|

|

|

|

|||||

|

|

|

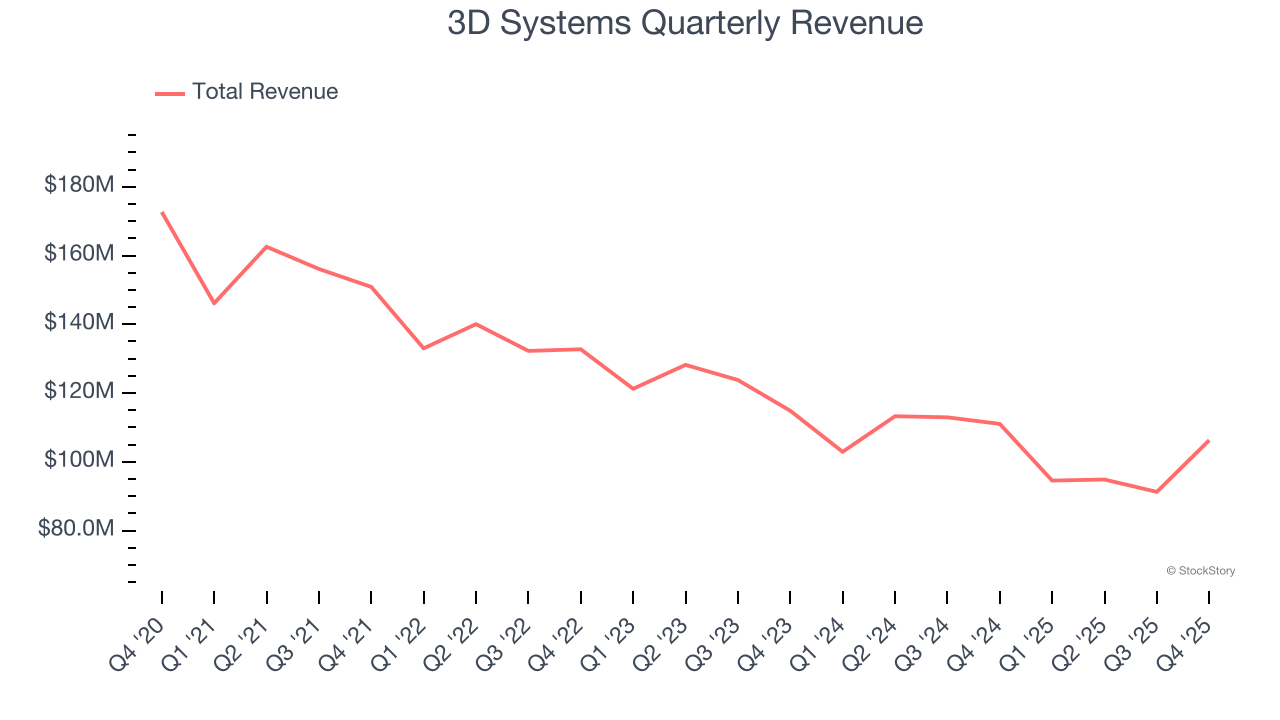

3D printing company 3D Systems (NYSE:DDD) beat Wall Street’s revenue expectations in Q4 CY2025, but sales fell by 4.3% year on year to $106.3 million. On top of that, next quarter’s revenue guidance ($92.5 million at the midpoint) was surprisingly good and 3.5% above what analysts were expecting. Its non-GAAP loss of $0.13 per share was 40.5% below analysts’ consensus estimates.

Is now the time to buy 3D Systems? Find out by accessing our full research report, it’s free.

Dr. Jeffrey Graves, President and CEO of 3D Systems said, "We are pleased with our fourth quarter performance, which exceeded our expectations driven by both our Healthcare and Industrial segments. Three markets were particularly noteworthy: med tech, dental, and aerospace and defense, which are rapidly adopting 3D printing as a core manufacturing method. These three markets have been a particular focus for our new product development over the last several years, and we believe offer sustained, growth opportunities over the next decade."

Founded by the inventor of stereolithography, 3D Systems (NYSE:DDD) engineers, manufactures, and sells 3D printers and other related products to the aerospace, automotive, healthcare, and consumer goods industries.

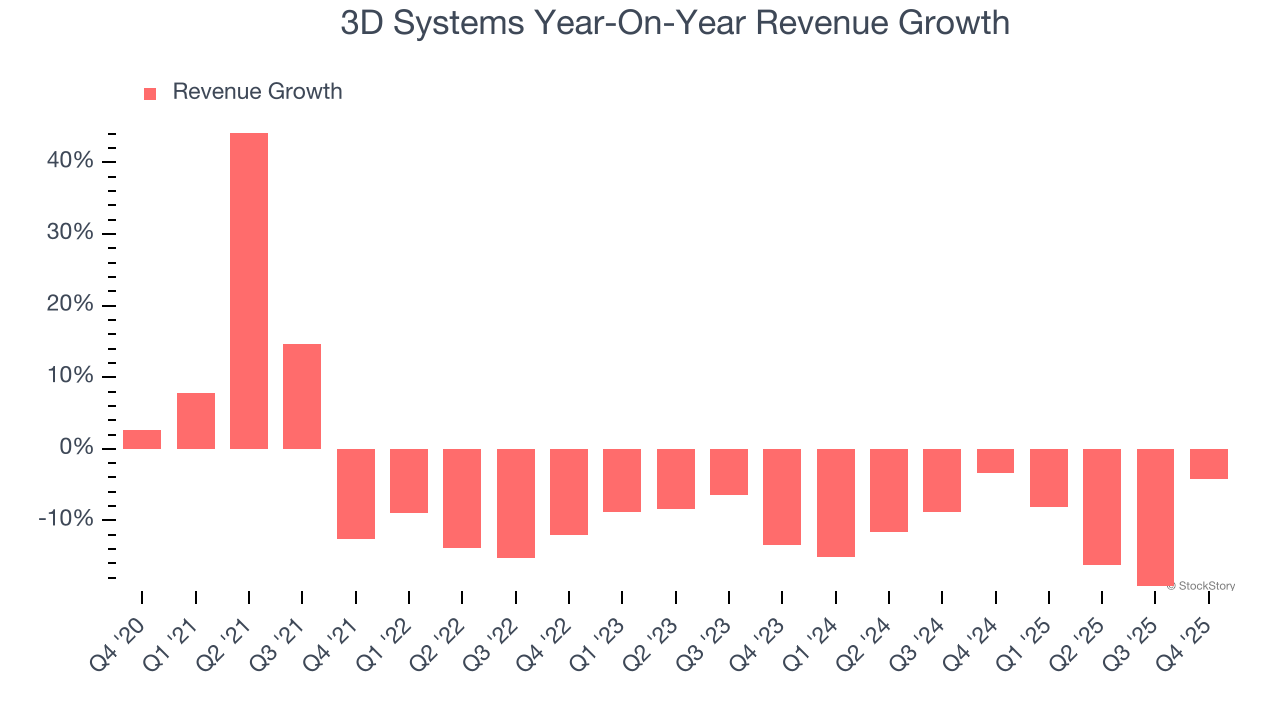

A company’s long-term sales performance is one signal of its overall quality. Any business can have short-term success, but a top-tier one grows for years. 3D Systems’s demand was weak over the last five years as its sales fell at a 7% annual rate. This wasn’t a great result and suggests it’s a low quality business.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. 3D Systems’s recent performance shows its demand remained suppressed as its revenue has declined by 11% annually over the last two years.

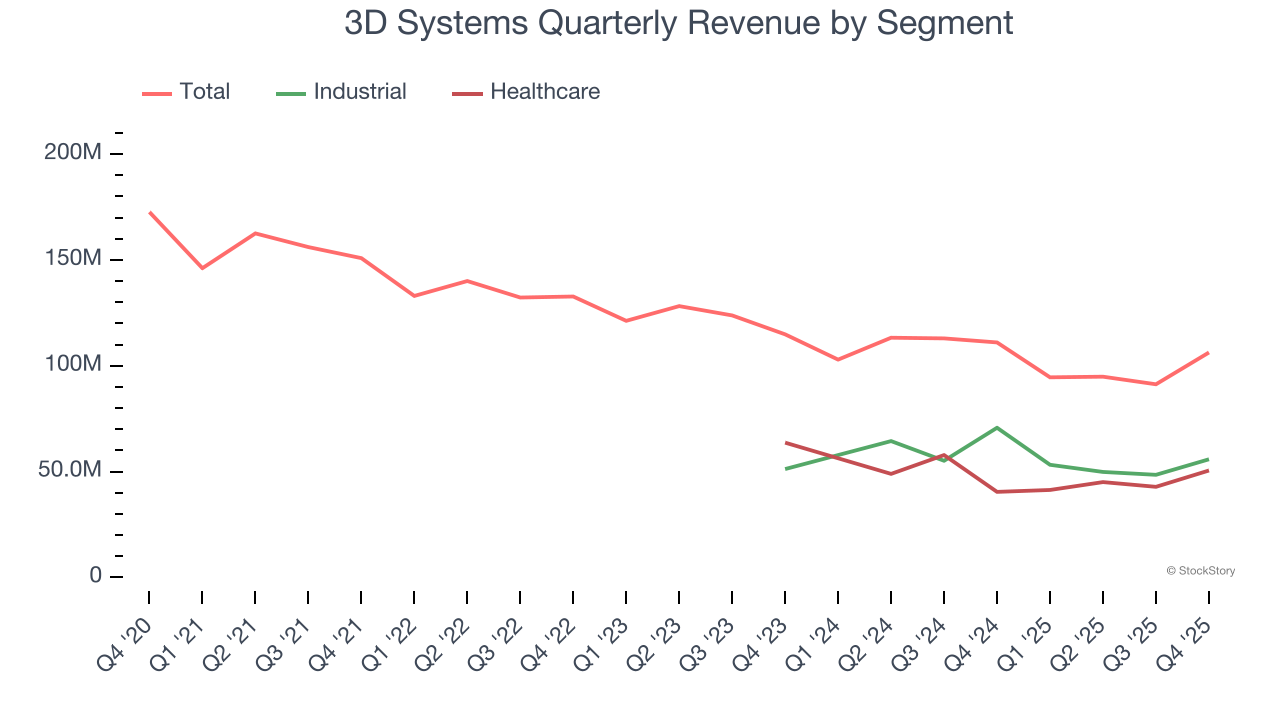

We can dig further into the company’s revenue dynamics by analyzing its most important segments, Industrial and Healthcare, which are 52.5% and 47.5% of revenue. Over the last two years, 3D Systems’s Industrial revenue (aerospace, defense, and transportation manufacturing) averaged 4.4% year-on-year declines while its Healthcare revenue (dental and medical devices) averaged 11.4% declines.

This quarter, 3D Systems’s revenue fell by 4.3% year on year to $106.3 million but beat Wall Street’s estimates by 8.5%. Company management is currently guiding for a 2.2% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to decline by 1.4% over the next 12 months. While this projection is better than its two-year trend, it’s tough to feel optimistic about a company facing demand difficulties.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

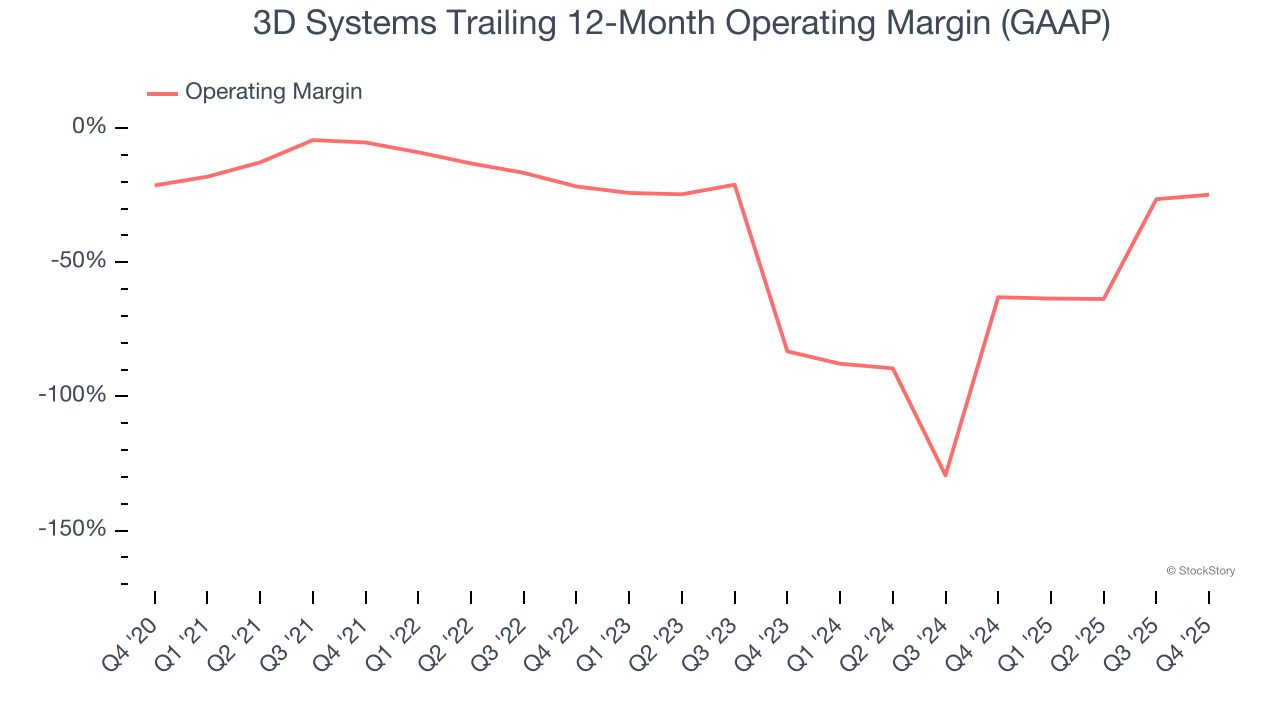

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

3D Systems’s high expenses have contributed to an average operating margin of negative 37.7% over the last five years. Unprofitable industrials companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

Looking at the trend in its profitability, 3D Systems’s operating margin decreased by 19.5 percentage points over the last five years. 3D Systems’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

This quarter, 3D Systems generated a negative 21.3% operating margin. The company's consistent lack of profits raise a flag.

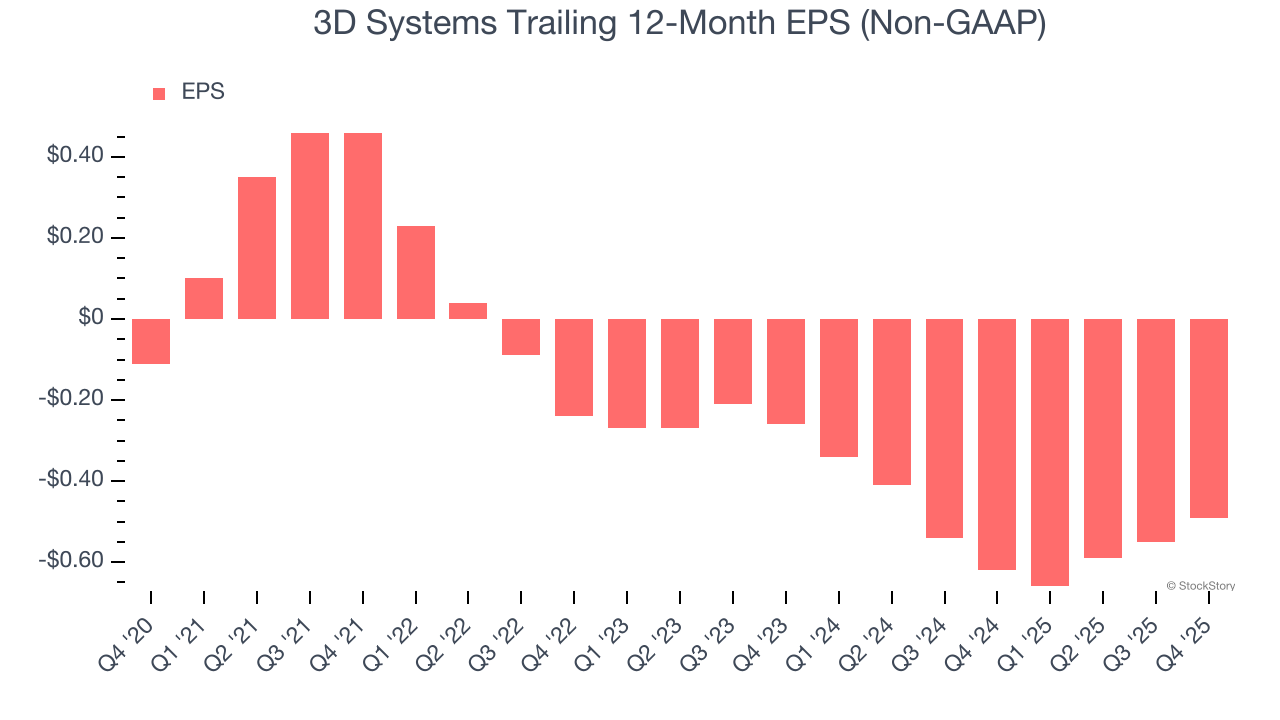

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

3D Systems’s earnings losses deepened over the last five years as its EPS dropped 34.8% annually. We tend to steer our readers away from companies with falling EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, 3D Systems’s low margin of safety could leave its stock price susceptible to large downswings.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For 3D Systems, its two-year annual EPS declines of 37.3% show it’s continued to underperform. These results were bad no matter how you slice the data.

In Q4, 3D Systems reported adjusted EPS of negative $0.13, up from negative $0.19 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates. Over the next 12 months, Wall Street expects 3D Systems to improve its earnings losses. Analysts forecast its full-year EPS of negative $0.49 will advance to negative $0.29.

We were impressed by 3D Systems’s optimistic EBITDA guidance for next quarter, which blew past analysts’ expectations. We were also excited its revenue and EBITDA outperformed Wall Street’s estimates by wide margins. Overall, we think this was a very solid quarter with some key areas of upside. The stock traded up 9.5% to $2.12 immediately following the results.

3D Systems may have had a good quarter, but does that mean you should invest right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).

| Aug-03 | |

| Aug-03 | |

| Jul-29 | |

| Jul-28 | |

| Jul-27 | |

| Jul-23 | |

| Jun-04 | |

| Jun-03 | |

| Jun-03 | |

| May-12 | |

| May-11 | |

| May-11 | |

| May-11 | |

| May-07 | |

| Apr-30 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite