|

|

|

|

|||||

|

|

|

Pan American Silver Corp. PAAS has skyrocketed 151% in a year compared with the industry’s upsurge of 193.6%. Meanwhile, the Basic Materials sector has risen 47.1%, and the S&P 500 has returned 25.6%.

With the PAAS stock riding high, investors may rush to add it to their portfolio. However, before making a decision, it will be prudent to take a look at the reasons behind the surge, the company’s growth prospects and risks (if any) in investing.

Pan American Silver reported record revenues of $3.62 billion in 2025, marking an improvement of 28.4% from 2024. This includes a record $1.18 billion in revenues in the fourth quarter of 2025. This impressive performance was driven by higher metal prices and silver production. However, this was partially offset by a decrease in quantities of metal sold due to the disposition of La Arena, and lower production at Dolores and Minera Florida.

The company produced 22.8 million ounces of silver in 2025, surpassing the company’s expectations. The figure increased 8% from 2024. Pan American Silver produced a record 7.3 million ounces of silver in the fourth quarter of 2025 on better-than-expected results at the Juanicipio mine.

The company’s gold production came in at 742.2 thousand ounces for 2025, in line with its guidance. It produced 197.8 thousand ounces in the fourth quarter of 2025. For 2026, the company expects silver production of 25-27 million ounces, indicating a year-over-year increase of 14% at the mid-point. Gold production is expected between 700 million and 750 million, indicating a dip of 2%.

Mine operating earnings surged 156% year over year to $1.4 billion in 2025. Adjusted earnings per share were $2.54, marking a significant jump from the year-ago’s 79 cents. The company reported a record cash flow in 2025, indicating robust operational cash generation and disciplined capital spending. A free cash flow of $1.15 billion in 2025 pushed Pan American Silver’s cash and short-term investments balance to $1.3 billion.

Backed by a strong cash flow generation, PAAS hiked its quarterly dividend 29% to 18 cents from the prior payment of 14 cents. In comparison, its peer Hecla Mining Company HL maintains an annual dividend of 2 cents and Endeavour Silver Corporation EXK currently does not pay a dividend.

In September 2025, PAAS completed the acquisition of MAG Silver Corp. This move boosts Pan American Silver’s position as one of the leading silver producers globally and significantly strengthens the company’s industry-leading silver reserve base.

Pan American Silver gained a 44% stake in the Juanicipio project, which is a large-scale, high-grade silver mine in Zacatecas operated by Fresnillo plc.

The transaction also adds the full ownership of the Larder exploration project and a full earn-in interest in the Deer Trail exploration project to PAAS’s portfolio. The addition of these assets will contribute significantly to Pan American Silver’s production, reserves and cash flow.

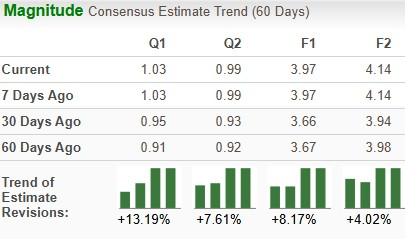

The consensus mark for 2026 earnings is pegged at $3.97 per share, indicating a year-over-year jump of 56.3%. The estimate for 2027 of $4.14 suggests an increase of 4.3%.

The Zacks Consensus Estimate for Pan American Silver’s earnings for 2026 has moved up 8.2% over the past 60 days. The same for 2027 has moved up 4%.

PAAS has solidified its position as a leading precious metal producer in the Americas with a diversified asset base. The company has been rationalizing its portfolio following the Yamana acquisition (in 2023) and investing in its producing mines while advancing organic opportunities.

In December 2025, the company reported strong drilling results for its operating mines, which will help advance its long-term exploration strategy to replace and grow its mineral resources. The company has also been successfully extending the lifespan of many of its operations, driven by ongoing exploration efforts across its portfolio.

The company invested $94 million in project capital in 2025 to advance several major projects, among which the most notable is the La Colorada mine in Mexico. The company is reevaluating the development plans for the Skarn project since the discovery of high-grade silver zones and increased mineral resources at La Colorada.

Pan American Silver aims to combine the mine plans and infrastructure of the La Colorada vein mine with the Skarn project through a phased development approach. With this approach, the company can focus on high-grade, low-tonnage and less capital-intensive initial stages, while targeting lower-grade material in a future expansion.

Silver prices have increased a whopping 167.8% year over year on resilient industrial demand and mounting supply deficits. Demand for solar energy, electronics and electrification now accounts for more than half of global silver demand. Currently, silver is trading at above $88 per ounce. Along with PAAS, these upsides in prices of gold and silver are aiding its peers, Hecla Mining and Endeavour Silver.

Pan American Silver is currently trading at a forward 12-month price-to-earnings multiple of 15.12X, at a discount to the industry average of 18.15X.

In comparison, Endeavour Silver and Hecla Mining are trading higher at 18.65X and 36.58, respectively.

PAAS is well-positioned to capitalize on the ongoing rally in silver prices and the recent MAG Silver buyout. Continued investments in growth initiatives strengthen its long-term prospects. While its appealing valuation makes the stock attractive, a lower gold outlook suggests caution for new investors.

Existing shareholders should stay invested in the PAAS stock to benefit from its solid long-term growth prospects. The company currently has a Zacks Rank #3 (Hold), which supports our thesis.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-31 | |

| Jul-30 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-28 | |

| Jul-23 | |

| Jul-23 | |

| Jul-16 | |

| Jul-15 | |

| Jul-14 | |

| Jul-09 | |

| Jul-09 | |

| Jul-08 | |

| Jul-08 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite