|

|

|

|

|||||

|

|

|

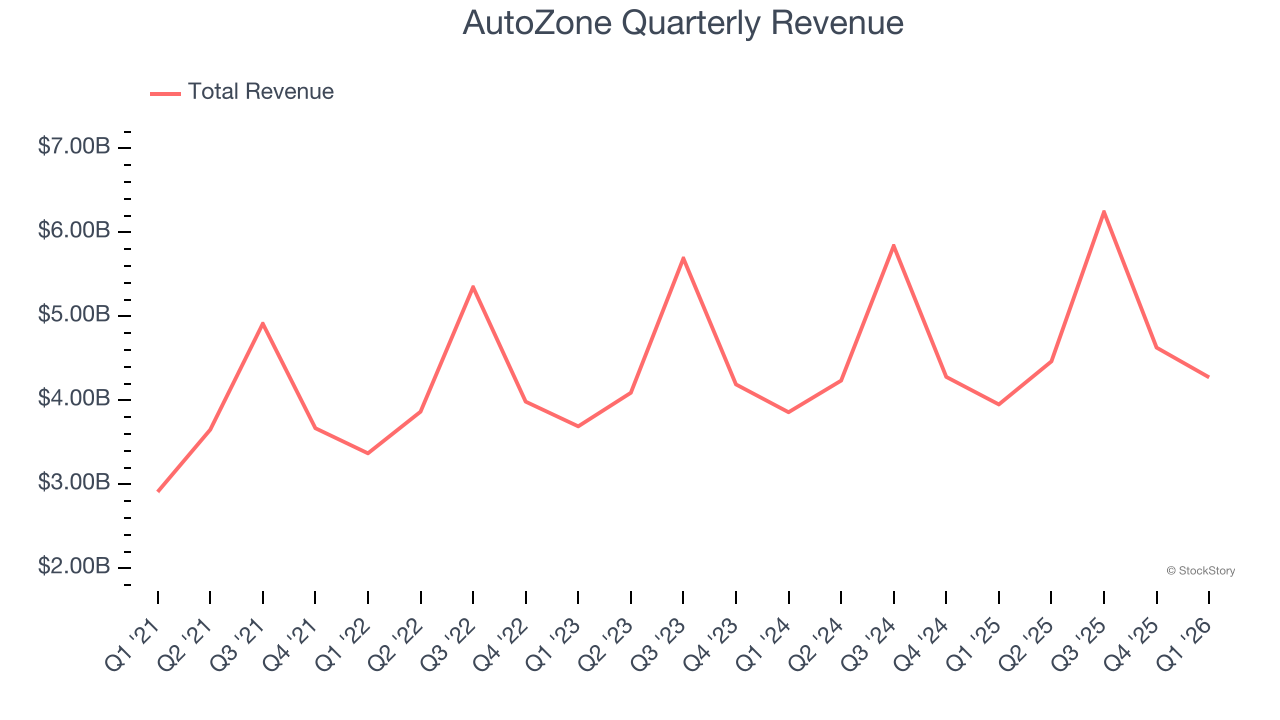

Auto parts and accessories retailer AutoZone (NYSE:AZO) fell short of the market’s revenue expectations in Q1 CY2026, but sales rose 8.1% year on year to $4.27 billion. Its GAAP profit of $27.63 per share was 1.2% above analysts’ consensus estimates.

Is now the time to buy AutoZone? Find out by accessing our full research report, it’s free.

“I want to thank our AutoZoners across the company for delivering solid financial results this past quarter. We continue to be pleased with our strategies to grow sales. Domestically, both DIY and Commercial sales continued to perform well this past quarter in spite of winter storms causing disruptions the last week of January and the first week of February. While our international sales, in constant currency, were slightly below our expectations, we believe our market share continues to grow as we outpace our competition in both Mexico and Brazil. We were also pleased to have opened 64 net new stores globally in the quarter, in line with our expectations to open approximately 350-360 stores for the full fiscal year. As we remain focused on gaining market share across our highly fragmented industry, we remain committed to a disciplined approach of increasing earnings and cash flows to drive shareholder value,” said Phil Daniele, President and Chief Executive Officer.

Aiming to be a one-stop shop for the DIY customer, AutoZone (NYSE:AZO) is an auto parts and accessories retailer that sells everything from car batteries to windshield wiper fluid to brake pads.

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $19.61 billion in revenue over the past 12 months, AutoZone is one of the larger companies in the consumer retail industry and benefits from a well-known brand that influences purchasing decisions. However, its scale is a double-edged sword because there is only so much real estate to build new stores, placing a ceiling on its growth. To expand meaningfully, AutoZone likely needs to tweak its prices or enter new markets.

As you can see below, AutoZone’s sales grew at a tepid 5.1% compounded annual growth rate over the last three years, but to its credit, it opened new stores and increased sales at existing, established locations.

This quarter, AutoZone’s revenue grew by 8.1% year on year to $4.27 billion, missing Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 8.1% over the next 12 months, an acceleration versus the last three years. This projection is particularly healthy for a company of its scale and implies its newer products will spur better top-line performance.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

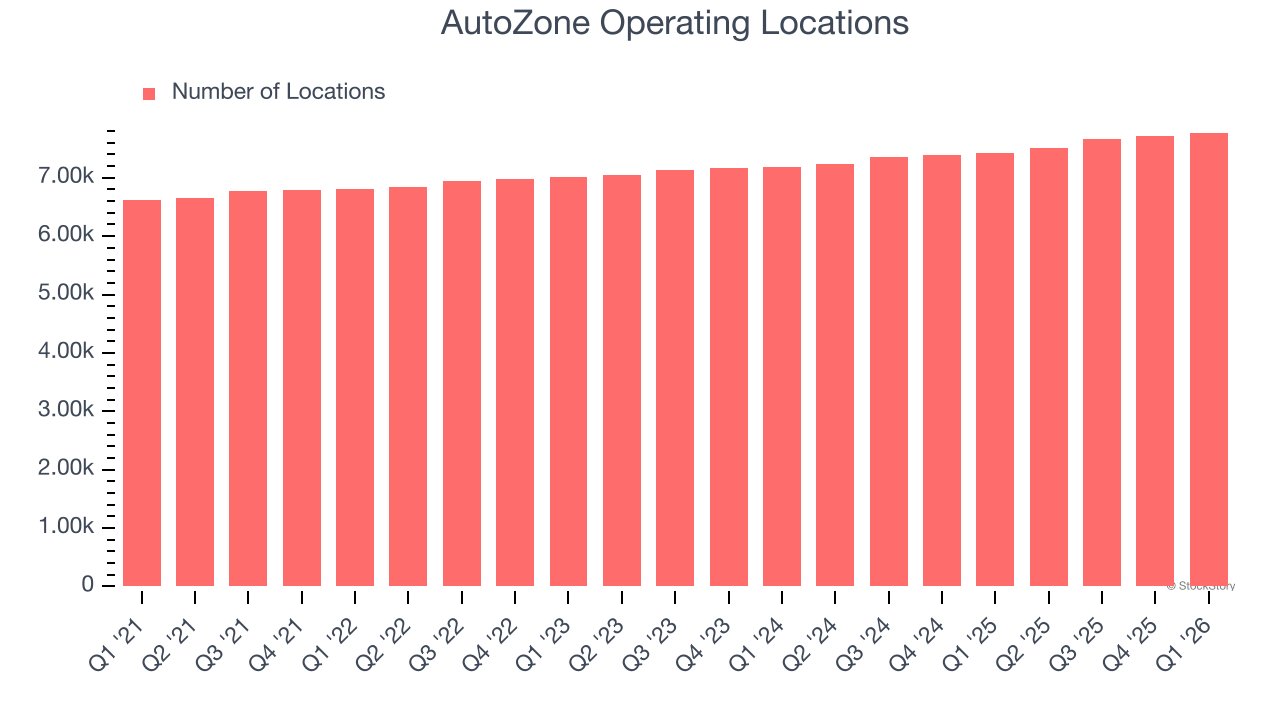

A retailer’s store count influences how much it can sell and how quickly revenue can grow.

AutoZone sported 7,774 locations in the latest quarter. Over the last two years, it has opened new stores quickly, averaging 3.6% annual growth. This was faster than the broader consumer retail sector.

When a retailer opens new stores, it usually means it’s investing for growth because demand is greater than supply, especially in areas where consumers may not have a store within reasonable driving distance.

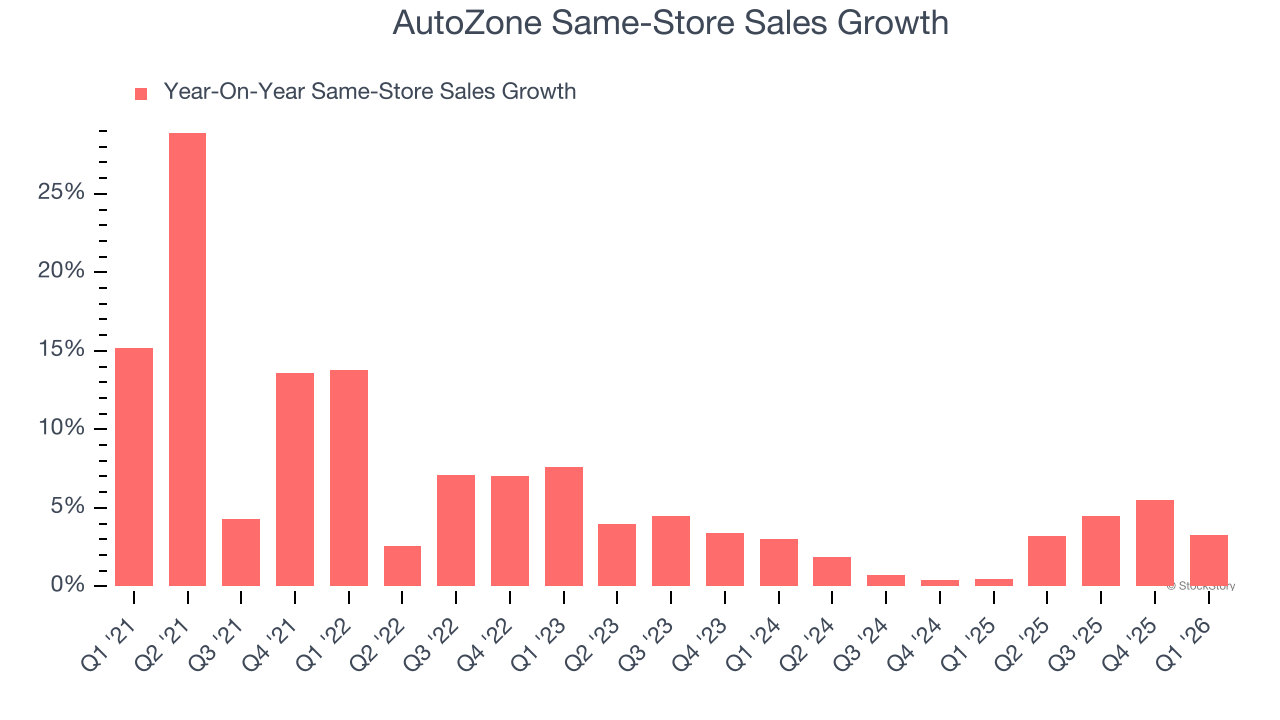

The change in a company's store base only tells one side of the story. The other is the performance of its existing locations and e-commerce sales, which informs management teams whether they should expand or downsize their physical footprints. Same-store sales gives us insight into this topic because it measures organic growth for a retailer's e-commerce platform and brick-and-mortar shops that have existed for at least a year.

AutoZone’s demand rose over the last two years and slightly outpaced the industry. On average, the company’s same-store sales have grown by 2.5% per year. This performance suggests its rollout of new stores could be beneficial for shareholders. When a retailer has demand, more locations should help it reach more customers and boost revenue growth.

In the latest quarter, AutoZone’s same-store sales rose 3.3% year on year. This performance was more or less in line with its historical levels.

It was good to see AutoZone narrowly top analysts’ EBITDA expectations this quarter. On the other hand, its revenue slightly missed. Overall, this quarter could have been better. The stock traded down 7.1% to $3,605 immediately following the results.

Big picture, is AutoZone a buy here and now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).

| Jul-22 | |

| Jul-10 | |

| Jul-06 | |

| Jun-16 | |

| Jun-04 | |

| Jun-03 | |

| May-29 | |

| May-28 | |

| May-26 | |

| May-26 | |

| May-26 | |

| May-26 | |

| May-26 | |

| May-26 | |

| May-26 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite