|

|

|

|

|||||

|

|

|

Since September 2025, Compass has been in a holding pattern, posting a small loss of 1.6% while floating around $9.40. The stock also fell short of the S&P 500’s 5.6% gain during that period.

Is there a buying opportunity in Compass, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

We're sitting this one out for now. Here are three reasons you should be careful with COMP and a stock we'd rather own.

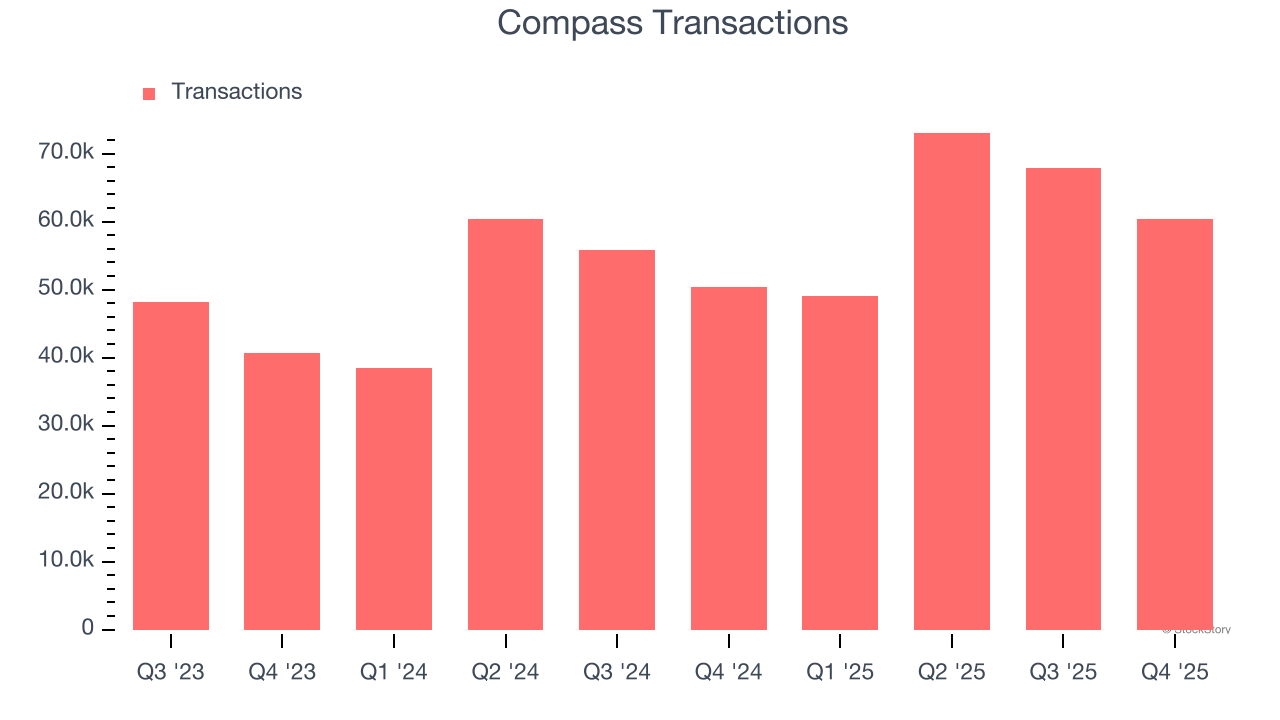

Revenue growth can be broken down into changes in price and volume (for companies like Compass, our preferred volume metric is transactions). While both are important, the latter is the most critical to analyze because prices have a ceiling.

Compass’s transactions came in at 60,328 in the latest quarter, and over the last two years, averaged 21.7% year-on-year growth. This performance was underwhelming and suggests it might have to lower prices or invest in product improvements to accelerate growth, factors that can hinder near-term profitability.

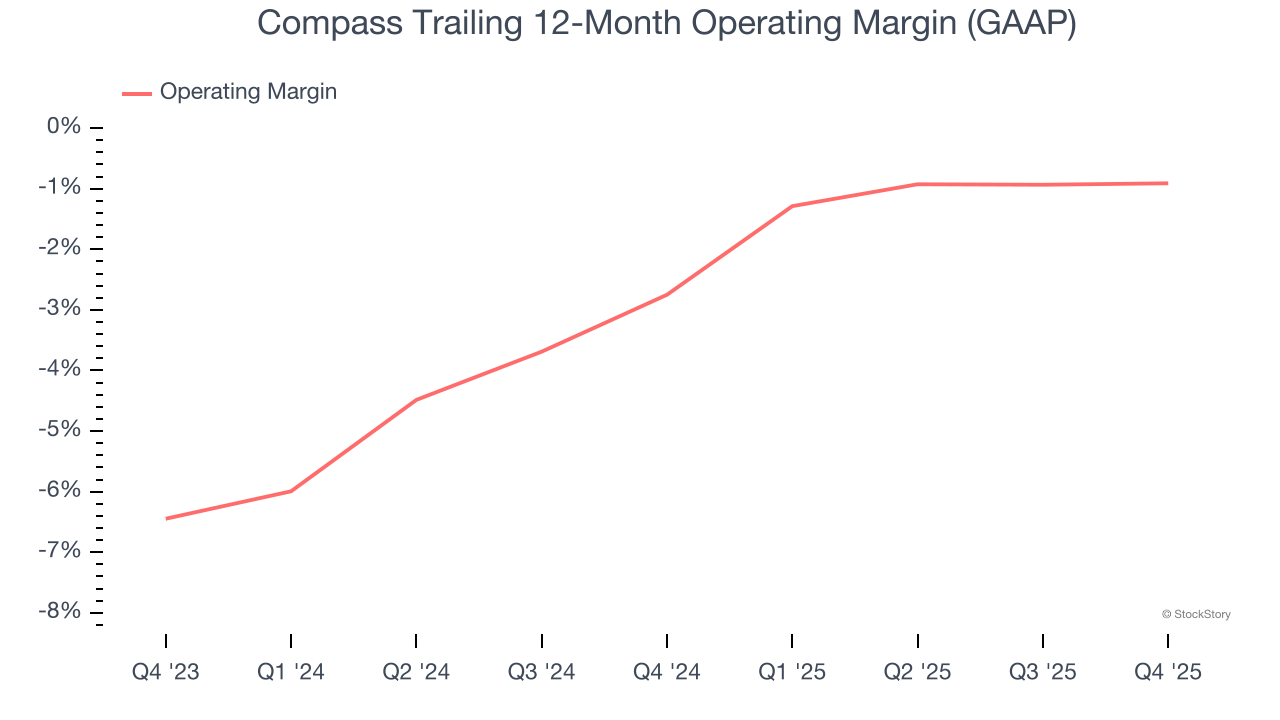

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Compass’s operating margin has been trending up over the last 12 months, but it still averaged negative 1.7% over the last two years. This is due to its large expense base and inefficient cost structure.

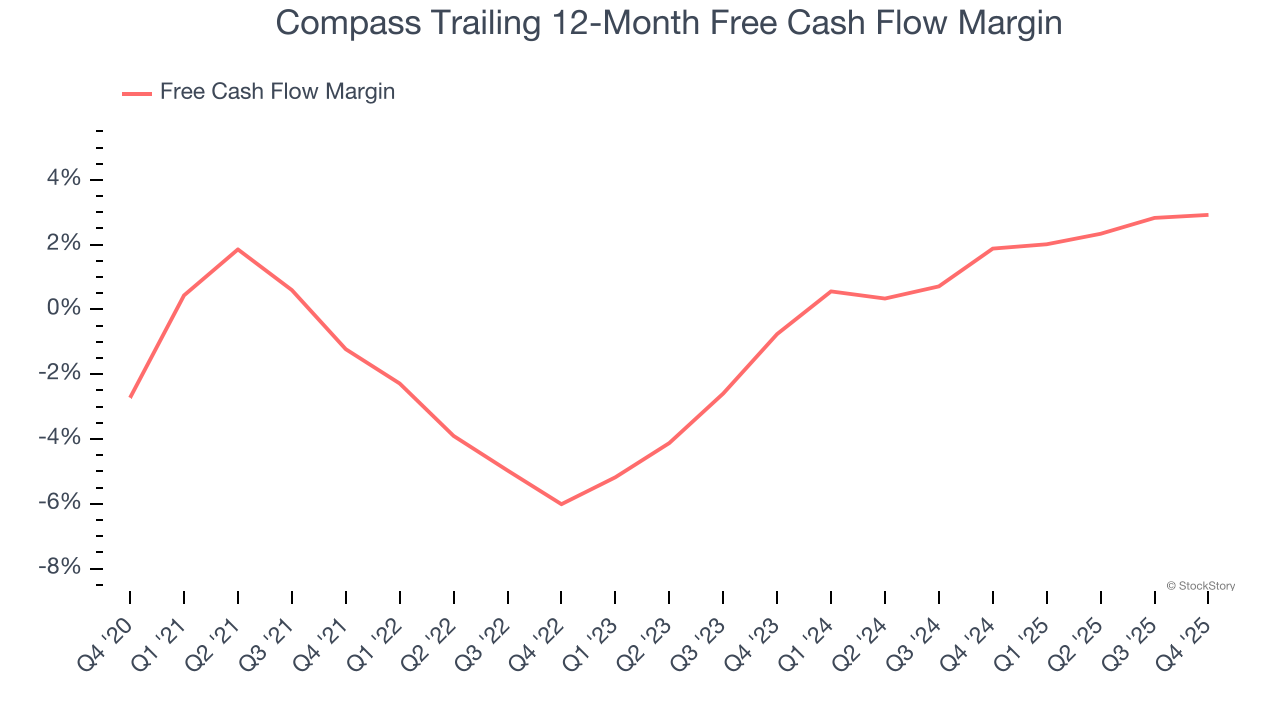

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Compass has shown poor cash profitability relative to peers over the last two years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 2.5%, below what we’d expect for a consumer discretionary business.

We cheer for all companies serving everyday consumers, but in the case of Compass, we’ll be cheering from the sidelines. With its shares underperforming the market lately, the stock trades at 29.9× forward P/E (or $9.40 per share). While this valuation is reasonable, we don’t see a big opportunity at the moment. There are more exciting stocks to buy at the moment. Let us point you toward the most dominant software business in the world.

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

| Jul-30 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-28 | |

| Jul-27 | |

| Jul-21 | |

| Jul-16 | |

| Jul-14 | |

| Jul-14 | |

| Jul-14 | |

| Jul-08 | |

| Jul-08 | |

| Jul-08 | |

| Jul-07 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite