|

|

|

|

|||||

|

|

|

Shareholders of Upstart would probably like to forget the past six months even happened. The stock dropped 55.5% and now trades at $27.78. This may have investors wondering how to approach the situation.

Given the weaker price action, is now the time to buy UPST? Find out in our full research report, it’s free.

Using over 2,500 data variables and trained on nearly 82 million repayment events, Upstart (NASDAQ:UPST) is an AI-powered lending platform that uses machine learning to help banks and credit unions more accurately assess borrower risk for personal loans, auto loans, and home equity lines of credit.

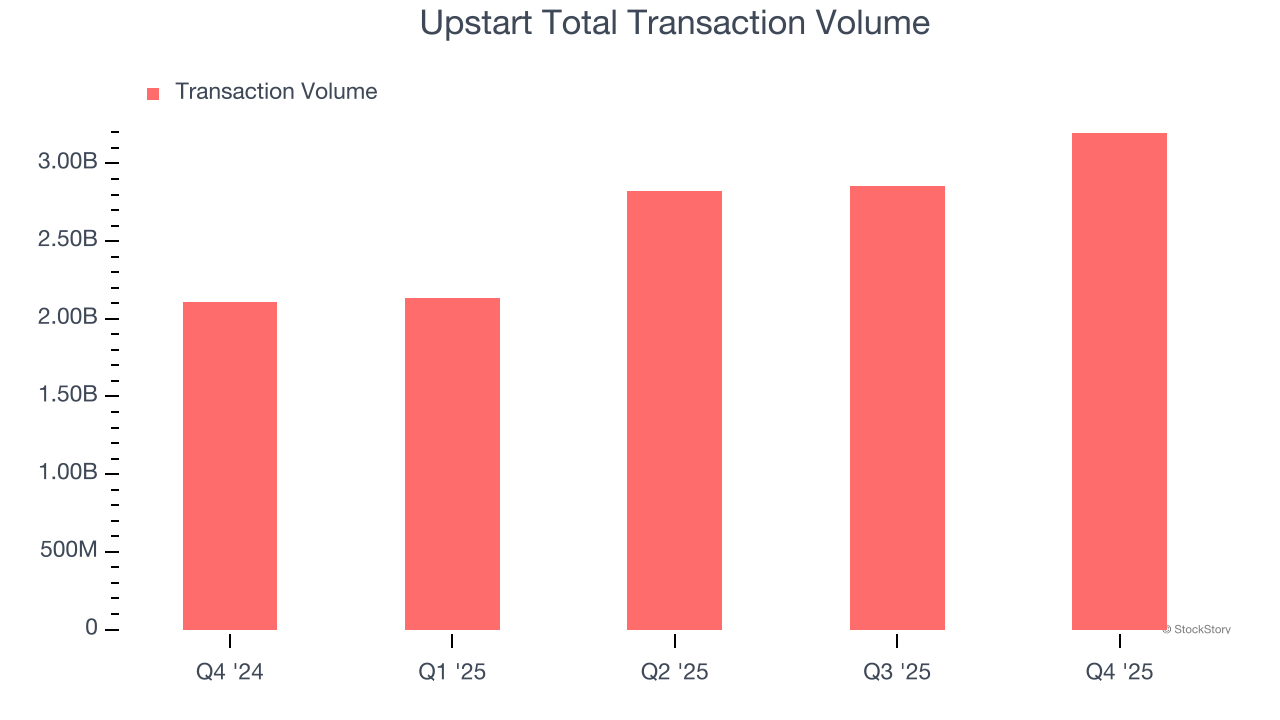

Total transaction volumes show the aggregate dollar value of loans processed on Upstart’s platform. This is the number from which the company will ultimately collect fees, and the higher it is, the more accurate its software becomes at assessing credit risk.

Upstart’s transaction volume punched in at $3.20 billion in Q4, and over the last four quarters, its year-on-year growth averaged 51.6%. This performance was fantastic and shows the company is capturing significant demand. It also indicates that customers are increasingly using Upstart’s platform to process loans, enabling it to collect more fees and expand into new markets (like credit cards).

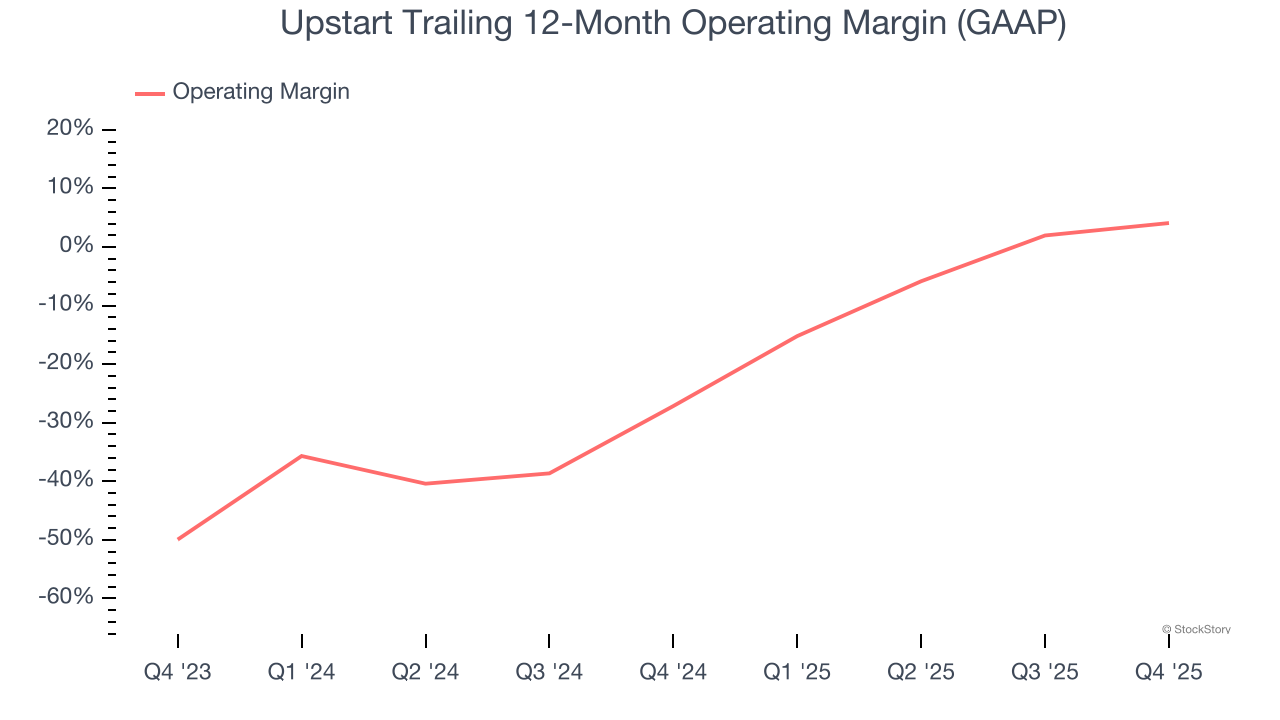

While many software businesses point investors to their adjusted profits, which exclude stock-based compensation (SBC), we prefer GAAP operating margin because SBC is a legitimate expense used to attract and retain talent. This is one of the best measures of profitability because it shows how much money a company takes home after developing, marketing, and selling its products.

Analyzing the trend in its profitability, Upstart’s operating margin rose by 31.2 percentage points over the last two years, as its sales growth gave it immense operating leverage. Its operating margin for the trailing 12 months was 4.1%.

The customer acquisition cost (CAC) payback period represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for sales and marketing investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

Upstart’s recent customer acquisition efforts haven’t yielded returns as its CAC payback period was negative this quarter, meaning its incremental sales and marketing investments outpaced its revenue. The company’s inefficiency indicates it operates in a competitive market and must continue investing to grow.

Upstart has huge potential even though it has some open questions. After the recent drawdown, the stock trades at 2.2× forward price-to-sales (or $27.78 per share). Is now the time to initiate a position? See for yourself in our full research report, it’s free.

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-03 | |

| Jul-29 | |

| Jul-29 | |

| Jul-28 | |

| Jul-24 | |

| Jul-23 | |

| Jul-08 | |

| Jul-06 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite