|

|

|

|

|||||

|

|

|

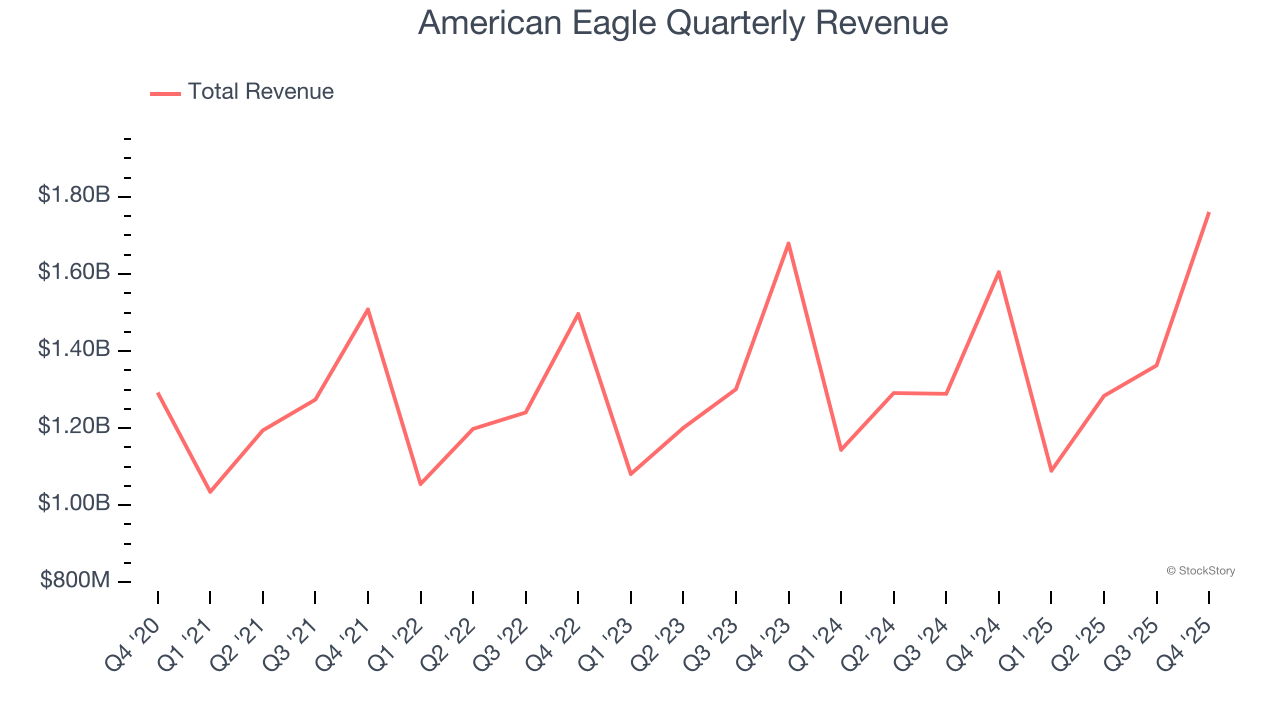

Young adult apparel retailer American Eagle Outfitters (NYSE:AEO) announced better-than-expected revenue in Q4 CY2025, with sales up 9.7% year on year to $1.76 billion. Its non-GAAP profit of $0.84 per share was 17.8% above analysts’ consensus estimates.

Is now the time to buy American Eagle? Find out by accessing our full research report, it’s free.

Jay Schottenstein, Executive Chairman of the Board and Chief Executive Officer, AEO Inc., commented, “I am extremely pleased with the strong execution in the back half of the year, which reignited growth across our brands and channels. Building on the improved trends beginning last summer, we achieved a record fourth quarter and holiday period, with double digit growth at Aerie and OFFLINE and solid, positive performance at American Eagle. Compelling new product collections, supported by fresh marketing campaigns, led to higher demand trends in the quarter. I want to thank our associates for their resilience and outstanding execution to deliver a strong finish to 2025.”

With a heavy focus on denim, American Eagle Outfitters (NYSE:AEO) is a specialty retailer offering an assortment of apparel and accessories to young adults.

A company’s long-term performance is an indicator of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years.

With $5.50 billion in revenue over the past 12 months, American Eagle is a mid-sized retailer, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale.

As you can see below, American Eagle’s 3.3% annualized revenue growth over the last three years was sluggish as its store footprint remained unchanged.

This quarter, American Eagle reported year-on-year revenue growth of 9.7%, and its $1.76 billion of revenue exceeded Wall Street’s estimates by 1.2%.

Looking ahead, sell-side analysts expect revenue to grow 3.2% over the next 12 months, similar to its three-year rate. This projection is above the sector average and implies its newer products will help sustain its historical top-line performance.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

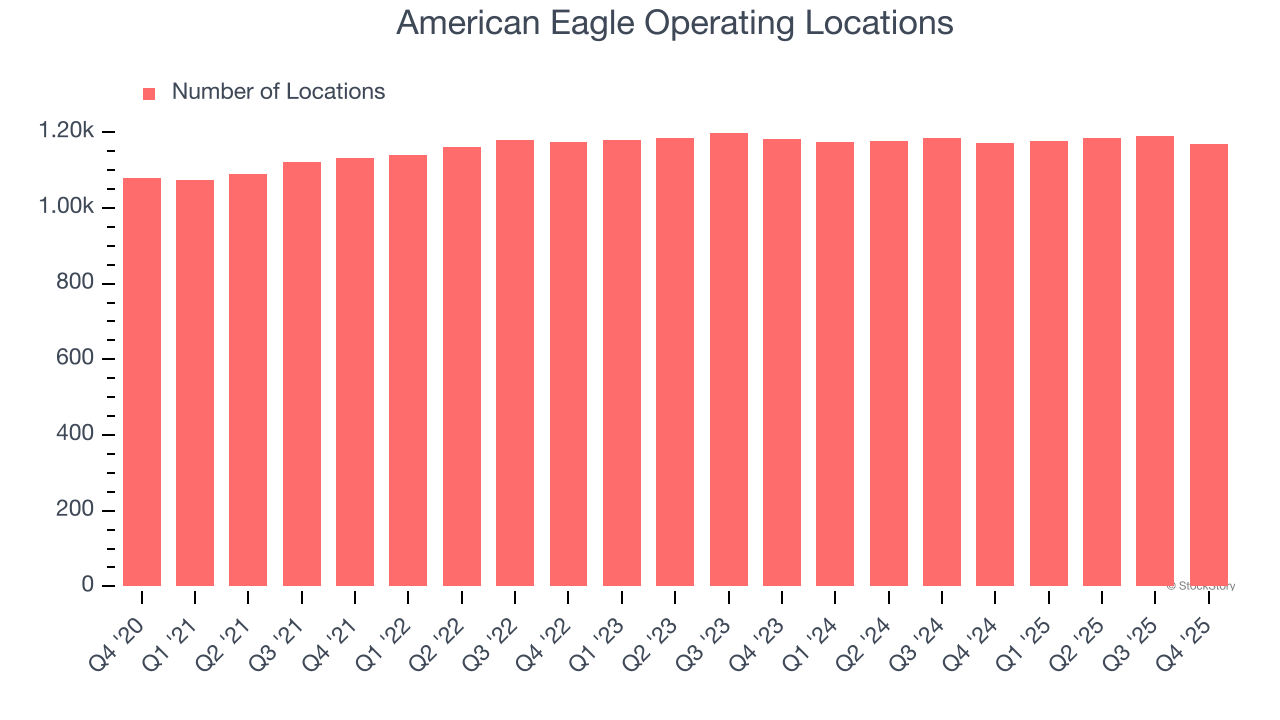

A retailer’s store count often determines how much revenue it can generate.

American Eagle listed 1,168 locations in the latest quarter and has kept its store count flat over the last two years while other consumer retail businesses have opted for growth.

When a retailer keeps its store footprint steady, it usually means demand is stable and it’s focusing on operational efficiency to increase profitability.

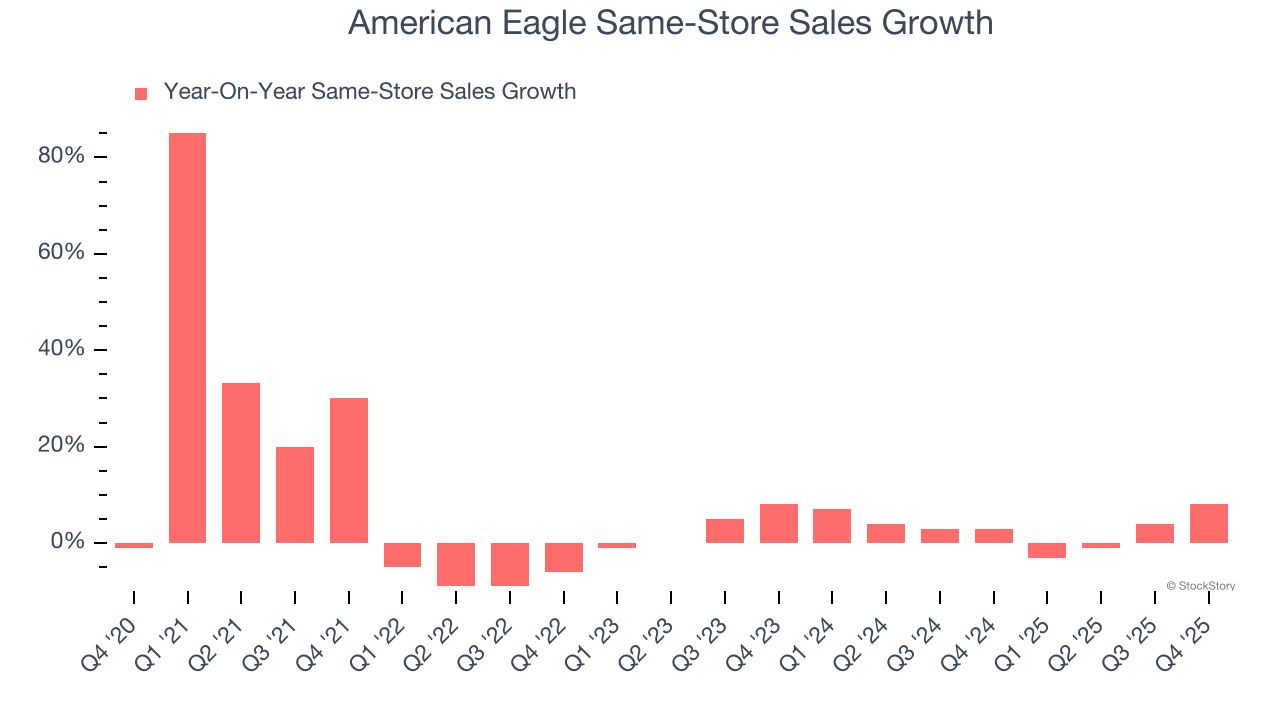

The change in a company's store base only tells one side of the story. The other is the performance of its existing locations and e-commerce sales, which informs management teams whether they should expand or downsize their physical footprints. Same-store sales gives us insight into this topic because it measures organic growth for a retailer's e-commerce platform and brick-and-mortar shops that have existed for at least a year.

American Eagle’s demand has been healthy for a retailer over the last two years. On average, the company has grown its same-store sales by a robust 3.1% per year. Given its flat store base over the same period, this performance stems from not only increased foot traffic at existing locations but also higher e-commerce sales as demand shifts from in-store to online.

In the latest quarter, American Eagle’s same-store sales rose 8% year on year. This growth was an acceleration from its historical levels, which is always an encouraging sign.

It was good to see American Eagle beat analysts’ EPS expectations this quarter. We were also happy its revenue narrowly outperformed Wall Street’s estimates. On the other hand, its EBITDA missed. Overall, this quarter could have been better. The stock remained flat at $22.78 immediately after reporting.

Is American Eagle an attractive investment opportunity at the current price? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).

| Jul-29 | |

| Jul-28 | |

| Jul-27 | |

| Jul-13 | |

| Jul-02 | |

| Jul-02 | |

| Jul-02 | |

| Jul-01 | |

| Jun-26 | |

| Jun-22 | |

| Jun-09 | |

| Jun-09 | |

| Jun-08 | |

| Jun-05 | |

| Jun-04 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite