|

|

|

|

|||||

|

|

|

What a brutal six months it’s been for Boston Scientific. The stock has dropped 29% and now trades at $76.39, rattling many shareholders. This might have investors contemplating their next move.

Following the drawdown, is now the time to buy BSX? Find out in our full research report, it’s free.

Founded in 1979 with a mission to advance less-invasive medicine, Boston Scientific (NYSE:BSX) develops and manufactures medical devices used in minimally invasive procedures across cardiovascular, urological, neurological, and gastrointestinal specialties.

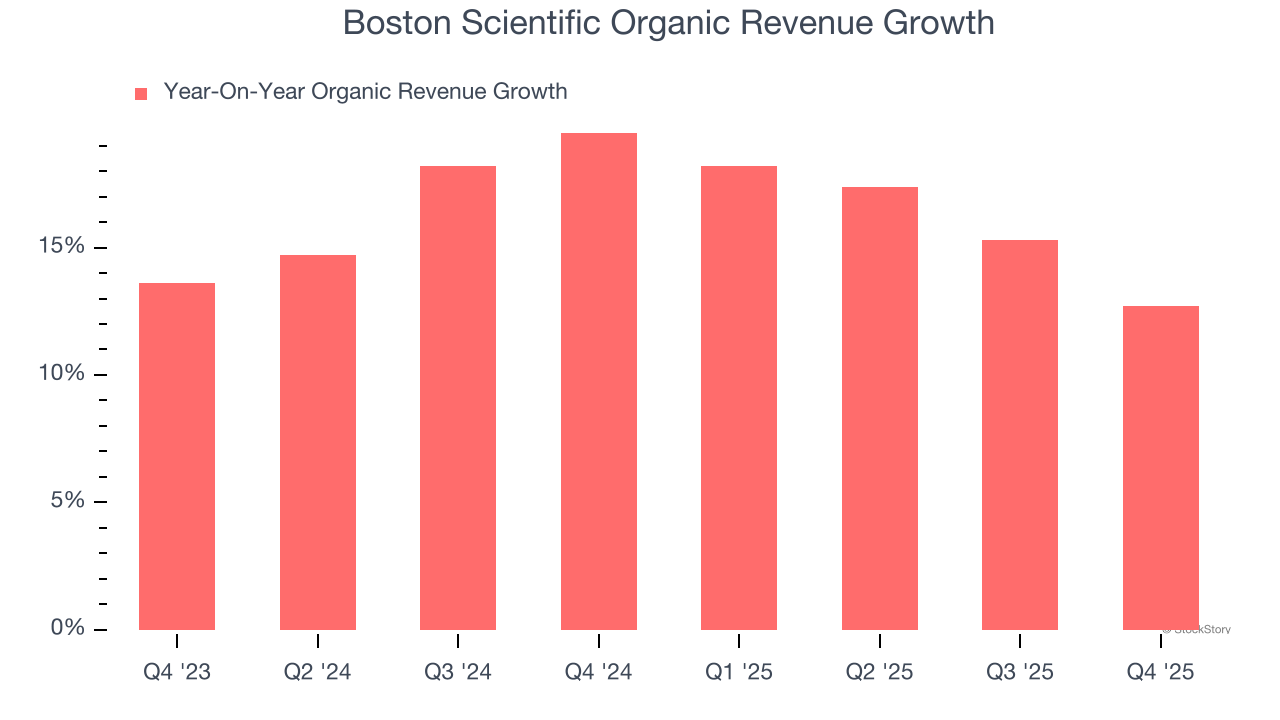

Investors interested in Medical Devices & Supplies - Diversified companies should track organic revenue in addition to reported revenue. This metric gives visibility into Boston Scientific’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, Boston Scientific’s organic revenue averaged 16.6% year-on-year growth. This performance was impressive and shows it can expand quickly without relying on expensive (and risky) acquisitions.

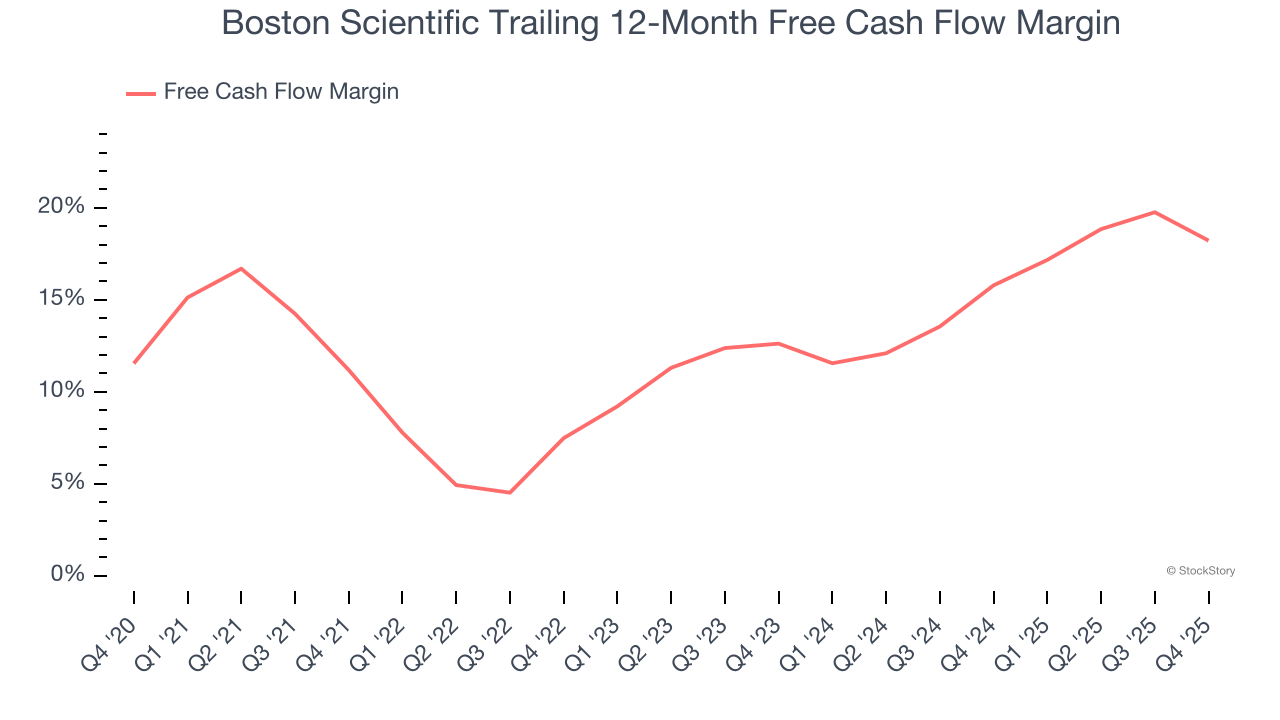

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, Boston Scientific’s margin expanded by 7 percentage points over the last five years. This is encouraging, and we can see it became a less capital-intensive business because its free cash flow profitability rose more than its operating profitability. Boston Scientific’s free cash flow margin for the trailing 12 months was 18.2%.

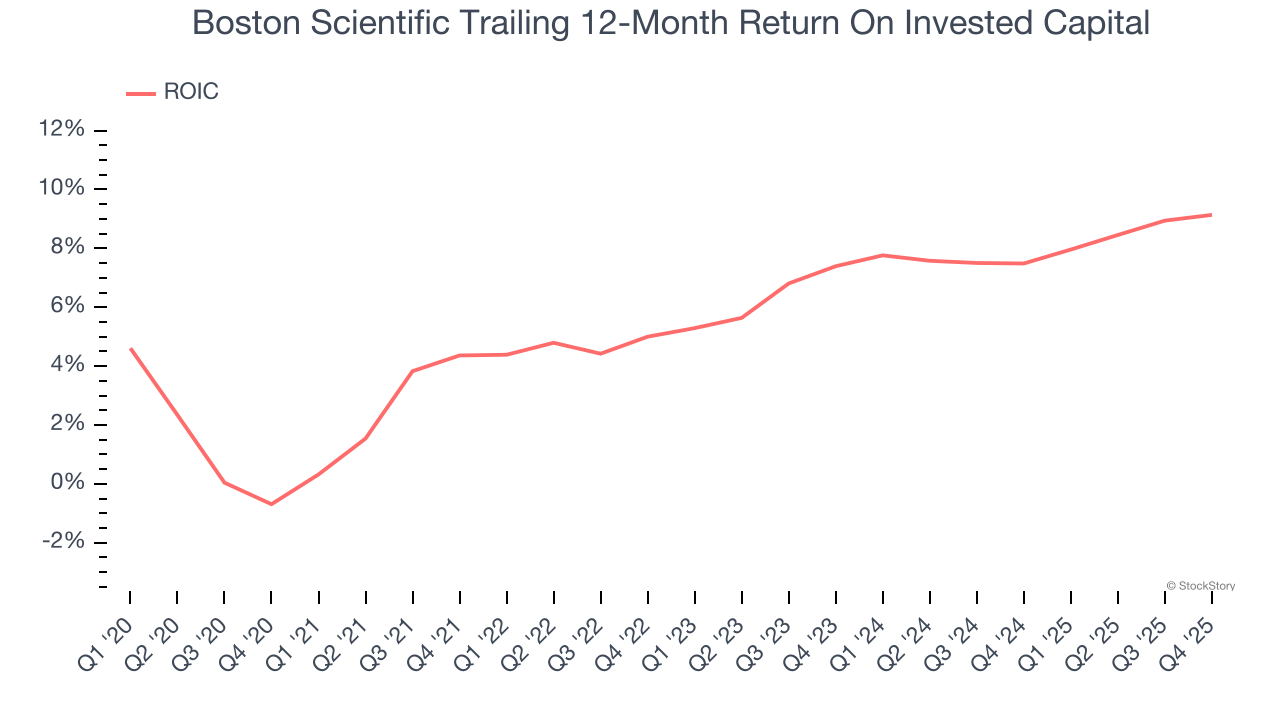

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Although Boston Scientific has shown solid fundamentals lately, it historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 6.7%, somewhat low compared to the best healthcare companies that consistently pump out 20%+.

Boston Scientific’s positive characteristics outweigh the negatives. After the recent drawdown, the stock trades at 22.2× forward P/E (or $76.39 per share). Is now the time to initiate a position? See for yourself in our full research report, it’s free.

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don't just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn't over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

| Jul-24 | |

| Jul-24 | |

| Jul-21 | |

| Jul-17 | |

| Jul-17 | |

| Jul-16 | |

| Jul-15 | |

| Jul-09 | |

| Jul-09 | |

| Jul-07 | |

| Jul-06 | |

| Jul-02 | |

| Jun-29 | |

| Jun-23 | |

| Jun-18 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite