|

|

|

|

|||||

|

|

|

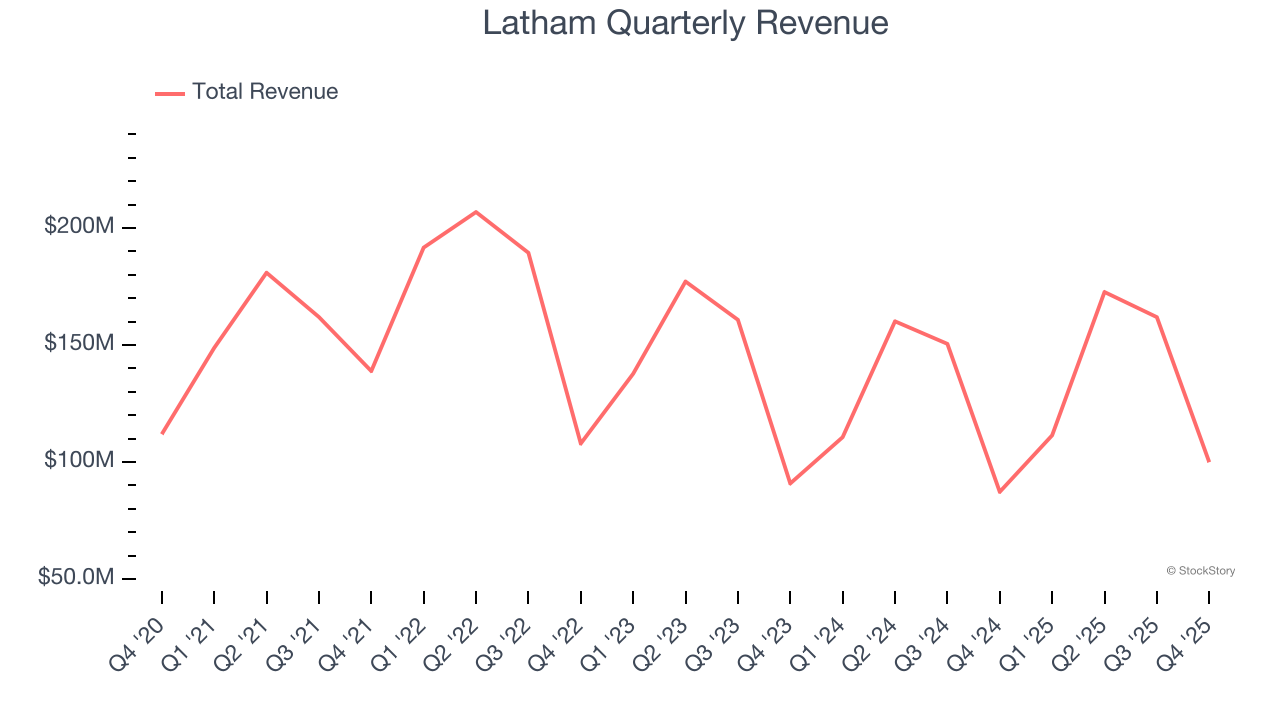

Residential swimming pool manufacturer Latham (NASDAQ:SWIM) reported Q4 CY2025 results topping the market’s revenue expectations, with sales up 14.5% year on year to $99.95 million. The company’s full-year revenue guidance of $595 million at the midpoint came in 4.2% above analysts’ estimates. Its GAAP loss of $0.06 per share was 45.2% above analysts’ consensus estimates.

Is now the time to buy Latham? Find out by accessing our full research report, it’s free.

“2025 marked another year of strong execution by the Latham team,” said Sean Gadd, President and CEO of Latham Group.

Started as a family business, Latham (NASDAQ:SWIM) is a global designer and manufacturer of in-ground residential swimming pools and related products.

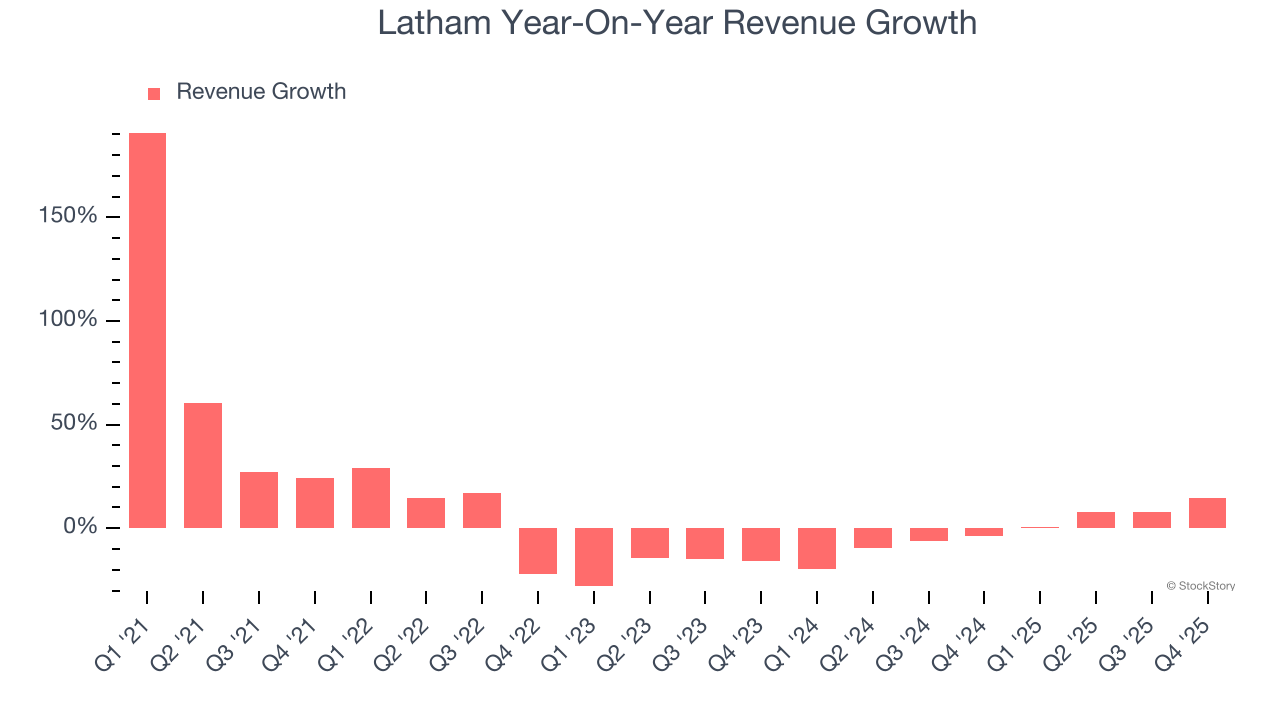

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Unfortunately, Latham’s 6.2% annualized revenue growth over the last five years was weak. This was below our standard for the consumer discretionary sector and is a rough starting point for our analysis.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Latham’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 1.8% annually.

This quarter, Latham reported year-on-year revenue growth of 14.5%, and its $99.95 million of revenue exceeded Wall Street’s estimates by 4.4%.

Looking ahead, sell-side analysts expect revenue to grow 4.8% over the next 12 months. Although this projection implies its newer products and services will catalyze better top-line performance, it is still below average for the sector.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

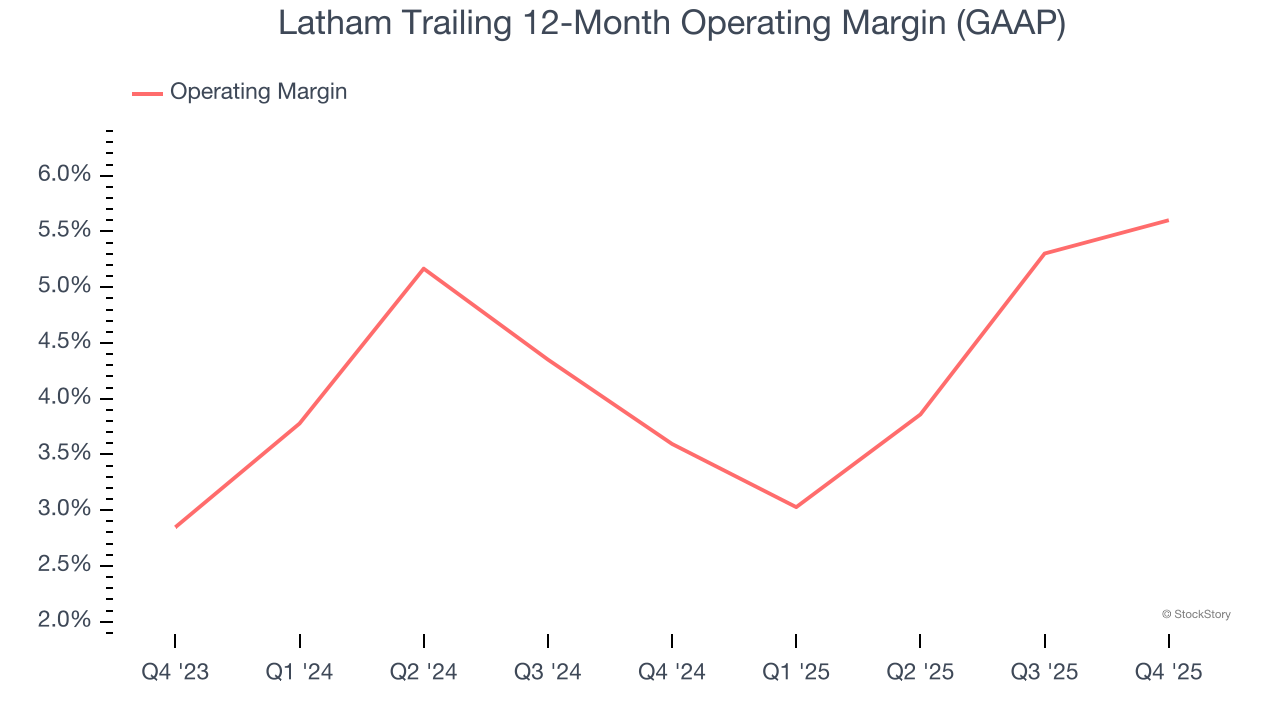

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Latham’s operating margin has been trending up over the last 12 months and averaged 4.6% over the last two years. The company’s higher efficiency is a breath of fresh air, but its suboptimal cost structure means it still sports inadequate profitability for a consumer discretionary business.

This quarter, Latham generated an operating margin profit margin of negative 10.7%, up 4.2 percentage points year on year. This increase was a welcome development and shows it was more efficient.

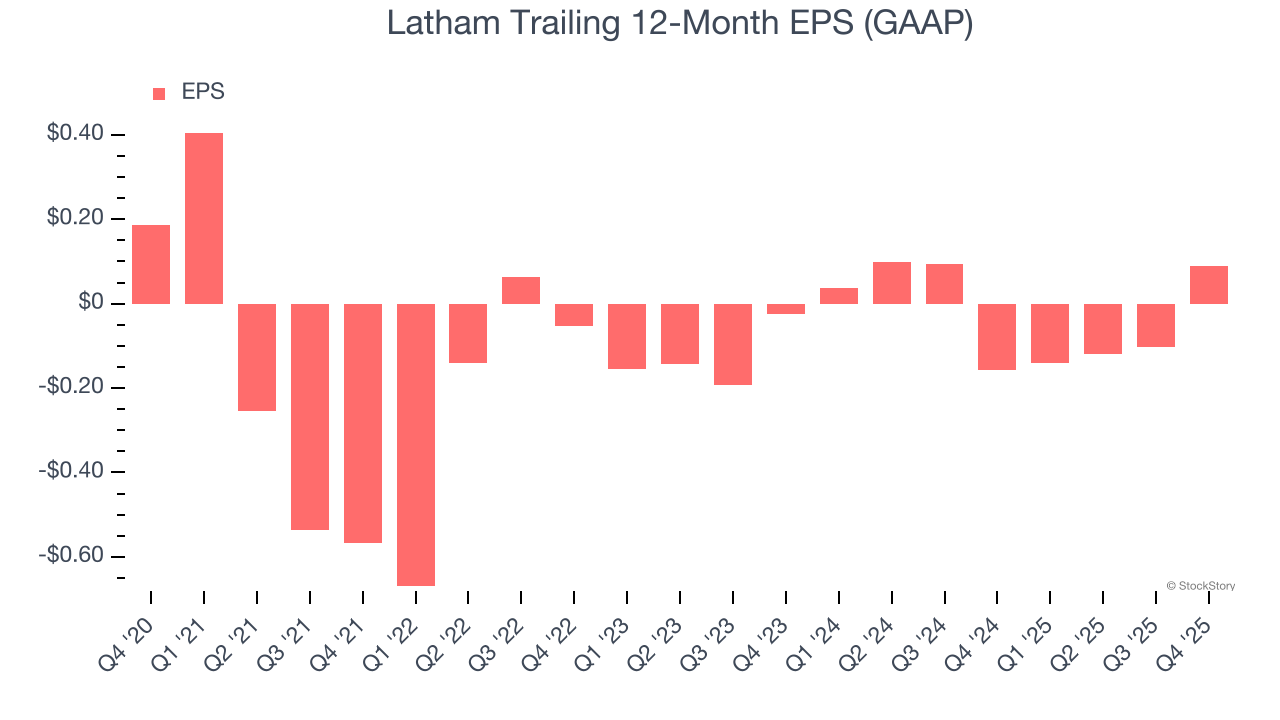

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Latham, its EPS declined by 13.6% annually over the last five years while its revenue grew by 6.2%. This tells us the company became less profitable on a per-share basis as it expanded.

In Q4, Latham reported EPS of negative $0.06, up from negative $0.25 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Latham’s full-year EPS of $0.09 to grow 26.5%.

It was good to see Latham beat analysts’ EPS expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a solid print. The stock traded up 14.9% to $7.41 immediately following the results.

Latham put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).

| Aug-03 | |

| Jul-08 | |

| May-25 | |

| May-18 | |

| May-05 | |

| May-05 | |

| May-05 | |

| May-01 | |

| Apr-30 | |

| Apr-09 | |

| Mar-10 | |

| Mar-04 | |

| Mar-04 | |

| Mar-04 | |

| Mar-03 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite