|

|

|

|

|||||

|

|

|

Rapid7 has gotten torched over the last six months - since September 2025, its stock price has dropped 68.9% to $6.35 per share. This was partly driven by its softer quarterly results and might have investors contemplating their next move.

Is now the time to buy Rapid7, or should you be careful about including it in your portfolio? Get the full breakdown from our expert analysts, it’s free.

Even though the stock has become cheaper, we're cautious about Rapid7. Here are three reasons you should be careful with RPD and a stock we'd rather own.

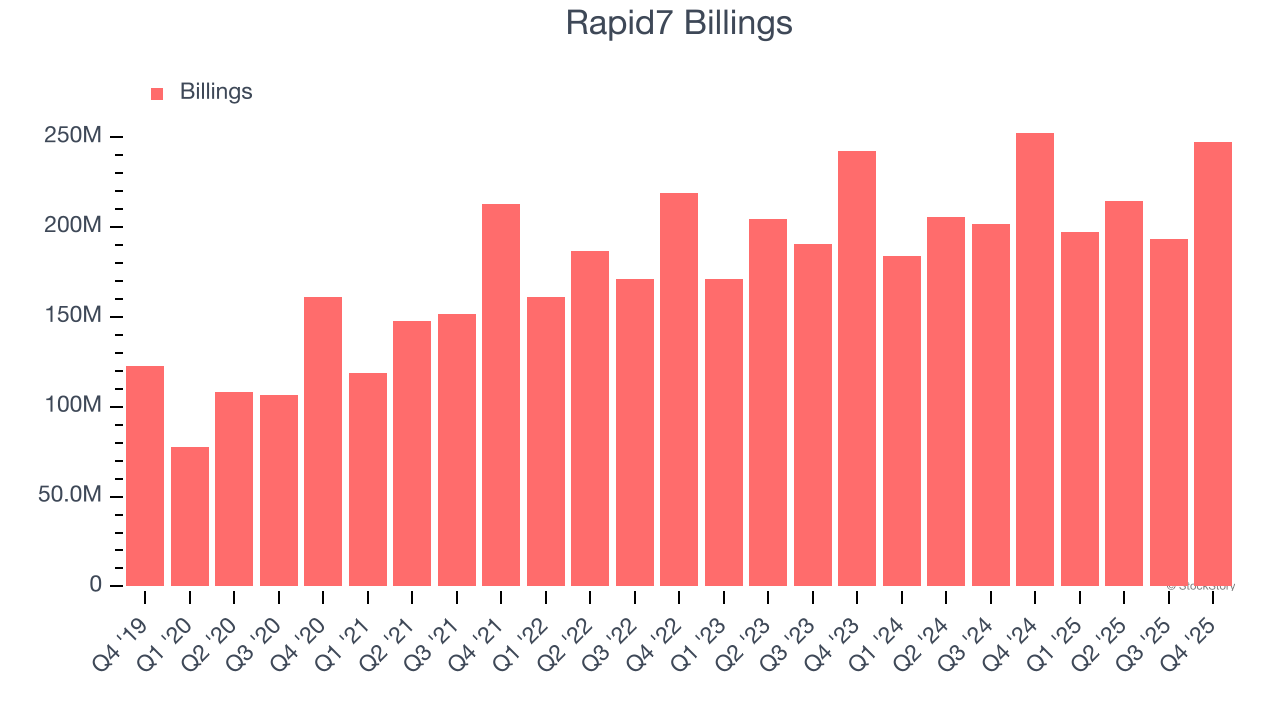

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Rapid7’s billings came in at $247.2 million in Q4, and over the last four quarters, its year-on-year growth averaged 1.3%. This performance was underwhelming and suggests that increasing competition is causing challenges in acquiring/retaining customers.

The customer acquisition cost (CAC) payback period represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for sales and marketing investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

Rapid7’s recent customer acquisition efforts haven’t yielded returns as its CAC payback period was negative this quarter, meaning its incremental sales and marketing investments outpaced its revenue. The company’s inefficiency indicates it operates in a highly competitive environment where there is little differentiation between Rapid7’s products and its peers.

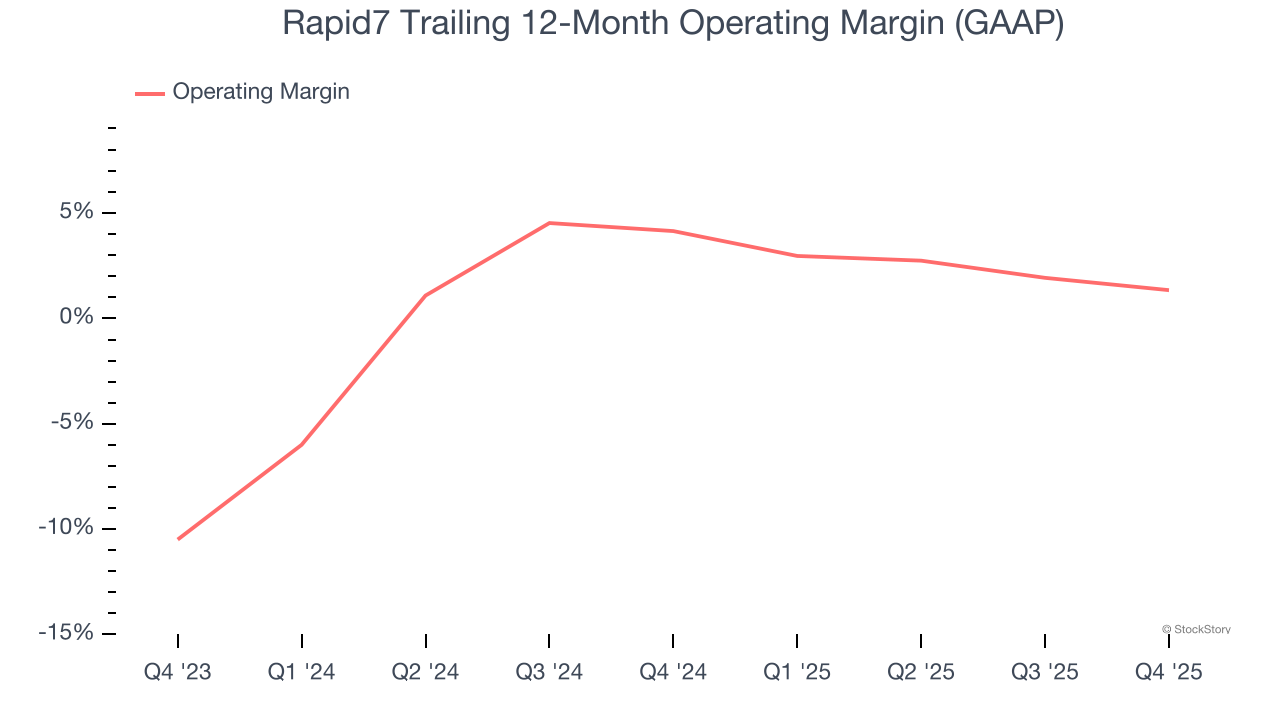

Many software businesses adjust their profits for stock-based compensation (SBC), but we prioritize GAAP operating margin because SBC is a real expense used to attract and retain engineering and sales talent. This metric shows how much revenue remains after accounting for all core expenses – everything from the cost of goods sold to sales and R&D.

Looking at the trend in its profitability, Rapid7’s operating margin decreased by 2.8 percentage points over the last two years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Its operating margin for the trailing 12 months was 1.3%.

Rapid7 doesn’t pass our quality test. After the recent drawdown, the stock trades at 0.5× forward price-to-sales (or $6.35 per share). While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are superior stocks to buy right now. We’d recommend looking at a fast-growing restaurant franchise with an A+ ranch dressing sauce.

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it's flagging for this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

| Jul-28 | |

| Jul-14 | |

| Jun-15 | |

| Jun-01 | |

| May-21 | |

| May-13 | |

| May-12 | |

| May-11 | |

| May-06 | |

| May-05 | |

| May-05 | |

| Apr-29 | |

| Apr-29 | |

| Apr-10 | |

| Apr-09 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite