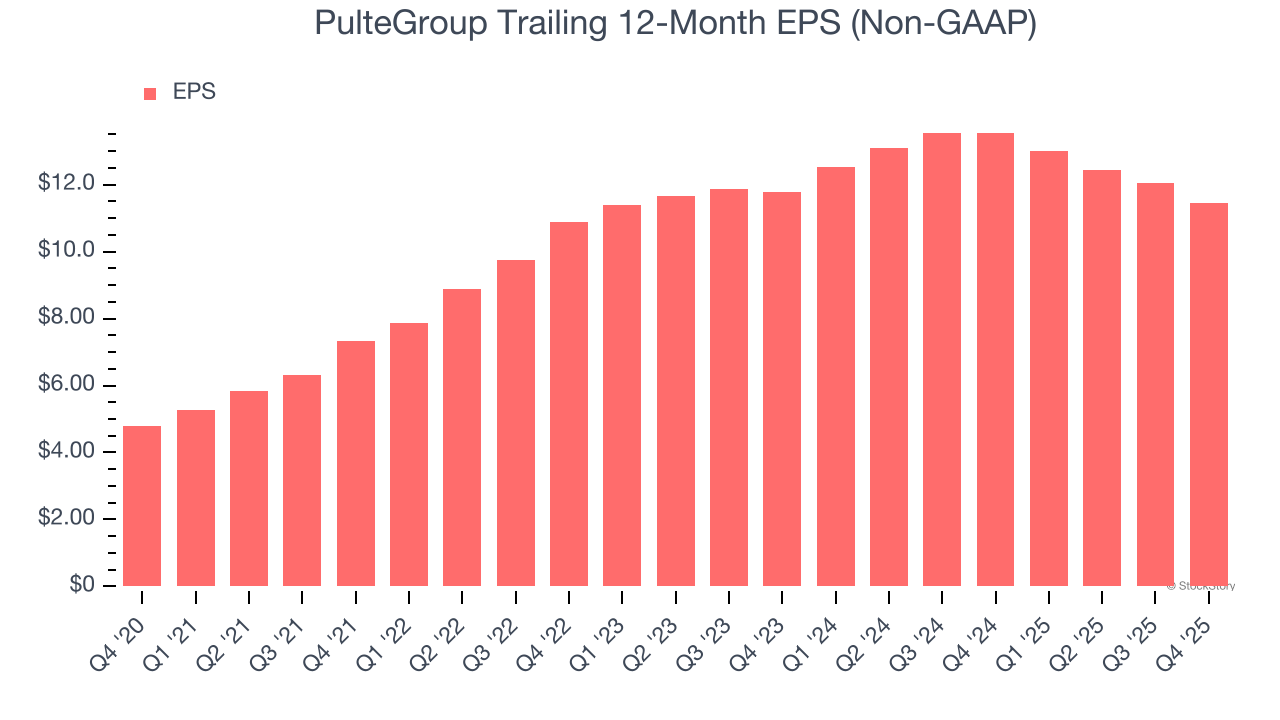

While long-term earnings trends give us the big picture, we also track EPS over a shorter period because it can provide insight into an emerging theme or development for the business.

Sadly for PulteGroup, its EPS declined by 1.4% annually over the last two years while its revenue grew by 3.8%. This tells us the company became less profitable on a per-share basis as it expanded.

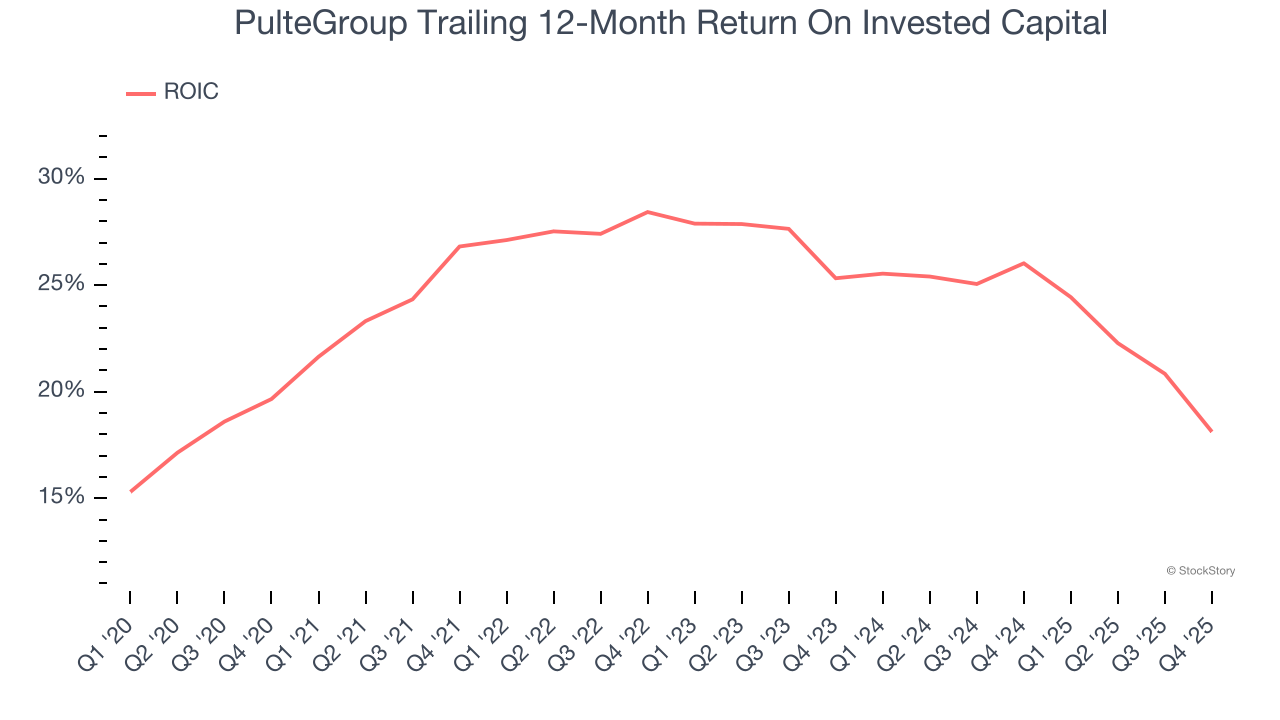

We like to invest in businesses with high returns, but the trend in a company’s ROIC can also be an early indicator of future business quality.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, PulteGroup’s ROIC has decreased over the last few years. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

PulteGroup isn’t a terrible business, but it doesn’t pass our bar. That said, the stock currently trades at 13.3× forward P/E (or $136.99 per share). This valuation is reasonable, but the company’s shakier fundamentals present too much downside risk. We're pretty confident there are more exciting stocks to buy at the moment. Let us point you toward the Amazon and PayPal of Latin America.

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-21 | |

| Jul-21 | |

| Jul-16 | |

| Jul-10 | |

| Jul-07 | |

| Jun-29 | |

| Jun-24 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite