|

|

|

|

|||||

|

|

|

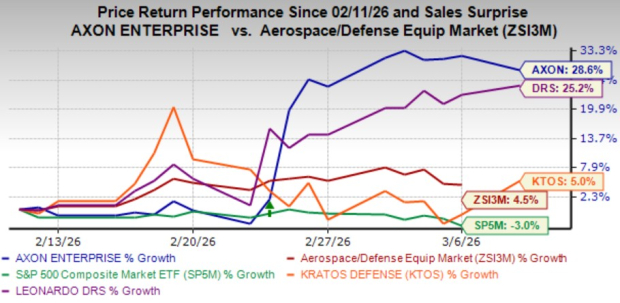

Shares of Axon Enterprise, Inc. AXON have been showing impressive gains of late, rising 28.6% in the past month. Shares of the public safety technology solution provider have outpaced the Zacks sub-industry’s growth of 4.5% and the S&P 500 composite’s 3% decline. The company has also outperformed other industry players like Kratos Defense & Security Solutions, Inc. KTOS and Leonardo DRS, Inc. DRS, which have returned 5% and 25.2%, respectively, over the same time frame.

Closing at $559.06 yesterday, the stock is trading below its 52-week high of $885.92 but significantly higher than its 52-week low of $396.41. Although the stock is hovering above its 50-day moving average, it is trading below its 200-day moving average.

The strongest driver of Axon’s business at the moment is solid momentum in its Connected Devices segment. The company continues to witness growing popularity for its next-generation TASER 10 products, whose shipment began in 2023. Growth in cartridge revenues, driven by higher adoption of the TASER products, has been driving the segment’s performance. Solid demand for its next-generation body-worn camera, Axon Body 4, virtual reality training services and counter-drone equipment also supports its growth. Segmental revenues increased 29.1% year over year in 2025.

An increase in the aggregate number of users to the Axon network is aiding the Software & Services segment. Continued momentum in digital evidence management and increased demand for premium add-on features are driving the segment’s growth. Adoption of premium subscription plans also continues to rise as more customers recognize the value of enhanced capabilities. Revenues from the segment increased 39.6% in 2025.

The company remains focused on investing in newer areas within the software business, like AI products, real-time operations, drones and robotics, which bodes well for growth. Given the strength across its business, Axon provided bullish financial guidance. For 2026, the company expects revenues to increase in the range of 27-30% year over year.

The company’s strategic partnership with other companies enables it to expand its product offerings and customer base. In October 2025, Axon’s Dedrone business announced its partnership with TYTAN (a leading provider of interceptor systems for Group 3 drones) to boost detection, identification and mitigation capabilities of counter drone equipment. The integration of TYTAN’s kinetic interceptor technology enhances Dedrone’s CUAS mitigation capability, making it suitable to deploy against Group 3 threats.

The escalating costs and expenses are a concern for Axon’s bottom line. In 2025, the company’s cost of sales soared 33.3% year over year. The company incurred high costs and expenses related to business integration activities, an increase in headcount and higher wages and stock-based compensation expenses. Axon’s selling, general and administrative expenses also surged 39.8% year over year in 2025.

Axon has been facing the pressure of rising debt levels. Exiting the fourth quarter of 2025, the company’s long-term notes payable (net) were $1.73 billion. The same stood at zero at the end of 2024. This increase was primarily due to funds raised to support the company’s strategic investments, expansion activities and potential acquisitions.

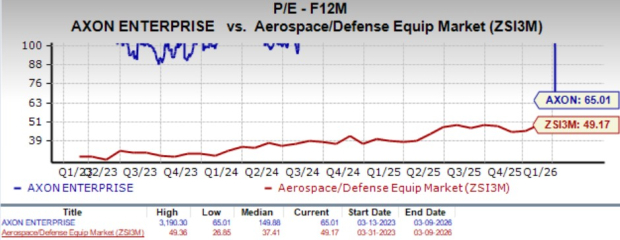

AXON’s lofty valuation remains a concern. The stock is trading at a forward 12-month price-to-earnings (P/E) ratio of 65.01X, higher than the industry average of 49.17X. This elevated valuation could make the stock vulnerable to further pullbacks if market sentiment sours.

While its peer, Leonardo DRS, is trading cheaper compared with AXON, Kratos Defense is trading at a premium. Notably, Leonardo DRS and Kratos Defense are trading at 36.85X and 111.68X, respectively.

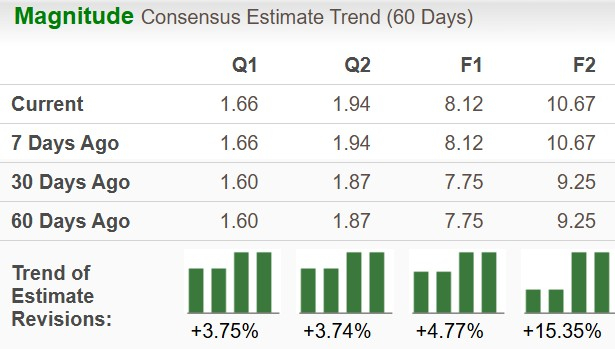

The company’s earnings estimates for 2026 have increased 4.8% to $8.12 per share over the past 60 days. The figure indicates year-over-year growth of 18.5%.

Earnings estimates for 2027 have increased 15.4% to $10.67 per share. The figure also indicates year-over-year growth of 31.5%.

Solid momentum across the Connected Devices and Software & Services segments, along with its investments in the AI space, drones and robotics, positions AXON favorably for impressive growth in the long run. However, a few challenges, such as escalating operating expenses, premium valuation and rising debt, are limiting this Zacks Rank #3 (Hold) company’s near-term prospects.

While current shareholders should hold their positions, new investors should wait for the stock to retract some of its recent gains and provide a better entry point. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-03 | |

| Aug-02 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-28 | |

| Jul-28 | |

| Jul-27 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-22 | |

| Jul-21 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite