|

|

|

|

|||||

|

|

|

Over the past six months, Inspired’s stock price fell to $8.21. Shareholders have lost 9.3% of their capital, which is disappointing considering the S&P 500 has climbed by 6.6%. This may have investors wondering how to approach the situation.

Is now the time to buy Inspired, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Even though the stock has become cheaper, we're swiping left on Inspired for now. Here are three reasons we avoid INSE and a stock we'd rather own.

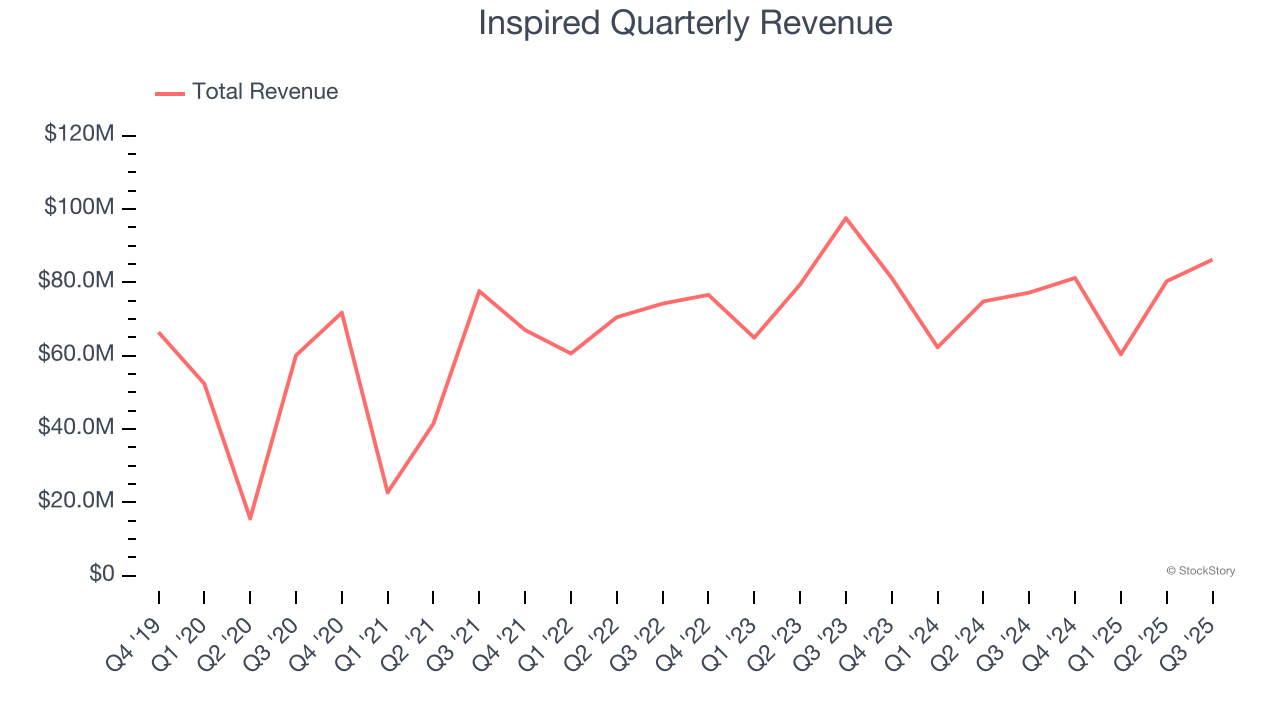

A company’s long-term sales performance is one signal of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, Inspired grew its sales at a weak 9.6% compounded annual growth rate. This was below our standard for the consumer discretionary sector.

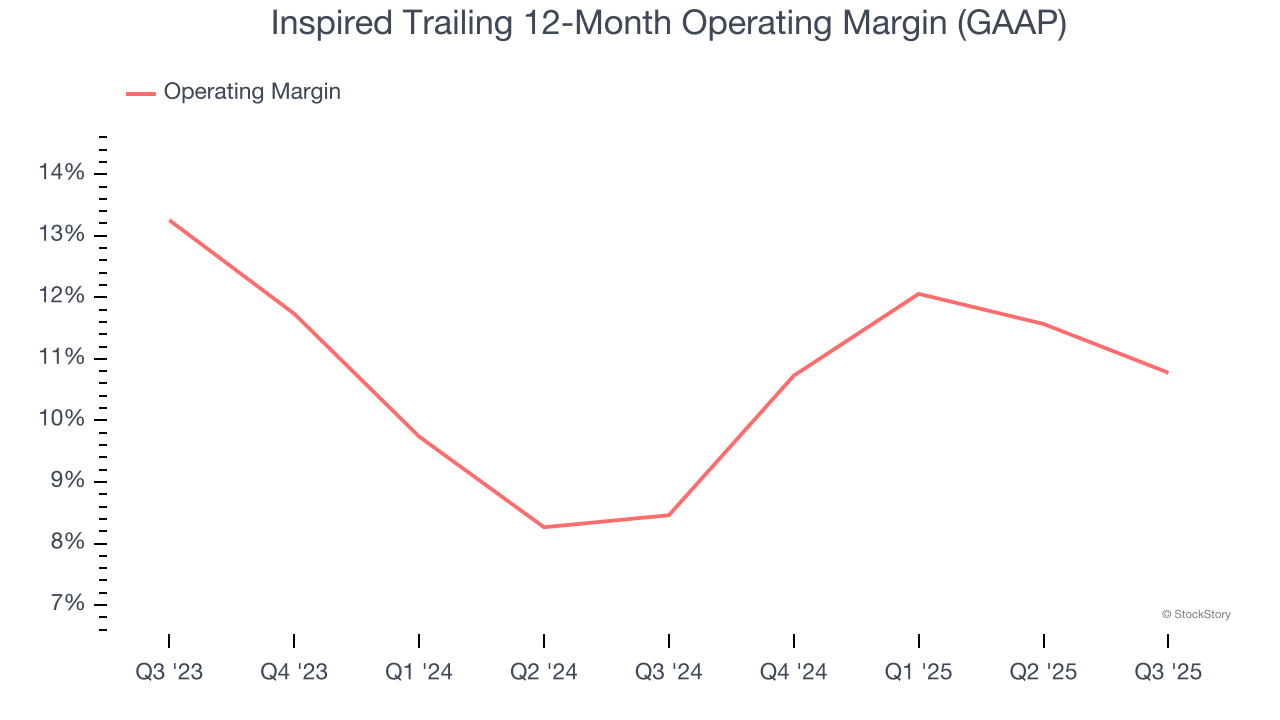

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Inspired’s operating margin has been trending up over the last 12 months and averaged 9.6% over the last two years. The company’s higher efficiency is a breath of fresh air, but its suboptimal cost structure means it still sports inadequate profitability for a consumer discretionary business.

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Over the next year, analysts predict Inspired’s cash conversion will slightly fall. Their consensus estimates imply its free cash flow margin of 5.7% for the last 12 months will decrease to 11%.

We see the value of companies helping consumers, but in the case of Inspired, we’re out. After the recent drawdown, the stock trades at 13.2× forward P/E (or $8.21 per share). This valuation is reasonable, but the company’s shaky fundamentals present too much downside risk. There are more exciting stocks to buy at the moment. We’d recommend looking at one of Charlie Munger’s all-time favorite businesses.

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it's flagging for this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

| Aug-06 | |

| Aug-05 | |

| Aug-05 | |

| Jul-30 | |

| Jul-21 | |

| Jul-13 | |

| Jun-22 | |

| May-19 | |

| May-18 | |

| May-07 | |

| May-07 | |

| May-07 | |

| May-06 | |

| Apr-24 | |

| Apr-22 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite