|

|

|

|

|||||

|

|

|

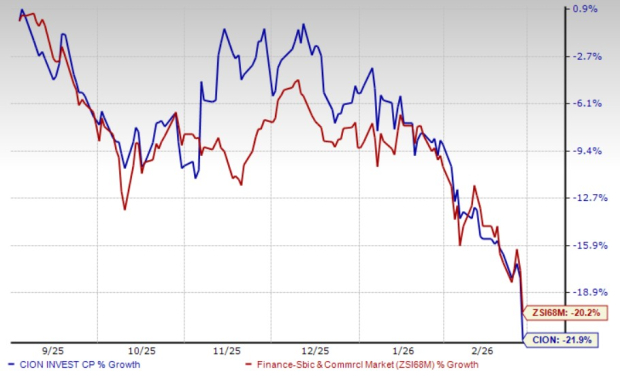

CION Investment Corporation CION is flashing the kind of yield that stops income investors mid-scroll. The dividend yield is higher, but the the stock has declined 21.9% over six months compared with the industry decline of 20.2%.

Price Performance

That mix sets up the real question: is the market saying “cheap for a reason,” or is this a mispriced income stream that can recover if credit trends stabilize

CION trades at 5.5x forward 12-month earnings, well below the 8.26x multiple for the Zacks sub-industry. The gap widens versus the broader Zacks Finance sector at 16.35x and the S&P 500 at 22.49x.

P/E F12M

Moreover, the dividend yield is 15.04%. At $7.98, CION Investment is priced like a caution sign, not an income opportunity. The yield is large because the share price has slid, and the market is clearly demanding compensation for risk.

CION Investment Corporation Dividend Yield (TTM)

CION Investment Corporation dividend-yield-ttm | CION Investment Corporation Quote

CION’s third-quarter 2025 results showed how strong quarters can look when multiple levers fire at once. Total investment income reached $78.7 million, driven by higher interest income and elevated transaction fees. Net investment income was 74 cents per share, and distribution coverage strengthened to 2.06x, helped by outsized fee activity tied to the Juice Plus opportunistic transaction.

The key for readers is to separate repeatable net interest income from episodic fee upside. Fee-driven strength can lift coverage sharply in a given quarter, but investors should not assume the same mix will recur every period.

The income case is not without support. CION’s portfolio has remained heavily first-lien, with most assets floating-rate and liabilities largely unsecured, which can help align funding and asset yields while preserving flexibility. Leverage has also been managed within a stated 1.25x-1.30x target range, with net debt-to-equity at 1.28x.

Liquidity is another buffer. As of Sept. 30, 2025, the company held $106 million in cash and short-term investments and had $100 million available under financing arrangements. Management has also emphasized selectivity in a competitive private credit market, and third-quarter 2025 activity reflected de-risking, with repayments and sales exceeding new commitments.

For income investors, the setup calls for monitoring rather than blind yield-chasing. Start with the direction of Credit quality. Non-accruals rose sharply beginning in the second quarter of 2025, reaching 1.75% of fair value and 4.08% of the total investment portfolio by the third quarter of 2025. That direction matters because non-accruals are often an early signal of future pressure on income and valuations.

Next, watch net asset value stability. Net asset value per share was $14.86 in the third quarter of 2025, down 5.5% year over year, reflecting mark-downs and prior-period losses alongside recent equity appreciation. Stabilization here would help support confidence in marks and earnings quality.

Finally, focus on distribution coverage after fee activity normalizes, and whether origination spreads remain consistent with traditional middle-market levels as management expects. Share repurchases can also be a support lever when the stock trades at a discount, and CION repurchased shares in the third quarter of 2025 with expectations to continue.

CION’s long-term view is Neutral, while the short-term Zacks Rank is #3 (Hold). That combination fits an “income with credit-risk monitoring” profile: the valuation discount and yield are compelling, but rising non-accruals and competitive pressure can keep the multiple compressed. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Its peers, Ares Capital ARCC and Main Street Capital MAIN also hold a Zacks Rank of 3, at present. Both trades at premium compared to CION. Ares Capital and Main Street Capital trades at a forward 12-month earnings of 14.12x and 9.61x, respectively.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-31 | |

| Jul-31 | |

| Jul-30 | |

| Jul-30 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-17 | |

| Jul-16 | |

| Jul-14 | |

| Jul-09 | |

| Jul-02 | |

| Jul-01 | |

| Jun-30 | |

| Jun-24 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite