|

|

|

|

|||||

|

|

|

A. O. Smith Corporation AOS has been benefiting from strong demand for commercial water heaters and boilers in North America. Also, organic sales from India have been particularly strong, jumping 12.9% year over year in 2025. A. O. Smith expects sales from its North America boiler business to grow approximately 6-8% this year, while volumes from the commercial water heater business are expected to increase in mid-single digits.

A. O. Smith remains focused on acquiring businesses to gain access to new customers, regions and product lines. For instance, in January 2026, the company completed the acquisition of LVC Holdco LLC (Leonard Valve) for $470 million. The buyout is likely to strengthen its water heating and boiler offerings and boost its presence in the water management market. It expects the addition of Leonard Valve to contribute approximately $70 million to its sales in 2026.

Management is committed to rewarding shareholders through dividend payouts and share repurchases. In 2025, it paid dividends worth $195.7 million and repurchased shares worth $400.8 million. In October 2025, it hiked its dividend by 6% to 36 cents per share. For 2026, it expects to repurchase shares worth approximately $200 million.

Also, AOS’ sound liquidity position adds to its strength. Exiting 2025, it had cash and cash equivalents of $174.5 million, higher than the current debt of $42.3 million.

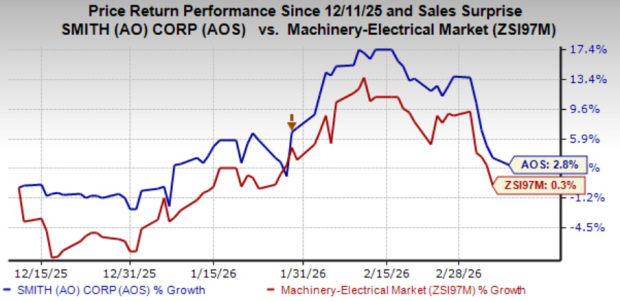

In the past three months, the Zacks Rank #3 (Hold) company has gained 2.8% compared with the industry’s 0.3% growth.

However, lower volumes of residential water treatment and water heater products in China remain challenging for the Rest of the World segment. The segment’s revenues declined 4% year over year in 2025. AOS issued a lackluster 2025 sales outlook for China. It currently expects the metric to decrease in mid-single digits on a year-over-year basis in local currency.

Also, rising operating expenses pose a threat to A. O. Smith’s bottom line. In 2025, AOS’ selling, general and administrative expenses increased 2.7% on a year-over-year basis. The metric, as a percentage of sales, increased 40 basis points. The rise was attributable to higher employee costs from increased wages and management incentives.

Some better-ranked stocks from the same space are discussed below.

Flowserve Corporation FLS presently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Flowserve’s earnings surpassed the consensus estimate in each of the trailing four quarters. The average earnings surprise was 17.3%. In the past 60 days, the Zacks Consensus Estimate for Flowserve’s 2026 earnings has increased 4.6%.

Nordson Corporation NDSN currently carries a Zacks Rank #2 (Buy). Nordson’s earnings topped the consensus estimate in each of the trailing four quarters. The average earnings surprise was 2.5%. In the past 60 days, the Zacks Consensus Estimate for Nordson’s fiscal 2026 earnings has increased 1.4%.

Parker-Hannifin Corporation PH currently carries a Zacks Rank of 2. Parker-Hannifin’s earnings topped the consensus estimate in each of the trailing four quarters. The average earnings surprise was 6.8%. In the past 60 days, the Zacks Consensus Estimate for Parker-Hannifin’s fiscal 2026 earnings has increased 2.3%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 14 hours | |

| 15 hours | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-29 | |

| Jul-29 | |

| Jul-27 | |

| Jul-24 | |

| Jul-23 | |

| Jul-22 | |

| Jul-21 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite