|

|

|

|

|||||

|

|

|

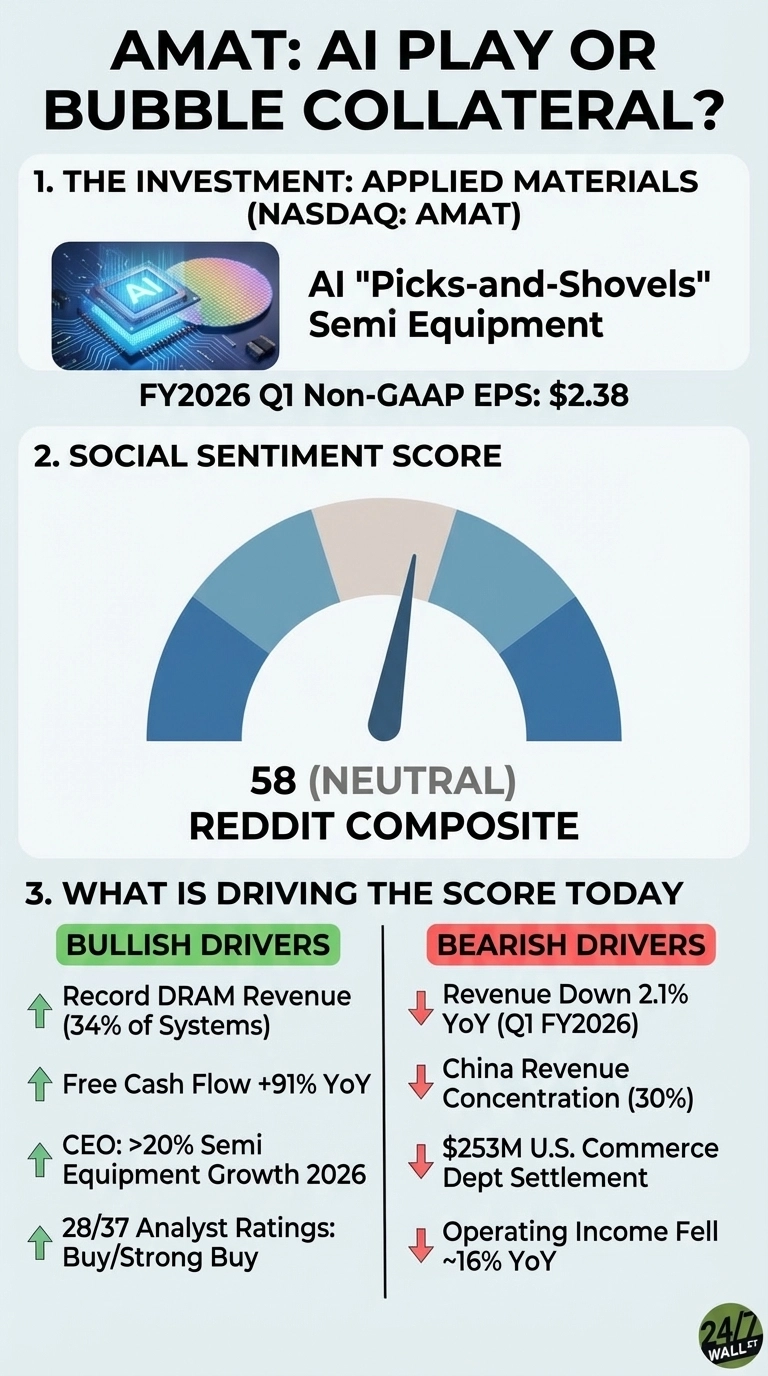

Applied Materials (AMAT) fell 11% to $328 despite $2.38 EPS beat and 20% growth guidance; revenue down 2.1%, operating income down 16%, China 30% of revenue, $253M Commerce settlement. 28 of 37 analysts rate Buy, $411 target. The pullback reflects questions about whether AI-driven semiconductor equipment demand can sustain Applied Materials’ valuation beyond 2026, particularly with China representing 30% of revenue.

A leading supplier of materials that are essential for the manufacturing of semiconductor chips and related electronics, Applied Materials (NASDAQ:AMAT) has shed about 11% over the past week, pulling back from a recent high near $372 to around $328 as of Monday morning. Retail sentiment, measured on a 0-to-100 scale from Reddit activity, sits at a composite score of 58 (neutral), down from bullish readings of 68-72 that dominated various investing communities in early March and mid-February. The debate: Is Applied Materials a legitimate picks-and-shovels AI winner, or is it priced for a cycle closer to its peak than its beginning?

The February earnings report gave bulls real ammunition as Applied Materials posted non-GAAP EPS of $2.38, beating the consensus of $2.21, while CEO Gary Dickerson declared on the call: “We expect to grow our semiconductor equipment business over 20 percent this calendar year.” DRAM now accounts for 34% of Semiconductor Systems revenue, up from 27% a year ago, all free cash flow surged 91% year over year to $1.04 billion.

The “ATH on Zero Growth” Problem Applied Materials Can’t ShakeBears have pointed to the stock’s significant run, even as revenue fell 2.1% year over year in the most recent quarter, with skepticism that the valuation is justified by current fundamentals.

The bears have real data to work with:

Looking ahead, 28 of 37 analysts rate AMAT a Buy or Strong Buy, with zero sell ratings and a consensus price target of around $411. A previously bullish Wall Street consensus has only grown more confident. Yet retail sentiment holds at a neutral 59, and the stock trades at a P/E of 33x, leaving little margin if AI capex slows. According to Finviz, the Zacks Consensus Estimate for AMAT’s current-year earnings increased 14% over the past month to $10.97, though brokerage recommendations carry institutional bias and limited predictive value on their own.

The next test is Q2 FY2026 guidance, where Applied Materials has projected revenue of approximately $7.2 – $8.2 billion and non-GAAP EPS of approximately $2.64. Whether the AI memory cycle has legs beyond 2026 will determine if this pullback reflects a temporary correction or the beginning of a longer-term trend.

Data Sources

| Aug-01 | |

| Aug-01 | |

| Aug-01 | |

| Jul-31 | |

| Jul-31 | |

| Jul-31 | |

| Jul-31 | |

| Jul-31 | |

| Jul-31 | |

| Jul-31 | |

| Jul-31 | |

| Jul-31 | |

| Jul-31 | |

| Jul-31 | |

| Jul-31 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite