|

|

|

|

|||||

|

|

|

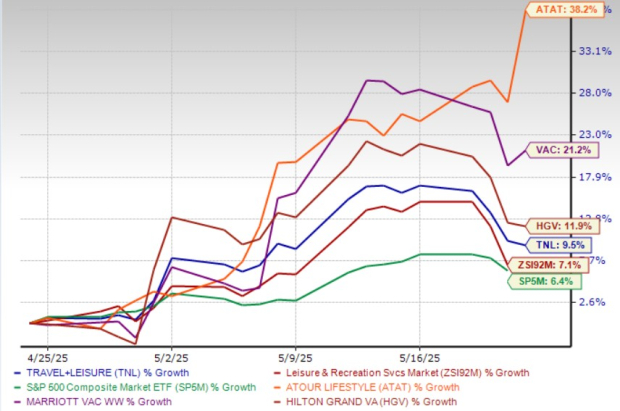

Travel + Leisure Co.’s TNL shares have gained 9.5% in a month compared with the industry and the S&P 500’s growth of 7.1% and 6.4%, respectively.

On Thursday, the stock closed at $47.89, below its 52-week high of $58.95, but up from 52-week low of $37.77. In the past month, shares of other industry players like Atour Lifestyle Holdings Limited ATAT, Marriott Vacations Worldwide Corporation VAC and Hilton Grand Vacations Inc. HGV have gained 38.2%, 21.2% and 11.9%, respectively.

Technical indicators imply TNL's continued strong performance. The stock is trading above its 50-day moving average, signaling robust upward momentum and price stability. This technical strength underscores positive market sentiment and confidence in TNL's financial health and prospects.

In the first quarter of 2025, Travel + Leisure demonstrated strong underlying consumer demand for its vacation ownership offerings. A key performance metric, Volume Per Guest (“VPG”) rose to $3,212, an increase from the prior year. The figure was solidly above the $3,000 threshold, signaling healthy spending behavior from guests. The company also noted a pickup in resort bookings, particularly as the quarter advanced, reflecting owners’ continued eagerness to utilize their vacation options. Additional portfolio performance indicators are expected to be addressed in more detail during the executive overview.

Several positive trends within the owner base indicate promising long-term growth prospects for the vacation ownership business. The average age of the company’s owners has shifted to the mid-50s, implying increased sales to Gen X, millennials and younger generations. At the same time, a disciplined approach to tour generation has significantly improved the credit quality of the loan portfolio.

Additionally, travel remains central to the experience economy with top destinations like Florida continuing to perform well, alongside growing interest in family-friendly locations, such as Washington, D.C., the Pacific Northwest and the Smoky Mountains. Backed by a solid foundation, a diverse geographic footprint and a unique multi-brand strategy, the company is well-positioned to capture a larger share of the vacation travel market by offering a wide range of ownership options tailored to consumer needs.

Travel + Leisure is sharpening its brand strategy through key partnerships and targeted expansion efforts. In the first quarter, its Blue Thread collaboration with Wyndham Hotels contributed 7% of new owner tours, delivering a VPG more than 20% up from other new owner channels, a clear indicator of its effectiveness. The company’s partnership with Wyndham's core brand in Asia Pacific continues to show positive momentum after a year in operation.

Looking ahead, Travel + Leisure remains on track to launch Sports Illustrated-branded sales in 2025 and has ramped up efforts to grow the Margaritaville brand, highlighted by the recently announced Margaritaville Resort in Orlando, slated to open in 2027 near Disney. This strategic addition will include a Vacation Ownership resort alongside an existing 265-room hotel and 900 cottages. The company has also nearly completed an internal realignment to better align its strategic, economic and personnel goals around these brands, reinforcing commitment to focused and effective brand execution.

The Zacks Consensus Estimate for 2024 and 2025 earnings per share has witnessed downward revisions of 0.8% and 1.1% to $6.40 and $7.43, respectively.

TNL is currently valued at a discount compared with the industry on a forward 12-month P/E basis. Its forward 12-month price-to-earnings ratio is 7.04, significantly lower than the industry. The company is also trading currently at a discount compared with other industry players like Atour Lifestyle, Marriott Vacations and Hilton Grand Vacations.

Broader macroeconomic conditions and declining consumer sentiment in 2025 posed risks to discretionary spending behavior, particularly among new buyers. TNL noted a dip in new owner close rates in first-quarter 2025, partially offset by an uptick in existing owner upgrades.

Travel + Leisure has demonstrated solid operational performance and resilient consumer demand, particularly within its core vacation ownership segment, supported by strong engagement from a loyal owner base and successful brand partnerships. While its stock has shown positive momentum and technical strength, concerns around weakening consumer sentiment and softer new owner close rates suggest emerging headwinds that could temper near-term upside.

Despite trading at a valuation discount to peers, cautious earnings estimate revisions and a less favorable macroeconomic backdrop advise prudence. Current investors may benefit from holding their position, but new buyers should wait for clearer visibility on growth sustainability and broader economic stability. The company currently has a Zacks Rank #3 (Hold).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 3 hours | |

| 4 hours | |

| Jul-20 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-16 | |

| Jul-16 | |

| Jul-15 | |

| Jul-14 | |

| Jul-09 | |

| Jul-07 | |

| Jul-02 | |

| Jul-01 | |

| Jun-29 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite