|

|

|

|

|||||

|

|

|

Fabrinet FN shares have jumped 24.9% in a month, driven by an accelerating Telecom and Datacenter Interconnect (DCI) revenues, easing datacom constraints and continued scaling in High-Performance Computing (HPC) business embedded in management’s fiscal third-quarter outlook.

The HPC program is scaling with added automation and credible execution, with optionality to gain share as a qualified second source. Fabrinet cites strong visibility, with sequential growth expected and catalysts ahead as DCI accelerates, next-gen 800ZR nears production and datacom constraints ease with second-source approvals.

In the second quarter of fiscal 2026, HPC contributed $85.6 million, and management expects the current program to exceed $150 million per quarter within the next couple of quarters, with double-digit sequential growth guided for the third quarter of fiscal 2026.

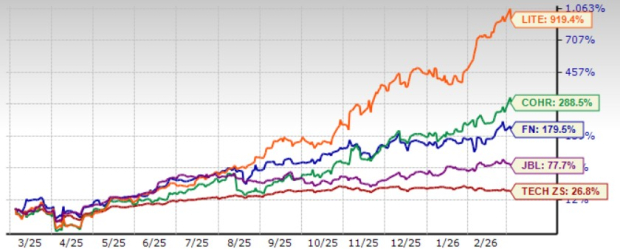

However, Fabrinet is facing stiff competition from the likes of Lumentum LITE, Coherent COHR and Jabil JBL. In the trailing 12-month period, Fabrinet shares have jumped 179.5%, underperforming Lumentum’s and Coherent’s 919.4% and 288.5% increases, respectively. However, FN shares outperformed Jabil’s return of 77.7%.

Fabrinet’s record second-quarter fiscal 2026 revenues and earnings exceeded guidance on execution and leverage. FN delivered strong second-quarter fiscal 2026 non-GAAP earnings of $3.36 per share that beat the Zacks Consensus Estimate by 3.07%. Revenues of $1.13 billion surpassed the consensus mark by 5.03%. The figure jumped 36% year over year and 16% sequentially.

Third-quarter fiscal 2026 guidance indicates continued top-line growth (35% year-over-year growth at mid-point of $1.15-$1.2 billion range) with non-GAAP earnings between $3.45 per share and $3.60 per share (indicating 40% year-over-year growth at mid-point) despite headwind from forex. Fabrinet plans to offset most of the currency pressure through operating leverage and disciplined operating expenses, building on multi-quarter margin expansion.

Fabrinet’s pipeline adds multi-year optionality. In datacom, programs to build transceivers for hyperscalers directly and for merchant vendors are described as quarters away, not years, from meaningful revenues. In telecom/DCI, next-gen 800ZR has not yet ramped, preserving an additional catalyst as products move to production. Engagements in co-packaged optics with three customers and in optical circuit switching further extend the opportunity set, with timing explicitly tied to customer roadmaps. Coupled with a pure-play EMS model that avoids margin stacking and does not compete with customers' products, these developments should translate into new high-value programs that layer on top of fiscal 2026’s growth drivers.

FN ended the fiscal second quarter with about $961.5 million in cash and short-term investments and no debt, supporting expansion plans and financial flexibility.

The company also had $169 million remaining under its share repurchase authorization, providing an additional lever during periods of quarterly volatility.

Fabrinet’s strong prospects, along with a debt-free balance sheet, justify a premium valuation, as suggested by the Value Score of F.

In terms of forward 12-month price/earnings (P/E), this Zacks Rank #2 (Buy) company is currently trading at 36.06X higher than the broader sector’s 24.58X and Jabil’s 20.32X. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

However, Fabrinet’s P/E multiple is lower than Coherent’s 42.55X.

The Zacks Consensus Estimate for the third quarter of fiscal 2026 earnings is currently pegged at $3.58 per share, up 3.5% over the past 30 days, and indicates 42.1% growth from the figure reported in the year-ago quarter.

Fabrinet price-consensus-chart | Fabrinet Quote

The consensus mark for fiscal 2026 earnings is currently pegged at $13.58 per share, up 2.2% over the past 30 days, suggesting 33.5% growth from fiscal 2025’s reported figure.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-23 | |

| Jul-23 | |

| Jul-22 | |

| Jul-22 | |

| Jul-21 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-16 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite