|

|

|

|

|||||

|

|

|

Owlet, Inc. OWLT is scheduled to report fourth-quarter 2025 results on March 5, after the closing bell.

In the last reported quarter, the company’s earnings and revenues beat the Zacks Consensus Estimate by 113% and 20.5%, respectively. On a year-over-year basis, the top line increased 44.6%, while the bottom line remained flat.

OWLT’s earnings topped the consensus mark in each of the trailing three quarters. The average surprise is shown in the chart below.

The Zacks Consensus Estimate for the fourth-quarter loss per share has remained unchanged at 13 cents over the past 30 days. The estimated figure implies 85.7% decline from the year-ago reported figure. The consensus mark for revenues is $25.4 million, indicating 24.1% year-over-year growth.

For 2025, Owlet is expected to register a 34% increase from a year ago in revenues. Its bottom line is expected to grow 66.7% from a year ago. Below is what to expect from OWLT stock.

Our proven model does not predict an earnings beat for Owlet for the quarter to be reported. That is because a stock needs to have both a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy), or 3 (Hold) for this to happen. This is not the case here, as you will see below.

Earnings ESP: OWLT has an Earnings ESP of 0.00%. You can uncover the best stocks to buy or sell before they are reported with our Earnings ESP Filter.

Zacks Rank: The company currently sports a Zacks Rank #1. You can see the complete list of today’s Zacks #1 Rank stocks here.

Owlet’s fourth-quarter 2025 revenues are expected to have gained year over year on the back of its ongoing transition from a hardware-focused baby monitor company to a data-enabled pediatric health platform. The company continues to benefit from stronger brand positioning, subscription growth and expanding international reach. Regulatory clarity and product innovation are likely to have supported demand during the quarter.

A key positive for the quarter is expected to have been regulatory differentiation. Owlet remains the first and only FDA-cleared over-the-counter infant monitoring device company in the market. The recent FDA safety communication against unauthorized infant monitors is likely to have strengthened Owlet’s competitive positioning. This distinction is expected to have reinforced brand trust among parents, retailers and healthcare partners. The regulatory edge might have helped the company sustain market share gains during the quarter.

Subscription and platform expansion are expected to have remained central to the growth story. Paying subscribers surpassed 85,000 as of the end of the third quarter, with attach rates exceeding 25%. The large installed base of more than 650,000 active devices provides room for further subscription conversion. Owlet360 momentum is likely to have continued in the fourth quarter, supported by international rollout and added camera-based features linked to Dream Sight’s onboard AI capabilities.

The company has also been preparing to pilot generative AI features in 2026 to deliver personalized sleep insights and coaching. These initiatives are expected to support engagement and retention over time. The continued shift toward software and services is likely to have supported margin stability through a higher mix of recurring revenues.

International expansion is expected to have provided additional support. Regulatory approval in India opens another growth avenue starting early 2026. Early progress in healthcare partnerships and remote patient monitoring programs might have added long-term optionality, though healthcare contributions are expected to have remained modest in the near term.

However, tariff pressures are likely to have weighed on margins during the quarter, with elevated import costs expected to persist. Consumer demand might have remained sensitive amid broader macro uncertainty, including a cautious spending environment and the aftereffects of the government shutdown. Tariff policies could also have impacted the important fourth-quarter holiday sales period. While the shift toward higher-margin software and services is expected to have provided some support, continued cost pressures and ongoing investments are likely to have led to a year-over-year decline in the bottom line.

Shares of Owlet have surged 53.2% over the past six months, outperforming the Zacks Electronics - Miscellaneous Products industry, Zacks Computer and Technology sector and the S&P 500 Index, as shown below.

Owlet stock has outperformed some other players, including Masimo MASI, iRhythm Technologies IRTC and Koninklijke Philips N.V. PHG in the past six months. In the said time frame, Masimo and Koninklijke Philips have gained 28.2% and 17.8%, respectively, while iRhythm Technologies declined 24.3%.

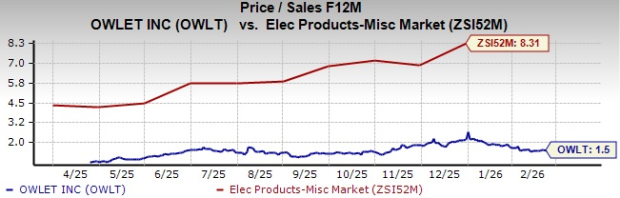

Owlet’s shares are currently trading at a forward 12-month price-to-sales (P/S) ratio of 1.5, an 81.9% discount to the industry average of 8.31.

Other peer companies, Masimo, Koninklijke Philips and iRhythm Technologies, have a forward P/S of 5.74, 4.85 and 1.39, respectively.

Owlet is expected to have made steady progress in the fourth quarter, supported by its shift toward a data-enabled pediatric health platform. Regulatory differentiation, subscription growth and expanding international presence are likely to have supported the business. The company’s focus on recurring revenues and software-led offerings continues to strengthen the long-term story.

However, near-term pressure on margins and earnings remains a concern due to tariffs, cost headwinds and a cautious consumer environment. While the transformation is progressing, profitability may take time to stabilize. Investors may view OWLT stock as a longer-term opportunity tied to platform expansion and regulatory strength, while remaining mindful of near-term earnings pressure.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-23 | |

| Jul-21 | |

| Jul-17 | |

| Jul-16 | |

| Jul-08 | |

| Jul-03 | |

| Jun-30 | |

| Jun-22 | |

| Jun-17 | |

| Jun-16 | |

| Jun-09 | |

| Jun-09 | |

| Jun-09 | |

| Jun-09 | |

| Jun-09 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite