|

|

|

|

|||||

|

|

|

Veeva Systems VEEV is scheduled to report fiscal fourth-quarter 2026 results on March 04, after the closing bell.

In the last reported quarter, the company’s earnings per share (EPS) of $2.04 topped the Zacks Consensus Estimate by 4.62%. Over the trailing four quarters, its earnings outperformed the Zacks Consensus Estimate on all the occasions, delivering an earnings surprise of 8.18%, on average.

Let’s check out the factors that have shaped VEEV’ performance prior to this announcement.

Ahead of the fiscal fourth-quarter results, investors should focus on segment-level trends across Subscription and Professional Services. Subscription revenue, the core of Veeva Systems’ business and its primary margin driver, has been fueled by steady demand for R&D, Quality and Crossix solutions, and investors will look for sustained double-digit growth in the fiscal fourth quarter to reaffirm the durability of its recurring model. Professional Services, while more implementation-driven and lumpy, is likely to reflect ongoing Vault CRM migrations and Development Cloud rollouts; stable demand and improving utilization would indicate continued platform expansion, even if near-term hiring weighs modestly on margins.

As Veeva Systems heads into its fiscal fourth-quarter earnings, the biggest focus remains the ongoing Vault CRM transition cycle. In the fiscal third quarter, management acknowledged that while the majority of top 20 biopharma customers are expected to migrate to Vault CRM, a few are opting for alternative paths. Importantly, VEEV emphasized that CRM now contributes roughly 20% of total revenue, meaning the broader business is far more diversified than it was a few years ago. Investors should closely monitor the fiscal fourth-quarter commentary around additional migration commitments, competitive dynamics, and the pace of customer conversions. Any clarity around revenue retention, win-backs, or incremental cross-sell within the CRM suite will be key in assessing the durability of Veeva Systems’ commercial franchise.

Another critical theme for VEEV’s fiscal fourth-quarter earnings will be AI integration and monetization across its product portfolio. Veeva Systems has accelerated its rollout of AI agents across Commercial, Safety, Quality, and Clinical applications, positioning AI as both a productivity enhancer and a long-term revenue driver. In commercial use cases, AI is expected to enhance field insights and marketing effectiveness, while in Safety and Clinical, it could materially reduce labor-intensive processes such as adverse event case handling and document review. Investors should look for early customer adoption signals, pricing commentary, and whether AI is beginning to influence deal sizes or pipeline velocity. Any measurable traction could reinforce confidence that AI will meaningfully expand VEEV’s total addressable market rather than simply enhance existing workflows.

Finally, investors should pay attention to growth drivers outside CRM, particularly Crossix and Development Cloud. Crossix has been a standout performer, benefiting from increased pharma digital marketing spend and stronger demand for audience measurement and optimization tools. Continued momentum here would support the narrative that Veeva Systems’ Commercial Cloud extends well beyond CRM and could become an increasingly important growth engine.

On the R&D side, updates around Safety, eTMF leadership, and adoption of newer modules such as RTSM, eCOA and LIMS is likely to be important. Since R&D and Quality collectively represent the majority of VEEV’s revenue mix and tend to be more predictable, sustained strength in these areas would reinforce the company’s diversified growth profile heading into fiscal 2027.

Veeva Systems Inc. price-eps-surprise | Veeva Systems Inc. Quote

For fourth-quarter fiscal 2026, the Zacks Consensus Estimate for revenues is pegged at $808.9 million, implying an improvement of 12.2% from the prior-year quarter’s reported figure.

The consensus estimate for EPS is pegged at $1.92, indicating growth of 10.3% from the prior-year period’s reported number.

Per our proven model, a stock with a Zacks Rank #1 (Strong Buy), 2 (Buy), or 3 (Hold), along with a positive Earnings ESP, has higher chances of beating estimates. This is not the case here, as you can see below.

Earnings ESP: VEEV has an Earnings ESP of 0.00%. You can uncover the best stocks to buy or sell before they are reported with our Earnings ESP Filter.

Zacks Rank: The company currently carries a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank stocks here.

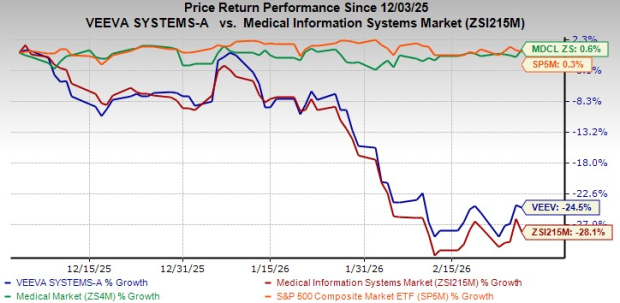

Over the past three months, Veeva Systems shares have plunged 24.5%, underperforming the broader Medical Info Systemsindustry, which fell 28.1% over the same period.

However, VEEV has significantly lagged the broader market, with the S&P 500 gaining 0.3% and the broader Zacks Medical sector rising 0.6% during this timeframe.

VEEV’s peers such as IQVIA IQV, Salesforce CRM and Schrodinger SDGR have also faced pressure over the same period. IQV shares have plunged 21.4%, CRM has lost 18.4%, while SDGR has plummeted 32.1%.

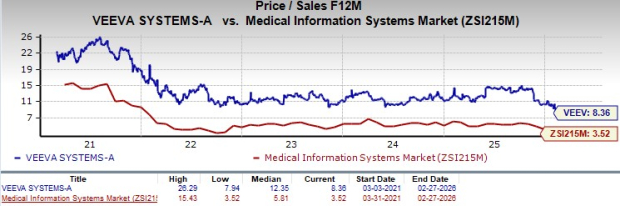

From a valuation standpoint, VEEV’s forward 12-month price-to-sales (P/S) is 8.4X, a premium to the industry's average of 3.5X while a discount to its five-year median of 12.4X.

The company is trading at a premium to its peers, IQVIA, Salesforce and Schrodinger. IQV and CRM’s P/S currently stand at 1.8X and 3.9X, respectively, while the ratio for SDGR stands at 2.8X.

This suggests that investors may be paying a higher price relative to the company's expected sales growth.

Veeva Systems offers strong long-term visibility driven by its expanding Industry Cloud strategy and diversified revenue mix. While CRM migration headlines have drawn attention, CRM now represents only about 20% of total revenue, with R&D, Safety and Quality forming a larger and more predictable base. Deep adoption of mission-critical products like eTMF across top biopharma customers, along with newer modules such as RTSM, eCOA and LIMS, positions VEEV to capture incremental share across the full drug development and manufacturing lifecycle. This diversification reduces reliance on any single segment and supports management’s confidence in its long-term targets.

Another key strength is Veeva Systems’ integrated model spanning software, data and consulting. By building a unified platform across Commercial and R&D Clouds — and operating independently of Salesforce infrastructure, VEEV gains greater product control, cross-sell flexibility and long-term margin leverage. As life sciences companies increasingly prefer standardized, end-to-end solutions over fragmented point products, Veeva Systems’ platform depth strengthens customer stickiness and competitive positioning.

Finally, AI represents a meaningful structural growth driver. VEEV is embedding domain-specific AI agents across Safety, Clinical and Commercial applications to improve efficiency, automate labor-intensive workflows and enhance insight generation. As adoption scales, AI could expand wallet share, support pricing power and further differentiate Veeva Systems in regulated markets. Together, platform breadth, recurring revenue durability and AI-driven innovation provide solid long-term growth and margin visibility.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite