|

|

|

|

|||||

|

|

|

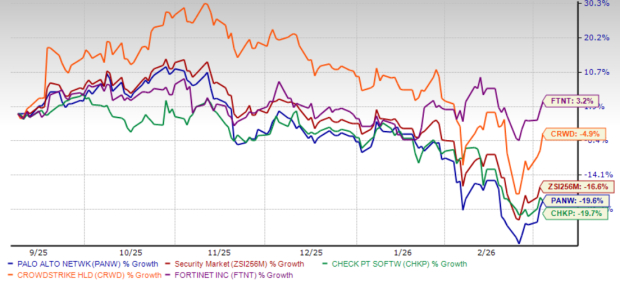

Palo Alto Networks PANW shares have lost 19.6% over the past six months, underperforming the Zacks Security industry’s decline of 16.6%. The stock has also underperformed industry peers such as Fortinet FTNT and CrowdStrike CRWD, while marginally outperforming Check Point Software CHKP. Over the past six months, shares of Fortinet have jumped 3.2%, while CrowdStrike and Check Point Software shares have lost 4.9% and 19.7%, respectively.

The underperformance of Palo Alto Networks’ shares raises the question: Should investors buy, sell or hold PANW stock?

Palo Alto Networks' near-term prospects are expected to be weighed down due to integration and acquisition-related costs. PANW recently completed two major acquisitions, which include its $25 billion CyberArk deal and $3.35 billion Chronosphere acquisition. As a result, PANW is incurring high integration-related costs, including onboarding employees, aligning go-to-market teams, and integrating systems and operations. Acquisition-related costs in the second quarter of fiscal 2026 amounted to $24 million, a whopping increase from $5 million incurred in the prior quarter. These costs are expected to hurt the company's profitability before the benefits of synergies from acquisitions are fully realized.

Equity dilution effect is expected to significantly hurt PANW’s bottom line. In the second quarter of fiscal 2026, PANW issued 112 million shares as part of the CyberArk deal. This is expected to result in a significant equity dilution effect, hurting the company’s bottom-line results. Management expects fiscal 2026 earnings per share (EPS) to be in the range of $3.65-$3.70, down from its prior guidance of $3.80-$3.90 per share.

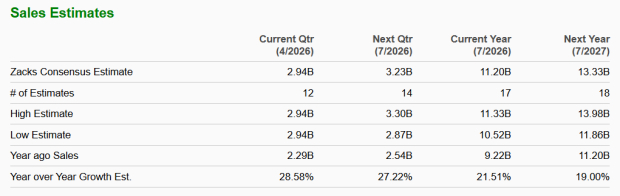

The Zacks Consensus Estimate for Palo Alto Networks’ fiscal 2026 and 2027 earnings is pegged at $3.73 and $4.07 per share, respectively. Estimates for fiscal 2026 and 2027 have both been revised downward by 11 cents and 25 cents, respectively, over the past 30 days.

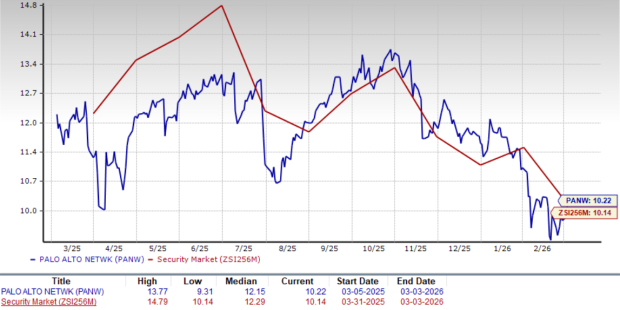

Palo Alto Networks is currently trading at a higher price-to-sales (P/S) multiple compared to the industry. PANW’s forward 12-month P/S ratio sits at 10.22X, slightly higher than the industry’s forward 12-month P/S ratio of 10.14X. The Zacks Value Score of F also suggests that PANW stock is overvalued.

Palo Alto Networks stock trades at a higher P/S multiple compared with Check Point Software and Fortinet, while trading at a lower P/S multiple compared with CrowdStrike. At present, CrowdStrike, Check Point Software and Fortinet have P/S multiples of 16.58X, 6.01X and 7.79X, respectively.

However, for investors, not everything is gloom and doom.

Palo Alto Networks is well-positioned to capitalize on the growing demand for advanced cybersecurity solutions. According to Fortune Business Insights, the global cybersecurity market is projected to expand from $248.28 billion in 2026 to $699.39 billion by 2034, representing a massive addressable market. As cyber threats become more sophisticated, enterprises are increasingly prioritizing multi-layered security platforms, which directly contribute to PANW’s strengths.

Palo Alto Networks’ wide range of innovative products, strong customer base and growing opportunities in areas like Zero Trust, Secure Access Service Edge (SASE) and private 5G security continue to support its long-term growth potential. For example, in the second quarter of fiscal 2026, SASE was Palo Alto Networks’ fastest-growing segment, with SASE Annual recurring revenues (ARR) increasing 40% year over year. Growth is mainly coming from customers who want to reduce the number of security tools they use.

Many organizations are moving away from older SASE products that do not provide a full view of their networks, cloud workloads and remote users. A notable example during the second quarter includes a global automotive leader selecting PANW for a major security transformation. The deal was worth more than $50 million, including about $30 million for SASE and $20 million for XSIAM to run the company’s global security operations center.

Similarly, a global technology supplier chose PANW for a transformation initiative worth more than $40 million, selecting XSIAM to modernize security operations globally while expanding its investment in SASE. PANW has sold more than 9 million secure browser licenses during the second quarter and added over 1,500 customers. Around 10% of these customers are from the Global 2000, indicating strong adoption among large enterprises.

The above-mentioned factors should continue to support PANW’s long-term growth as demand for cybersecurity solutions across enterprises continues to rise. The Zacks Consensus Estimate for fiscal 2026 and 2027 indicates revenue growth of around 21.5% and 19%, respectively.

Palo Alto Networks remains a leader in cybersecurity, with a strong long-term growth trajectory, continued AI-driven innovation and a shift toward a more predictable recurring revenue model. Growth in areas such as SASE, XSIAM and platform-based security offerings remains strong, supported by large enterprise deals and increasing customer adoption, which provides a favorable long-term growth opportunity for the company.

Palo Alto Networks faces near-term risks from rising integration costs due to large acquisitions, share dilution is meaningful, and downward revision of EPS guidance for fiscal 2026. These could hurt PANW’s prospects in the near term.

Currently, Palo Alto Networks carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| 3 hours | |

| 8 hours | |

| 9 hours | |

| 9 hours | |

| 11 hours | |

| 12 hours | |

| Jul-25 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-23 | |

| Jul-23 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite