|

|

|

|

|||||

|

|

|

CrowdStrike Holdings CRWD shares have jumped 9.6% since the company reported its fourth-quarter fiscal 2026 results on March 3. The rise in share price can be attributed to better-than-expected fourth-quarter fiscal 2026 results.

In the fourth quarter of fiscal 2026, CrowdStrike reported non-GAAP earnings per share of $1.12, which surpassed the Zacks Consensus Estimate by 1.6%. The bottom line increased 8.7% on a year-over-year basis. The company’s fourth-quarter revenues of $1.31 billion surpassed the consensus estimate by 0.68%. The top line increased 23.6% year over year.

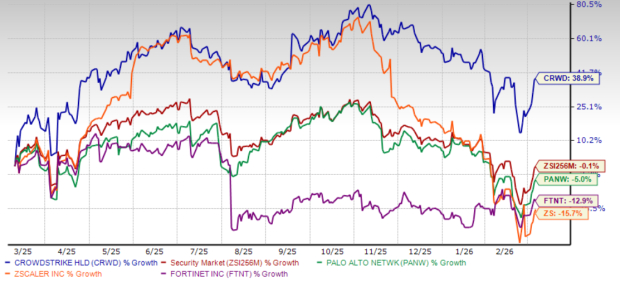

CrowdStrike shares have soared 38.9% in the trailing 12-month period, outperforming the Zacks Security industry’s decline of 0.1%. The stock has outperformed other industry peers, including Palo Alto Networks PANW, Zscaler ZS and Fortinet FTNT. Shares of Palo Alto Networks, Zscaler and Fortinet have plunged 5%, 15.7% and 12.9%, respectively, over the trailing 12-month period.

CrowdStrike has been riding on strong enterprise demand for artificial intelligence (AI)-native cybersecurity solutions. But with the stock outperforming the industry and peers, the question arises: Does it still have room to run, or is it time for investors to consider taking profits? Let’s find out.

CrowdStrike’s subscription business model is driving its overall top-line performance. The company’s revenues crossed the $1 billion mark for the sixth consecutive time during the fourth quarter of fiscal 2026 and marked a year-over-year improvement of nearly 23%. This was partly achieved due to the strong adoption of the Falcon Flex Subscription Model, which allows customers to commit upfront and later choose modules, eliminating procurement friction.

CrowdStrike’s subscription customers, who adopted six or more cloud modules, represented 50% of the total subscription customers at the end of the second quarter. Those with seven or more cloud modules accounted for 34%, and those with eight or more cloud modules represented 24% as of Jan. 31, 2026. In the fourth quarter, Annual Recurring Revenues (ARR) from Falcon Flex customers reached $1.69 billion, rising more than 120% on a year-over-year basis. Management said Falcon Flex is now one of the most common ways customers choose to buy and expand on the Falcon platform.

Falcon Flex helps customers adopt new modules without long contract steps, which leads to faster platform usage. This is also driving strong re-Flex activity, where more than 380 customers expanded their Flex contracts in the fourth quarter. CrowdStrike added more than 350 Flex customers in the fourth quarter and ended fiscal 2026 with over 1,600 customers who have adopted Falcon Flex.

Falcon Flex helps customers adopt new modules without long contract steps, which leads to faster platform usage. This structure is leading to larger deals. Notable examples during the fourth quarter include a large enterprise software company. The customer initially started with CrowdStrike’s threat intelligence module, and is now using 25 different CrowdStrike modules after adopting the Falcon Flex model, committing to a total Falcon Flex contract value of $86 million.

If these patterns continue, Falcon Flex could remain one of CrowdStrike’s most important growth drivers through fiscal 2027 and beyond. The Zacks Consensus Estimate for fiscal 2026 and 2027 revenues indicates a year-over-year increase of around 23% and 21%, respectively.

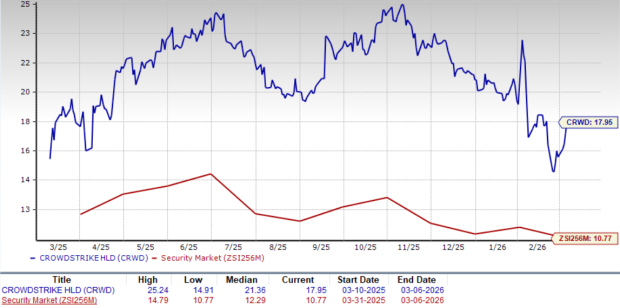

CrowdStrike is currently trading at a high price-to-sales (P/S) multiple, far above the Zacks Security industry. CrowdStrike’s forward 12-month P/S ratio sits at 17.95X, significantly higher than the Zacks Security industry’s forward 12-month P/S ratio of 10.77X. The Zacks Value Score of F also suggests that CRWD stock is overvalued.

CRWD stock also trades at a higher P/S multiple compared with other industry peers, including Palo Alto Networks, Fortinet and Zscaler. At present, Palo Alto Networks, Fortinet and Zscaler have P/S multiples of 10.79X, 8.03X and 7.12X, respectively.

As businesses continue prioritizing AI-driven cybersecurity solutions, CrowdStrike’s leadership in threat prevention, response and recovery will only strengthen. The company’s subscription-based model and recurring revenue streams should provide stability and gradual growth, even amid ongoing macroeconomic challenges and geopolitical issues.

However, the company’s premium valuation warrants a cautious approach to the stock.

CrowdStrike currently has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-08 | |

| Aug-07 | |

| Aug-07 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-04 | |

| Aug-04 | |

| Aug-03 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite