|

|

|

|

|||||

|

|

|

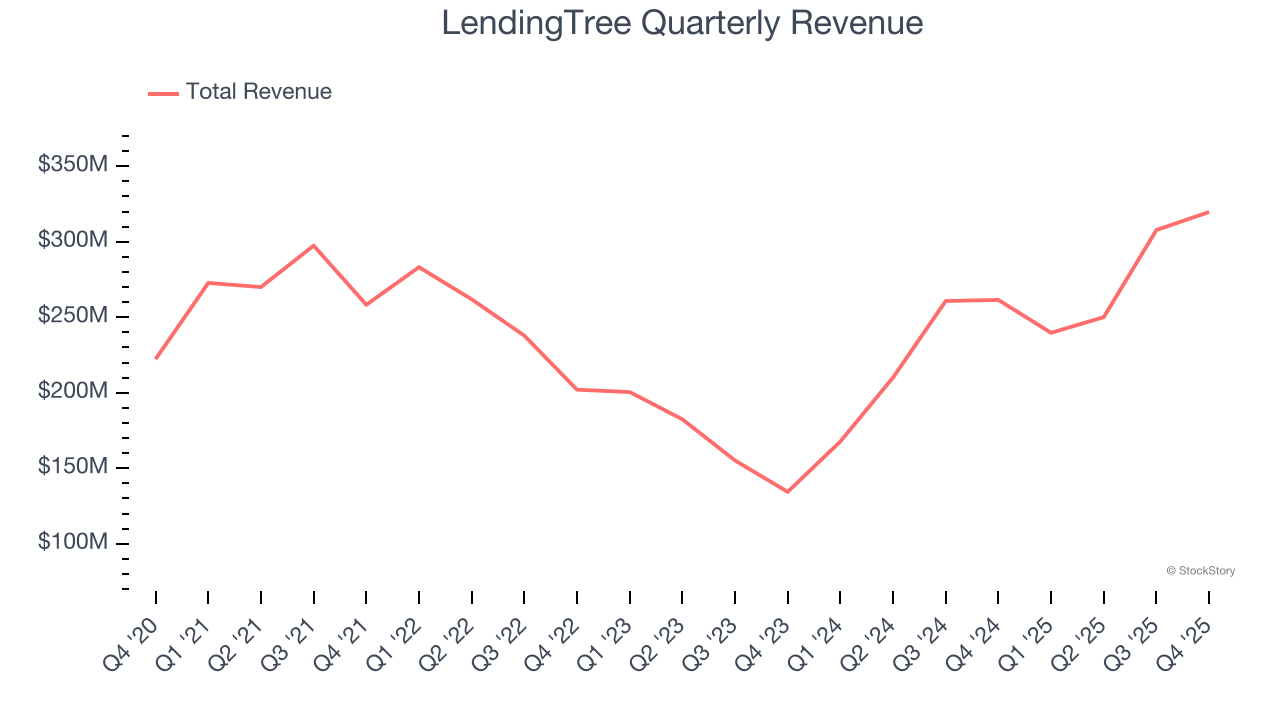

Financial marketplace platform LendingTree (NASDAQ:TREE) beat Wall Street’s revenue expectations in Q4 CY2025, with sales up 22.3% year on year to $319.7 million. On top of that, next quarter’s revenue guidance ($321 million at the midpoint) was surprisingly good and 16.5% above what analysts were expecting. Its non-GAAP loss of $0.39 per share was significantly below analysts’ consensus estimates.

Is now the time to buy LendingTree? Find out by accessing our full research report, it’s free.

Using the same comparison model that revolutionized travel booking, LendingTree (NASDAQ:TREE) operates an online platform that connects consumers with financial service providers across mortgages, personal loans, credit cards, insurance, and other financial products.

A company’s long-term performance is an indicator of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Regrettably, LendingTree’s sales grew at a sluggish 4.3% compounded annual growth rate over the last three years. This was below our standard for the consumer internet sector and is a tough starting point for our analysis.

This quarter, LendingTree reported robust year-on-year revenue growth of 22.3%, and its $319.7 million of revenue topped Wall Street estimates by 11.5%. Company management is currently guiding for a 33.9% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 3.5% over the next 12 months, similar to its three-year rate. This projection doesn't excite us and suggests its newer products and services will not lead to better top-line performance yet.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

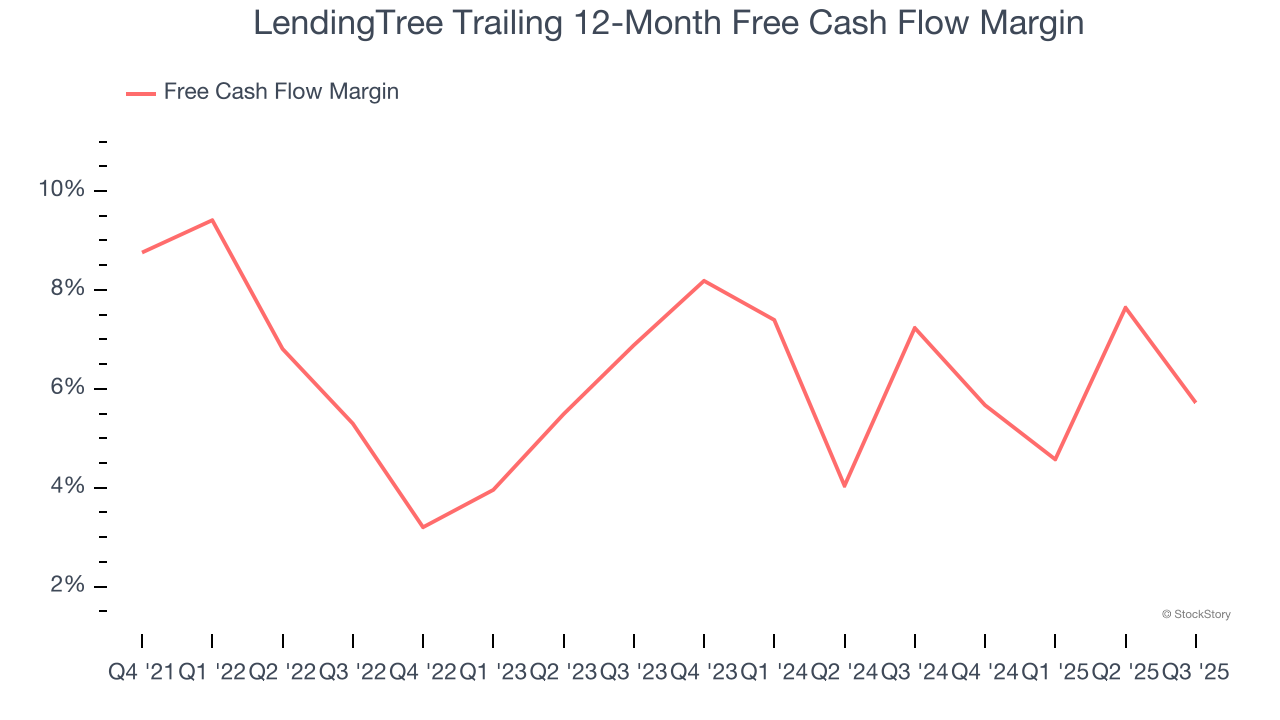

Although EBITDA is undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

LendingTree has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 5.8% over the last two years, slightly better than the broader consumer internet sector.

Taking a step back, we can see that LendingTree’s margin expanded by 3.7 percentage points over the last few years. This is encouraging because it gives the company more optionality.

We were impressed by LendingTree’s optimistic EBITDA guidance for next quarter, which blew past analysts’ expectations. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a good print with some key areas of upside. The stock traded up 14.7% to $43.29 immediately after reporting.

Indeed, LendingTree had a rock-solid quarterly earnings result, but is this stock a good investment here? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).

| Jul-14 | |

| Jul-09 | |

| Jul-07 | |

| Jul-06 | |

| Jun-11 | |

| May-07 | |

| May-04 | |

| May-03 | |

| May-01 | |

| Apr-30 | |

| Apr-30 | |

| Apr-22 | |

| Apr-15 | |

| Apr-14 | |

| Apr-14 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite