|

|

|

|

|||||

|

|

|

West Pharmaceutical Services has been treading water for the past six months, recording a small loss of 2.7% while holding steady at $248.28. The stock also fell short of the S&P 500’s 3.1% gain during that period.

Is there a buying opportunity in West Pharmaceutical Services, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.

We're sitting this one out for now. Here are three reasons there are better opportunities than WST and a stock we'd rather own.

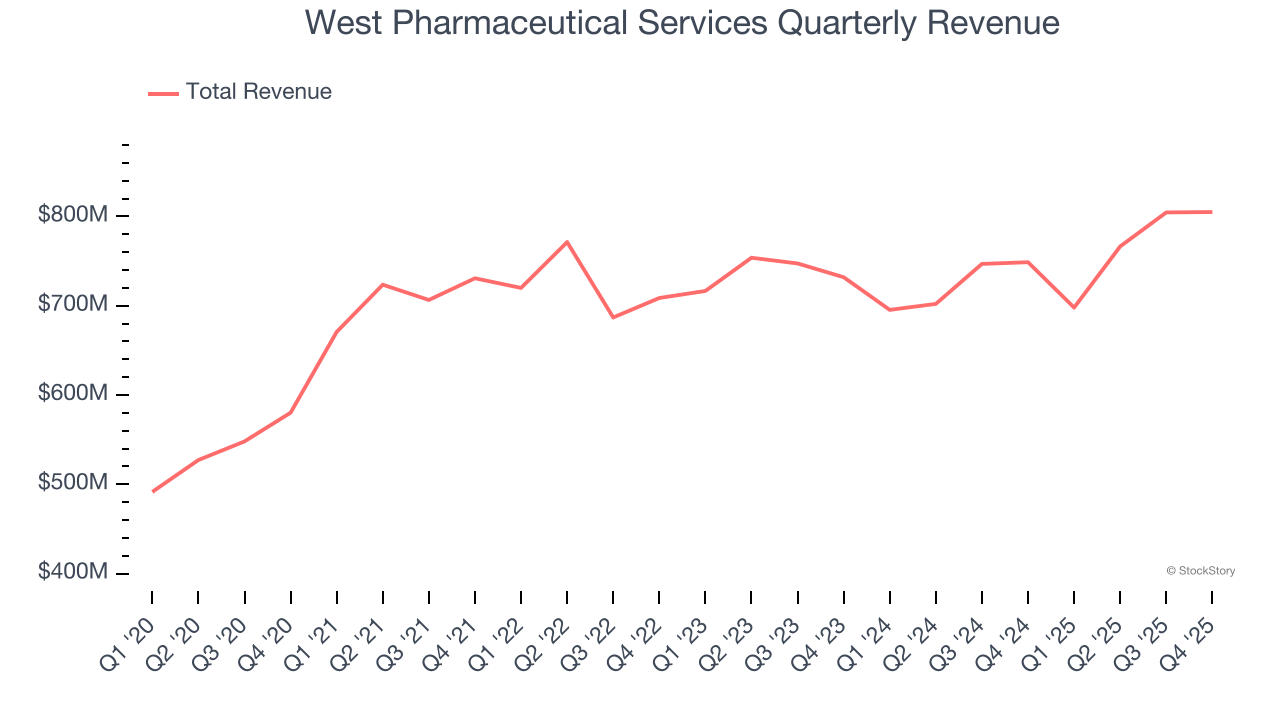

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Unfortunately, West Pharmaceutical Services’s 7.4% annualized revenue growth over the last five years was mediocre. This was below our standard for the healthcare sector.

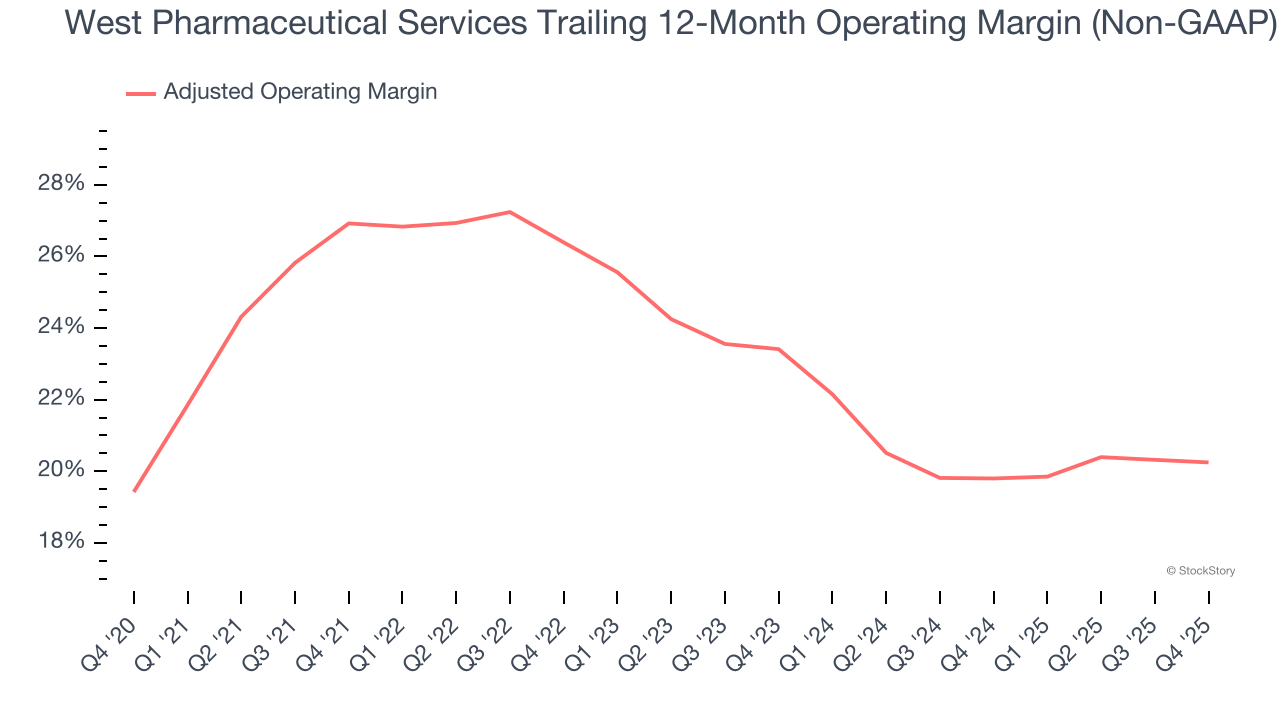

Adjusted operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies because it excludes non-recurring expenses, interest on debt, and taxes.

Looking at the trend in its profitability, West Pharmaceutical Services’s adjusted operating margin decreased by 6.7 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Its adjusted operating margin for the trailing 12 months was 20.2%.

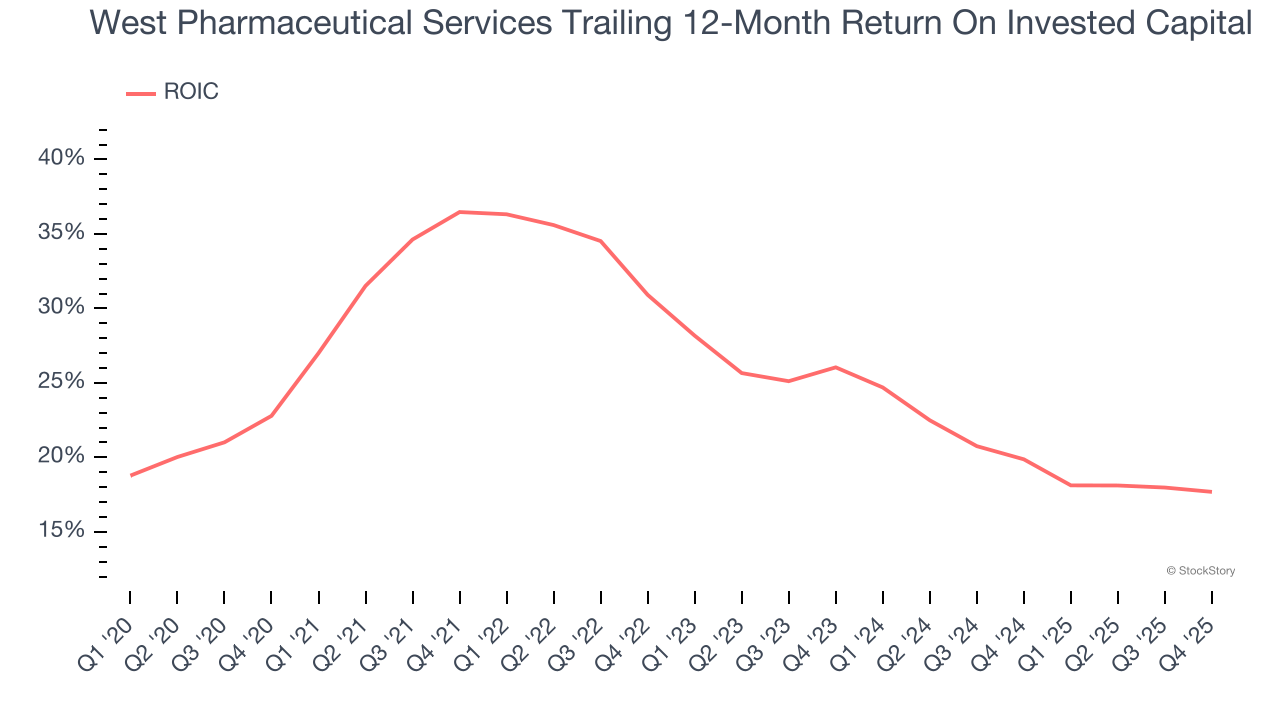

ROIC, or return on invested capital, is a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, West Pharmaceutical Services’s ROIC has decreased significantly over the last few years. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

West Pharmaceutical Services’s business quality ultimately falls short of our standards. With its shares lagging the market recently, the stock trades at 30.7× forward P/E (or $248.28 per share). At this valuation, there’s a lot of good news priced in - you can find more timely opportunities elsewhere. We’d suggest looking at a top digital advertising platform riding the creator economy.

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it's flagging for this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-21 | |

| Jul-17 | |

| Jul-17 | |

| Jul-07 | |

| Jul-01 | |

| Jun-01 | |

| May-20 | |

| May-14 | |

| May-12 | |

| Apr-28 | |

| Apr-24 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite