|

|

|

|

|||||

|

|

|

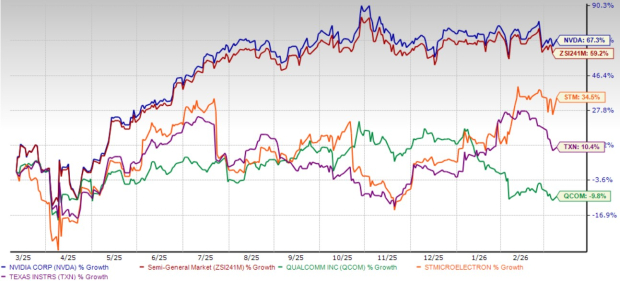

NVIDIA Corporation NVDA shares have soared 67.3% over the past year, outperforming the broader Zacks Semiconductor – General industry’s rise of 59.2%. NVDA has even outpaced major semiconductor companies, including QUALCOMM QCOM, STMicroelectronics STM and Texas Instruments TXN. Shares of STMicroelectronics and Texas Instruments have gained 34.5% and 10.4% in the trailing 12 months, while shares of QUALCOMM have declined 9.8%.

NVIDIA has been a key beneficiary of the artificial intelligence (AI) boom, which has driven strong demand for its graphics processing units (GPUs) and computing solutions. As the demand for hardware supporting AI and high-performance computing is likely to remain strong, NVDA is well-positioned to benefit. This makes the stock a better investment option right now.

NVIDIA’s most powerful growth engine continues to be its Data Center business. In the fourth quarter of fiscal 2026, the segment generated $62.31 billion in revenues, representing 91.5% of total sales. This marked a staggering 75% year-over-year increase and 22% sequential growth.

The robust performance was mainly driven by higher shipments of the Blackwell GPU computing platforms that are used for the training and inference of large language models, recommendation engines and generative AI applications.

The demand for NVIDIA’s Blackwell GPU computing platforms has been a key catalyst as cloud providers and enterprises scale their AI infrastructure. Large cloud service providers contributed to the majority of Data Center revenues, indicating continued hyperscale investment in AI-driven computing.

With AI adoption accelerating across industries, NVIDIA's stronghold in data centers makes it a critical beneficiary of this trend. The company’s leadership in AI chip development positions it well for sustained revenue growth in this segment.

Despite ongoing macroeconomic challenges, geopolitical issues, and trade and tariff wars, NVIDIA’s financials remain rock solid. In the fourth quarter of fiscal 2026, revenues jumped 73% from the year-ago quarter, while non-GAAP earnings per share rose 82%.

NVIDIA’s outlook for the first quarter of fiscal 2027 remains upbeat. The company expects first-quarter revenues to increase 77% year over year to $78 billion, reflecting continued momentum in AI-driven demand. The non-GAAP gross margin is expected to be strong at 75%, indicating a 370-basis-point improvement from the year-ago quarter’s 71.3% (excluding H20 charge).

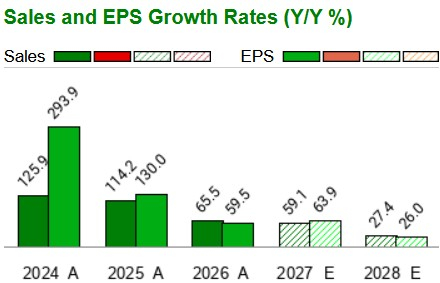

The Zacks Consensus Estimate for fiscal 2027 and 2028 suggests continued growth momentum for the company’s top and bottom lines.

NVIDIA’s cash flow generation also remains robust. It generated a free cash flow of $36.19 billion in the fiscal fourth quarter and $102.72 billion in fiscal 2026. The company ended the fiscal fourth quarter with $62.6 billion in cash, cash equivalents and marketable securities, up from $60.6 billion in the previous quarter.

This strong liquidity position enables NVIDIA to reinvest in research and development, expand manufacturing capabilities and return capital to shareholders. In the fiscal fourth quarter, the company returned $243 million to its shareholders through dividend payouts and repurchased stocks worth $3.82 billion. In fiscal 2026, NVIDIA paid out $974 million in dividends and bought back shares worth $40.09 billion.

Despite the rally, NVIDIA stock trades at a reasonable valuation multiple. It trades at a forward 12-month price-to-earnings (P/E) of 22.73X compared with the industry average of 24.5X.

Compared to other semiconductor peers, NVIDIA has a higher P/E multiple than QUALCOMM but a lower multiple than STMicroelectronics and Texas Instruments. Currently, QUALCOMM, STMicroelectronics and Texas Instruments trade at P/E of 11.99X, 26.08X and 29.22X, respectively.

NVIDIA’s strong fundamentals, dominant position in AI and impressive growth outlook make a compelling case for staying invested. The company’s reasonable valuations support buying the stock.

Currently, NVIDIA carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 6 hours | |

| Jul-10 | |

| Jul-10 | |

| Jul-10 | |

| Jul-10 | |

| Jul-10 | |

| Jul-10 | |

| Jul-10 | |

| Jul-10 | |

| Jul-10 | |

| Jul-10 | |

| Jul-10 | |

| Jul-10 | |

| Jul-10 | |

| Jul-10 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite