|

|

|

|

|||||

|

|

|

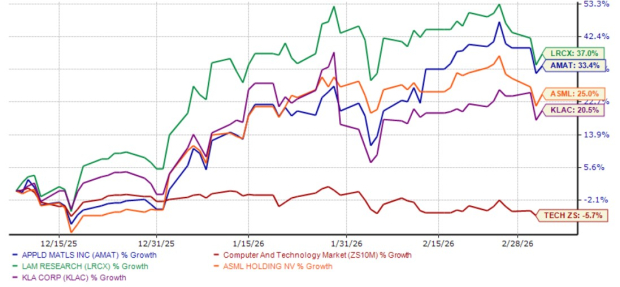

Applied Materials AMAT shares have risen 33.4% in the past three months, outperforming the Zacks Computer and Technology sector’s decline of 5.7%. AMAT stock outperformed its peers, ASML Holding ASML and KLA Corporation KLAC, while underperforming Lam Research LRCX.

ASML Holding, KLA Corporation and Lam Research shares have appreciated 25%, 20.5% and 37%, respectively, in the past three months. Given the rise of AMAT stock in the past three months and its dynamics with the other wafer fabrication equipment (WFE) players, investors are wondering: Is it the right time to buy, sell or hold AMAT stock?

The wafer fabrication equipment supply chain has multiple fabrication steps, and AMAT has the broadest and most diversified offerings as it provides solutions across multiple fabrication steps, like deposition, materials engineering, etch, metrology and packaging. While its competitors serve only one or two verticals.

For instance, Applied Materials and KLA Corporation offer similar solutions like Wafer Inspection, Yield Enhancement and Process Control inspection systems. Lam Research develops Atomic Layer Deposition tools like AT200M, AT410 and AT650P that are similar to the devices made by AMAT.

Both ASML and AMAT specialize in advanced semiconductor nodes, although they develop solutions for various stages of semiconductor production. ASML Holdings develops lithography solutions, including EXE and NXE systems. AMAT’s etching products include Sym3 Magnum Etch, Centura Xtera and Centura Etch.

Products like Producer GT and Producer SE for CVD deposition, Olympia ALD for atomic layer deposition and Endura PVD for physical vapor deposition compete with Lam Research, and platforms like PROVision eBeam Inspection systems, SEMVision e-beam metrology systems, ExtractAI metrology platform compare with KLAC’s metrology and inspection tools.

AMAT’s broad product portfolio enables it to seamlessly integrate its equipment across multiple processes. This reduces reliance on any single technology cycle and prices its product stack better to protect margins. The Zacks Consensus Estimate for AMAT’s fiscal 2026 earnings implies growth of 16.5%. The estimates have been revised upward in the past 30 days.

Applied Materials expects its leading-edge foundry, logic, DRAM and high-bandwidth memory (HBM) to be the fastest-growing wafer fabrication equipment businesses in 2026. In Logic, AMAT’s revenues are driven by the shift from FinFET to Gate-All-Around (GAA) transistors and backside power delivery.

The company specializes in GAA transistors at 2nm and below, HBM stacking and hybrid bonding and 3D device metrology, which are indispensable for manufacturing next-generation semiconductor chips. Recent launches like Xtera epi, Kinex hybrid bonding, and PROVision 10 eBeam will add to AMAT’s growth story throughout 2026 and beyond.

AMAT’s DRAM offerings are gaining traction as customers are aggressively investing in 6F² nodes supported by rising demand for high bandwidth memory DRAM, driven by AI workloads. On its first-quarter 2026 earnings call, AMAT highlighted its record growth in both Logic and DRAM segments, driven by major semiconductor transitions.

Applied Materials’ HBM chips are increasing in complexity and size, with three to four times more wafer starts per bit than standard DRAM, making it highly equipment-intensive. This is good for AMAT as the market for HBM expands. The company is determined to reach $3 billion in the next few years.

AMAT expects future generations of HBM to adopt hybrid bonding, and in the hybrid bonding space, AMAT is one of the leading innovators. AMAT’s advanced packaging, particularly 3D chiplet stacking, is another structural tailwind as AI chips become more heterogeneous. AMAT’s new product launches and growth in cold field emission e-beam technology further strengthen its competitive position.

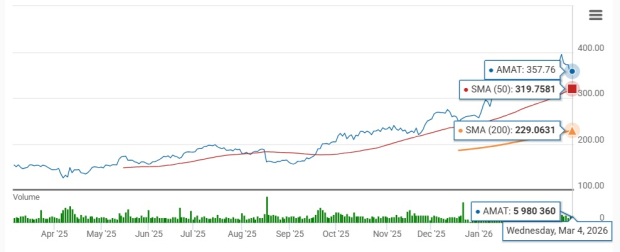

AMAT’s shares are trading above the 200-day and 50-day moving averages, indicating a bullish trend.

Applied Materials, with its broad portfolio of WFE products across deposition, materials engineering, etch, metrology, and packaging and traction across products like foundry, logic, DRAM and high-bandwidth memory, is a strong player in the semiconductor supply chain with strong opportunities. Given these conditions, we suggest that investors should buy this Zacks Rank #2 (Buy) stock at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 3 hours | |

| 3 hours | |

| 5 hours | |

| 10 hours | |

| 10 hours | |

| 12 hours | |

| 12 hours | |

| Aug-09 | |

| Aug-09 | |

| Aug-09 | |

| Aug-08 | |

| Aug-08 | |

| Aug-08 | |

| Aug-07 | |

| Aug-07 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite